Since the big CPI and PPI prints earlier this week, markets have been trying to figure out direction and sentiment. What will be the outcome of continued higher inflation prints?

Capital markets seem to be a bit confused as to what to do next. As Federal Reserve Chair Powell testified in front of House and Senate committees over the last two days, there doesn’t seem to be any additional clarity in my eyes.

I wanted to wait until the Fed’s 2-day testimony concluded before publishing today’s opinion piece to gain any additional clarity on the markets.

There is a conundrum that exists right now. We keep getting higher inflation readings, and the Fed has already telecasted that higher rates are in the cards in 2023 (maybe 2022). Inflation is a problem and needs to be tamed. One way of taming it is to raise interest rates. There are other tools at the Fed’s disposal to tame interest rates like tapering and more. The question becomes, at what point is action going to be taken?

As the Fed testified in Congress yesterday and today, interest rates fell and the price action seemed anything but typical following Wednesday’s poor 30-year bond auction. We get it, the markets are addicted to low interest rates, but unless hyperinflation is the goal, it feels like something needs to change soon. When will the Fed begin tapering bond buying? How about some incremental tapering or very fractional interest rate increases such as an eighth of a percentage point or something? If something doesn’t change soon, we could be heading for a 1981 style inflationary environment. Rates are going to have to rise, and the stock market is not going to like it. However, action needs to be taken.

Will the US equity markets be able to maintain their upward trajectory?

All of this stimulus, decade-plus near-zero interest rates, bond buying, and market addiction to easy monetary policy will have repercussions eventually.

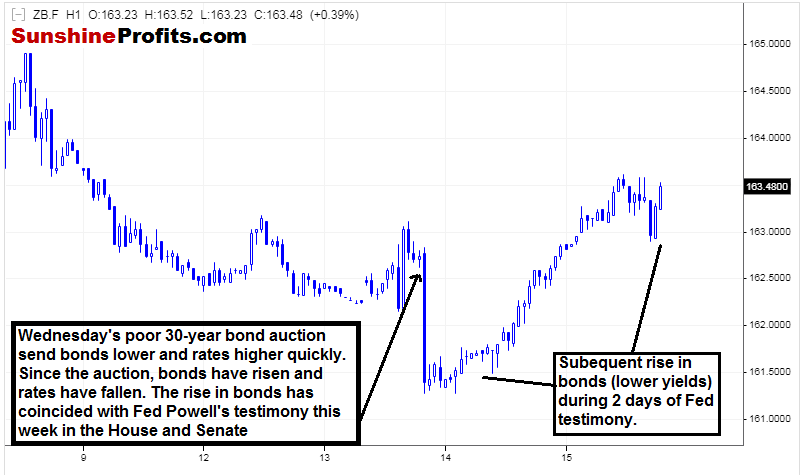

Since we have been analyzing TLT, let’s take a look at the 30 Year Bond Futures:

Figure 1 - U.S. Treasury Bond Futures July 8, 2021 - July 15, 2021, 1 Hour Candles Source stooq.com

The puzzling price action (or perhaps not so puzzling in retrospect given the 2-day Fed testimony) is the creep higher after the weak demand shown in Wednesday’s 30-year bond auction. If you were short bonds at this time via TLT or any product, things were looking good. Since that auction, we had the Fed testimony, which showed many select congress members pleading for interest rates to be kept low. Unfortunately, if rates remain at rock bottom levels, it seems like inflation could spiral out of control. This continued inflation would be bad for the American people.

It is unusual price action; to say the least. The 30-year bond auction was priced at 2%, and demand was extraordinarily weak. There is a solid explanation of this most recent bond auction on Barrons.

However, today, we have 30-year bonds catching a bid near 1.94%. Yes, it is illogical. Yes, markets can be illogical for extended periods.

Looking at the 30-year bond from a perspective of yield:

Figure 2 - U.S. 30 Year Treasury Bond Yield July 7, 2021 - July 15, 2021, 1 Hour Candles Source stooq.com

Fed’s James Bullard, Federal Reserve Bank of St. Louis President urged for tapering of bonds earlier today.

At the time of writing, we have the bonds continuing to be bid with the $SPX moving lower. The message of the market is exhibiting signs of change in my eyes. I don’t want to sound any overall warning bells just yet, but I am tuned in all day, every business day.

Thank you.

Rafael Zorabedian Stock Trading Strategist

Sunshine Profits: Effective Investment through Diligence & Care

* * * * *

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.