Long-term investors in the S&P 500 may be tempted to buy out-of-the-money put options to hedge against further downside losses during an extended bearish period. But has this historically been a good strategy? Is the protection worth the premium?

Put Options Are Expensive and Poorly Timed

As an options broker for 15 years, I bought plenty of put options for customers aiming to hedge a long-term portfolio of stocks like SPY. From cursory account encounters, and in many instances, these options didn't provide the protection investors sought. As Roni Israelov found in his 2017 paper, using put options over an extended period to protect a long-term investment in the S&P 500 has turned out to be a waste of time and money (Israelov, 2017).

For the sake of argument, we’ll discuss SPDR S&P 500 ETF Trust (SPY) instead of SPX, since SPX options do not offer a tradeable underlying asset, whereas SPY closely tracks the S&P 500 and is widely used by investors.

SPY: Fundamental Insights

The SPDR S&P 500 ETF Trust (SPY) is one of the largest and most widely traded exchange-traded funds, with assets under management (AUM) exceeding $600 billion. Its primary objective is to track the performance of the S&P 500 Index. By mirroring the index, SPY offers broad diversification across industries and sectors.

Historically, SPY has delivered robust long-term returns, closely tracking the S&P 500’s growth. Over the past decade, SPY has achieved an annualized return of 11%, outperforming many actively managed funds.

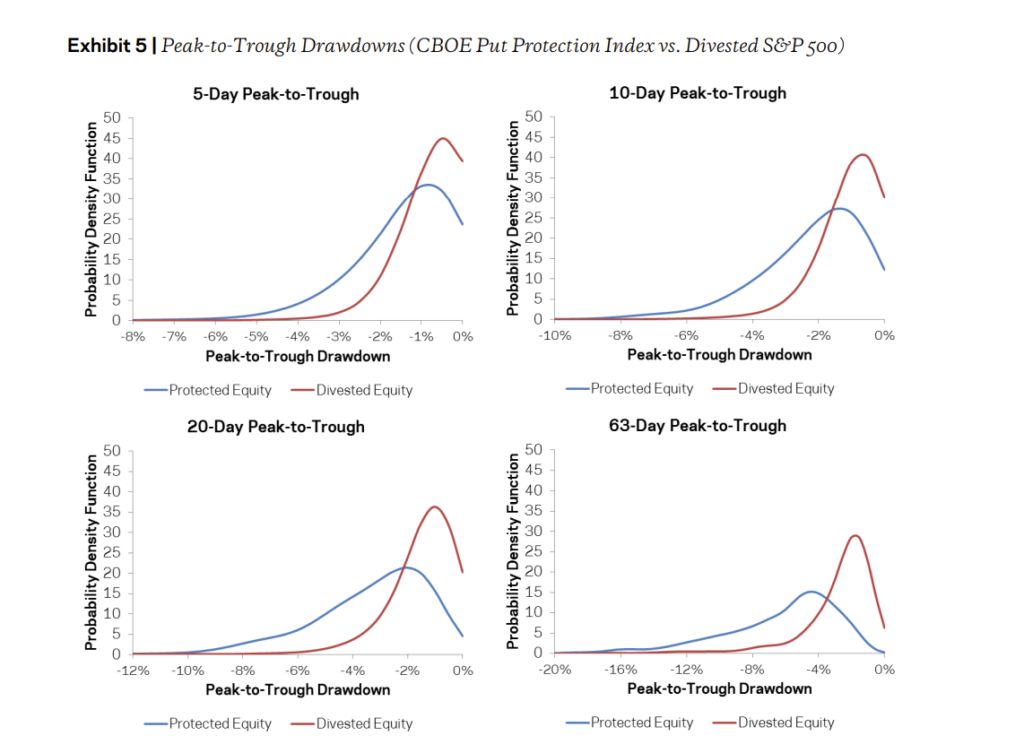

Put Options: Expensive & Poorly Timed

If you knew exactly when a market drawdown would occur and how severe it would be, then buying put options as a tactical hedge against poor SPY performance would make sense. But since we don't have a crystal ball, maintaining continuous protection over time means constantly buying new puts—a costly, inefficient strategy that acts as a constant drag on your account.

Buying puts after a volatile event doesn't typically work either because the premium you pay will be dramatically higher than before vol spiked. It's like trying to buy car insurance while sliding down the highway toward an 18-wheeler—the insurance company will charge you an arm and a leg.

Puts May Increase Volatility

Most investors assume protective puts reduce volatility—but paradoxically, they can actually increase it. Protective puts introduce time-varying equity exposure, meaning the portfolio's risk level fluctuates depending on whether the puts are in or out of the money. This added variability can actually make a portfolio more volatile, sometimes worsening peak-to-trough drawdowns rather than mitigating them.

Israelov's research also found that simply reducing portfolio exposure during extended bear markets provides superior downside protection to buying puts—while, interestingly, maintaining the same expected return.

His study showed that the CBOE S&P 500 5% Put Protection Index performed worse than a portfolio that simply held less stock and more cash. In other words, you don't need to pay for expensive protection when holding less stock achieves the same result for free. This argument is even more convincing in 2025, as interest rates are considerably higher than they were in 2017, giving cash positions more bang for the buck.

Puts Fail to Hedge Against Prolonged Bear Markets

Buying puts on SPY can provide protection against sudden, unexpected market crashes, like the COVID selloff or the volatility of the past few weeks. But the problem is that most drawdowns don't happen overnight—they unfold over months or years. Puts might help in extreme crashes, but they're an expensive and unreliable hedge for most bear markets that only experience moderate volatility.

What About 2025?

Eight long, volatile years have passed since Israelov published Pathetic Protection: The Elusive Benefits of Protective Puts. So—does his thesis still hold up?

The article was written in a low-interest-rate environment, but rates have skyrocketed in recent years. Meanwhile, the VIX has seen more dramatic spikes, with major surges during the COVID-19 crash (2020), inflationary turmoil (2022), and recent geopolitical and economic uncertainty.

It's also worth thinking about SPY's evolution over the years – an increasing weight in tech giants that's nearly 20% of SPY's exposure in just three stocks. This concentration means that SPY's risk profile has changed, potentially reducing the impact of broad-market SPY hedges. For example, the current weighting of the top three holdings are:

- Apple (AAPL): 7.05% weighting

- Microsoft (MSFT): 6.98% weighting

- Nvidia (NVDA): 5.64% weighting

This concentration results in nearly 20% of the ETF’s exposure resting on just three stocks. While these tech giants have driven significant returns, their dominance increases risk in the event of sector-specific downturns.[MM1]

The options market has also exploded, with shorter expiration cycles flooding option chains and 0DTE (zero-day-to-expiration) options now widely traded. While this enhances liquidity and expands tactical hedging opportunities, it does little to alter Israelov's argument materially.

If anything, these shifts in market structure further reinforce his conclusions:

- Options are still expensive when you need them most.

- They fail to hedge against prolonged drawdowns.

- Simply reducing equity exposure still offers better downside protection, particularly with today’s elevated interest rates.

Buying put options to protect a portfolio is an expensive and ineffective strategy over the long run. While puts may provide short-term relief during extreme market events, they fail to consistently reduce drawdowns due to inevitable poor timing, high costs, and path dependency.

Source

- Israelov, Roni. Pathetic Protection: The Elusive Benefits of Protective Puts. The Journal of Financial Economics, 2017. Available at SSRN: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2934538

- Take note that Israelov determines how far the put options should be out of the money based on the time until expiration:

- 20-day options: 4.8% out of the money

- 63-day options: 9.2% out of the money

- 250-day options: 18.2% out of the money

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.