This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

AT-A-GLANCE

- QE tends to suppress volatility in financial markets

- Balance sheet shrinkage risks increasing implied volatility

- Equity index options implied volatility rose sharply during the 2017-19 reverse-QE

- Gold, U.S. Treasury Long Bond options have been muted to the prospect of Fed tightening

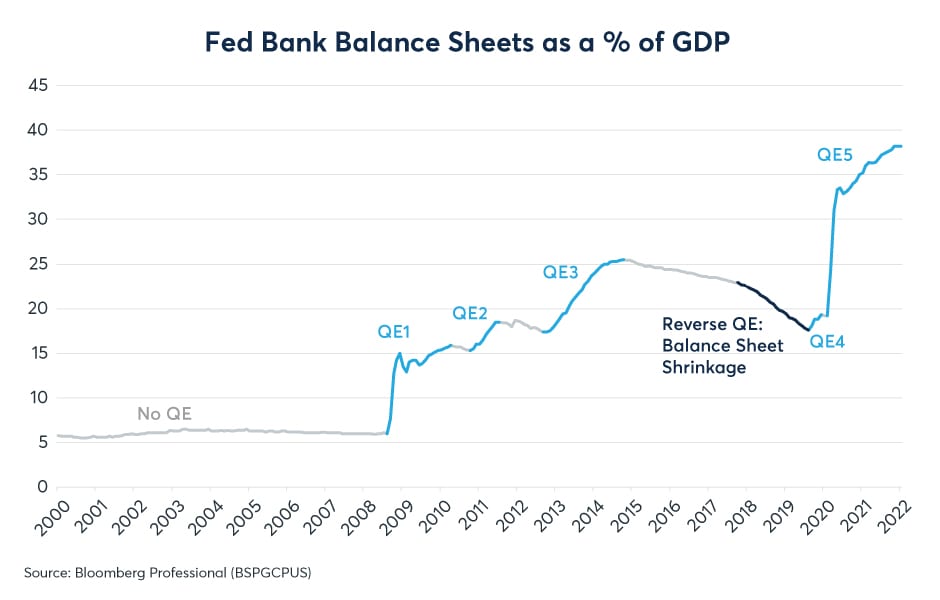

Since the pandemic began the U.S. Federal Reserve (Fed) has increased the size of its balance sheet by $4.7 trillion to $8.86 trillion. The expansion, caused by quantitative easing (QE) to bolster the economy, could come to an end in March as the Fed stops asset purchases, and could soon thereafter begin to shrink its balance sheet. At its January meeting the Fed stated, “It will soon be an appropriate time to raise rates,” and suggested that the process of shrinking the balance sheet could begin soon after.

This isn’t the first time that the Fed has reversed QE. It announced a similar program in September 2017 that continued through 2018 and much of 2019 (Figure 1). While its various QE programs between 2009 and 2014 were generally associated with falling levels of implied volatility across markets, its 2017-19 balance sheet shrinkage coincided with (or, perhaps, helped to cause) a period of rising volatility, whose impact was especially noticeable in the equity index options markets.

Figure 1: After three rounds of QE from 2009-14, the Fed began shrinking its balance sheet in late 2017

The 2017-19 reverse-QE was fairly moderate. As the bonds in its portfolio reached maturity, the Fed reinvested only a portion of the proceeds through new purchases further out on the yield curve. Over a period of 20 months this reduced the size of its balance sheet by $700 billion to $3.7 trillion. In its January 2022 statement the Fed suggested a similarly “predictable” approach could be used soon after it begins raising rates. This time, the Fed’s balance sheet is not only much larger, but its average bond maturity is also somewhat shorter. Moreover, there has been discussion of reinvesting a smaller proportion of the receipts from maturing bonds than the Fed did the last time. This holds open the possibility of a faster reduction in the size of its balance sheet.

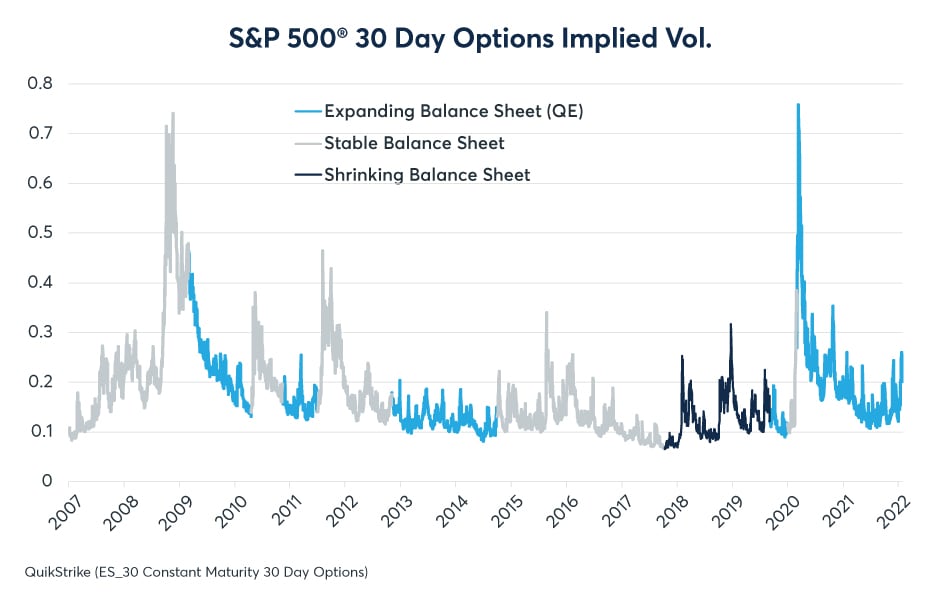

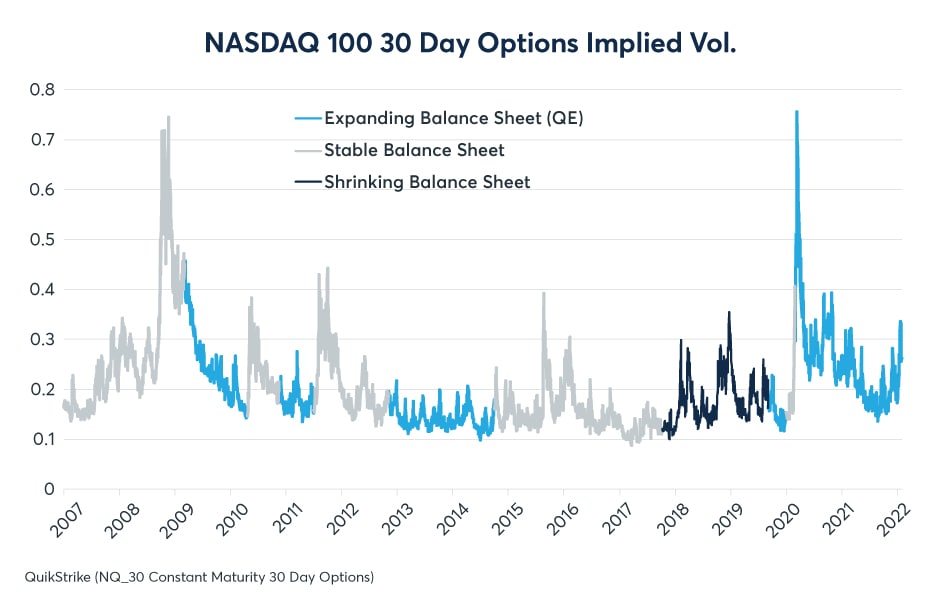

The mere prospect of the Fed tightening policy appears to have played a role in raising volatility in recent weeks, notably for equity index options but also for 30Y bond options. Equity index options such as those on the S&P 500® and the Nasdaq 100 tended to fall sharply during periods of QE but trended higher during the Fed’s 2017-19 reverse-QE (Figures 2 and 3).

Figure 2: QE tends to supress volatility; reversing QE tends to revive it

Figure 3: Nasdaq 100 implied volatility began to rise with the prospect of tighter Fed policy

The current round of QE halted the spike in implied volatility quickly in March 2020 and volatility trended lower until mid-2021 when rising inflation began to tilt monetary policy expectations back in the direction of a Fed tightening. As inflation soared to 7% in late 2021, implied volatility began rising, most likely in anticipation of a Fed policy tightening. With equity valuations near historically high levels, the prospect of tighter policy creates a variety of concerns for equity investors including the possibility of slower profit growth going forward as well as higher rates at which to discount future cash flows.

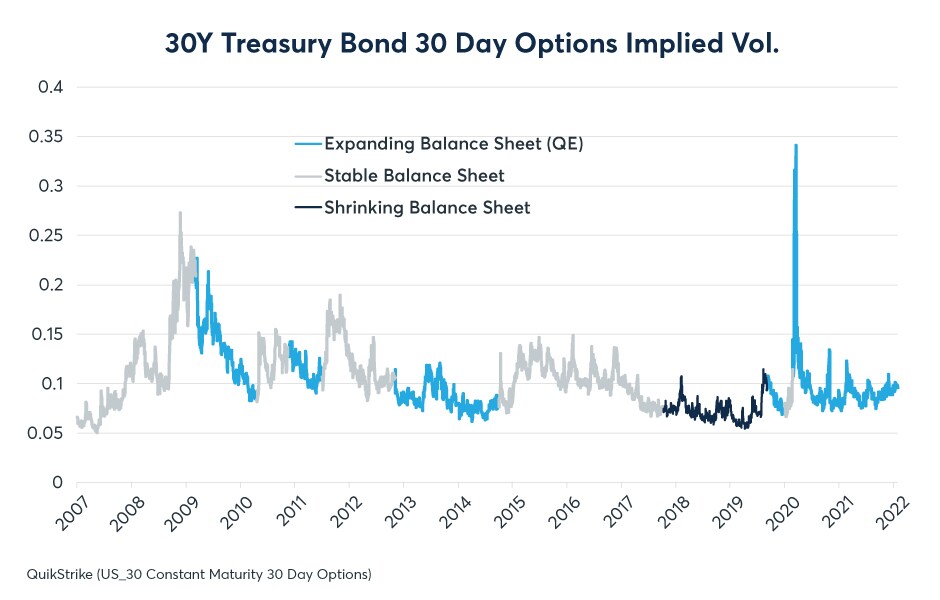

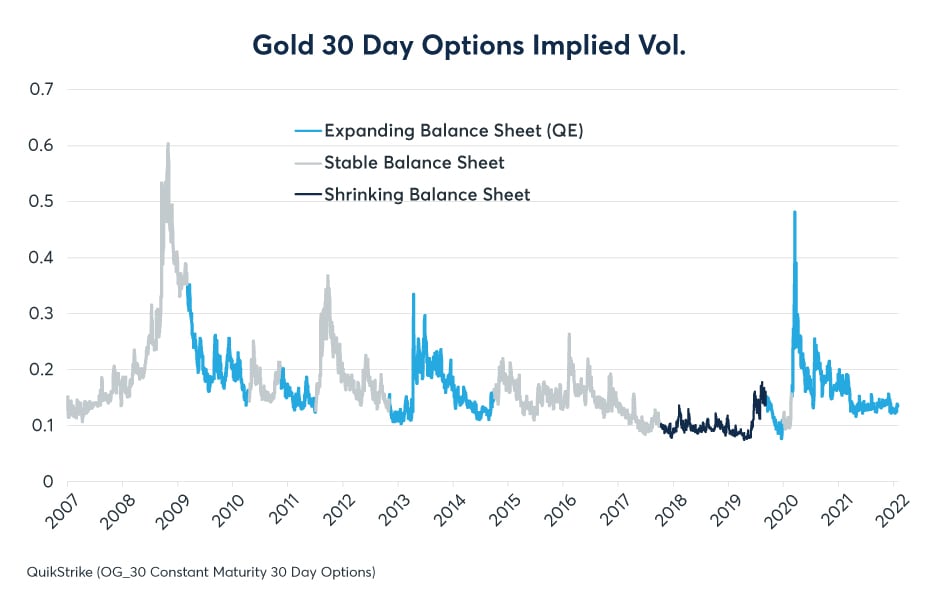

For other options markets such as U.S. Treasury Long Bonds (30Ys) and gold, the relationship between balance sheet shrinkage and implied volatility is not quite as clear. Even so, for these markets implied volatility has tended to fall during periods of QE while usually trending sideways, and sometimes higher, during periods of balance sheet stability and shrinkage (Figures 4 and 5).

Investors in long-term U.S. Treasuries might, in fact, be comforted by Fed tightening. While the prospect of Fed rate hikes creates volatility in short-term interest rate markets, the effects are often muted further up the curve as investors see tighter monetary policy as helping to anchor long-term inflation expectations. As such, implied volatility on U.S. Treasury Long Bonds options has shown a muted response to the recent equity market volatility thus far.

Figure 4: Treasury options showed less reaction to the 2017-19 balance sheet shrinkage

Figure 5: Gold options implied volatility eventually rose at the end of the last balance sheet shrinkage

Gold options have also been relatively stable in recent weeks as well. For its part, the yellow metal appears to be caught in a tug of war. On the one hand, rapidly rising inflation in the U.S. and Europe should, in theory, raise its value with respect to fiat currencies such as the U.S. dollar (USD). At the same time, however, as a non-interest-bearing asset, investors tend to avoid gold when they come to expect higher short-term interest rates on their USD deposits. Amid these countervailing forces, gold has been trading in an increasingly narrow trading range and this lack of realized volatility (and trend) may be behind the options market’s lack of response to the prospect of tighter U.S. monetary policy.

Although bond and gold options have not joined equity index options in their trend towards rising implied volatility, the fact of an economy that remains seriously out of kilter (7% inflation, disrupted labor markets and ongoing supply chain issues), might put them at risk of a volatility spike later in 2022. If QE helps to suppress volatility then the risk is that balance sheet shrinkage could increase it.

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.