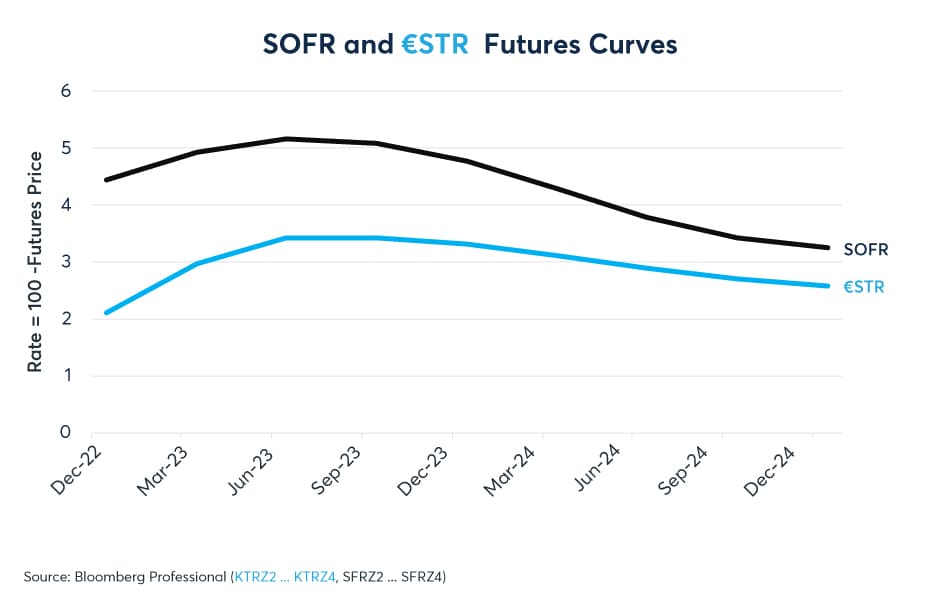

For the moment, Euro Short-Term Rate (€STR) futures are looking a great deal like the Secured Overnight Financing Rate (SOFR) and Fed Funds Rate. What all three futures markets have in common is that after a period of dramatic tightening by the European Central Bank (ECB) and Federal Reserve (Fed), they are pricing one, or more likely two, 25-basis-point (bps) rate hike(s), to be followed by a long period of rate reduction as of this writing. In the case of SOFR, investors are pricing 200 bps of Fed rate cuts after a peak at around 5% (rates are 4.5%-4.75% currently). In the case of €STR, investors are pricing the likelihood of 75-100 bps in rate cuts after hikes of 25-50 bps in Q1 (Figure 1).

Figure 1: SOFR, ESTR both price hikes of 25bps (or so) followed by Fed, ECB rate cuts

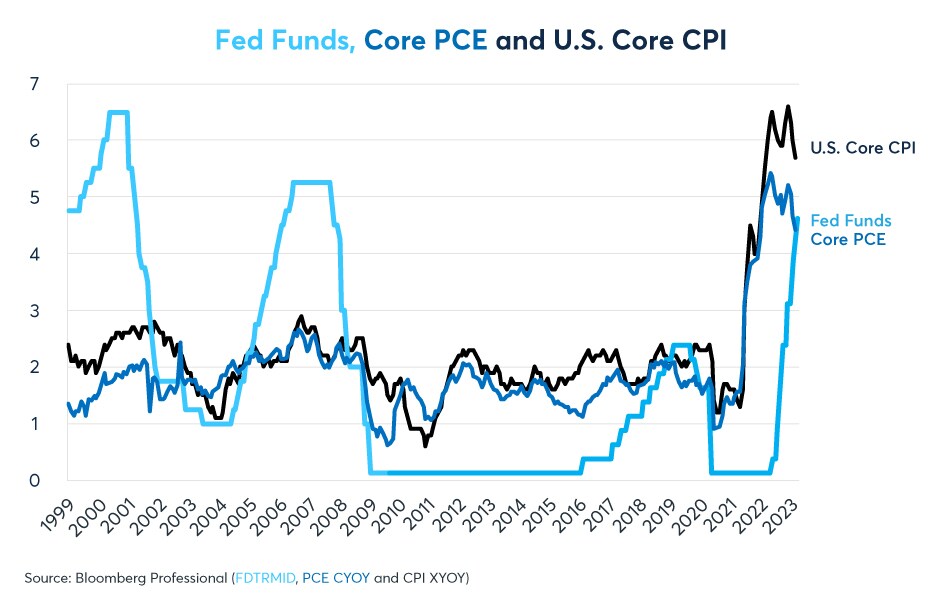

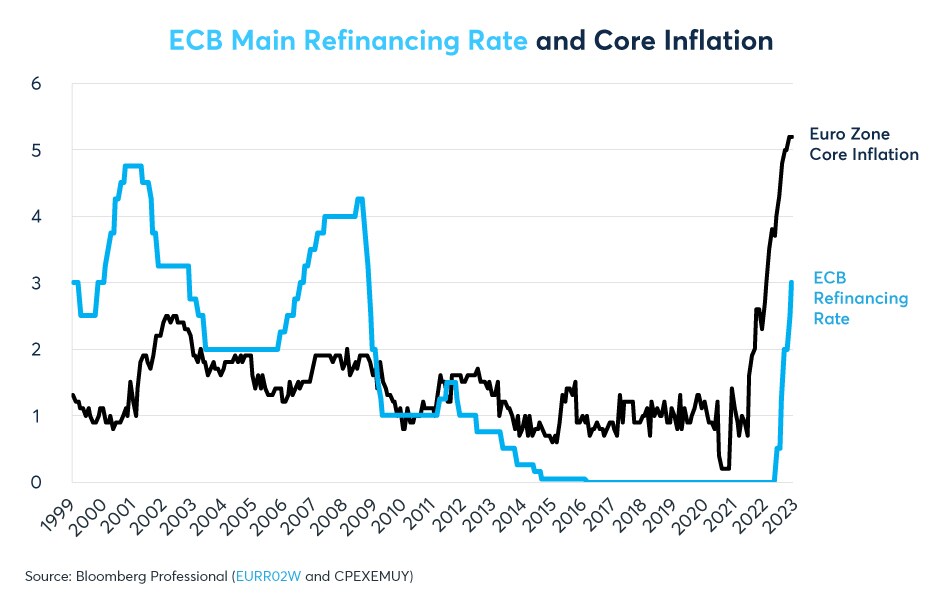

What is curious about this pricing is: In the U.S., after 450 bps of rates rises, the Fed funds rate is now within 1% of U.S. core-CPI (Figure 2) and is above the Fed’s preferred measure of inflation, core PCE, or personal consumption expenditures. By contrast, the ECB, despite 300 bps of rate hikes, still has its main refinancing rate 220 bps below eurozone core inflation (Figure 3). On the one hand, the fact that the ECB’s main refinancing rate is still so far below the level of core inflation might suggest that the ECB has much further to go in terms of raising rates than the Fed. But that’s not what €STR is pricing. On the other hand, more deeply negative eurozone real rates may explain why investors don’t see the ECB cutting rates as deeply as they see the Fed reducing rates in late 2023 and in 2024.

Scan the above QR code for more expert analysis of market events and trends driving opportunities today!

Figure 2: Fed Funds are currently just 100 bps below core-CPI

Figure 3: ECB rates are still 220 bps below the level of eurozone core-CPI

Additionally, investors are also pricing a lower long-term equilibrium interest rate for €STR than SOFR. For example, as of February 7, 2023, December 2024 €STR futures traded at a rate of 2.55%, whereas December 2024 SOFR futures traded at 3.23%. There are several possible explanations. For starters, eurozone core inflation is about 0.5% below that of the U.S. based on their respective CPI measures. That said, U.S. core inflation appears to have already crested, and has now begun to decline. By contrast, eurozone core inflation was still at its highest point at the end of January.

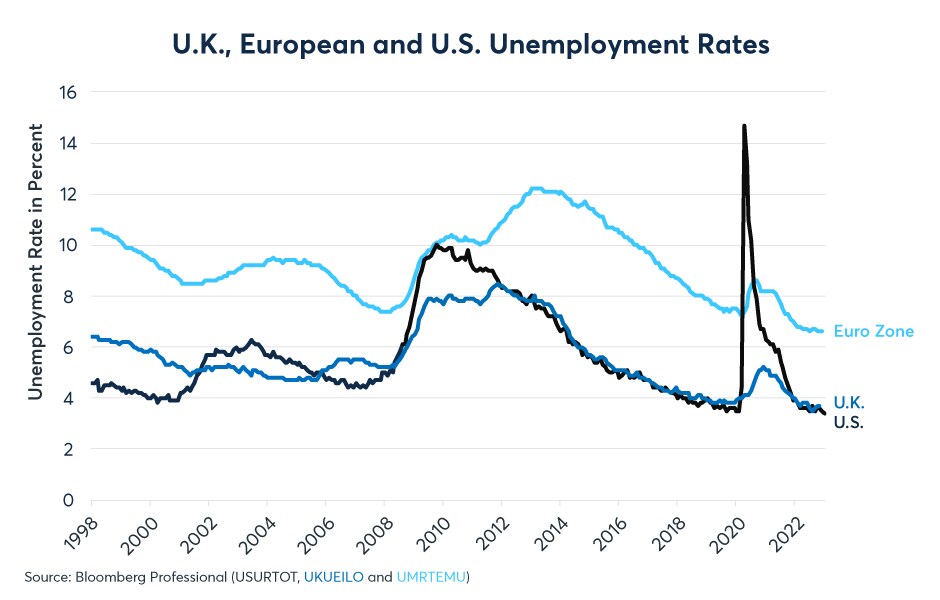

It may also be that labor markets are not as tight in Europe as in the U.S, where unemployment has fallen to a 53-year low of 3.4%, and employers are still listing an additional 11 million open positions, according to the latest JOLTS survey. By contrast, eurozone unemployment is 6.6%, nearly twice the U.S. level. Here, too, however, there are complications. Compared to their pre-pandemic lows, U.S. unemployment has fallen by only 0.1%, from 3.5% at its lowest in 2019 to 3.4% today. In the eurozone, unemployment is now 0.6% lower than it was pre-pandemic, having fallen from a low of 7.2% in 2019 to today’s 6.6%, which is the lowest since Eurostat began recording the data in 1998 (Figure 4). Moreover, Europe has a higher level of structural unemployment than the U.S. owing to labor regulations in southern European countries like France, Greece, Italy, Portugal and Spain that render employment markets less flexible and dissuade employers from taking the risk of adding staff.

Figure 4: Eurozone unemployment is higher than in the U.S. but at a record low for the region

What remains unclear in both the U.S. and in Europe is the extent to which historically low rates of unemployment are propelling inflation. In both places, the so-called Phillips curve, which relates the level of unemployment to the rate of inflation, was exceptionally flat pre-pandemic. From 1993 to 2019, it didn’t seem to matter if unemployment was high or low, either way core inflation ran at about 2% in the U.S. and around 1% in Europe. It was more of a Phillips pancake than a curve. Estimating the curve post-pandemic isn’t yet possible for lack of sufficient data. However, investors in both the U.S. and Europe seem to think that either:

- The Phillips curve will be pretty flat and that tight labor markets won’t cause a permanent rise in inflation, or

- Central banks will contain inflation by causing a downturn in labor markets.

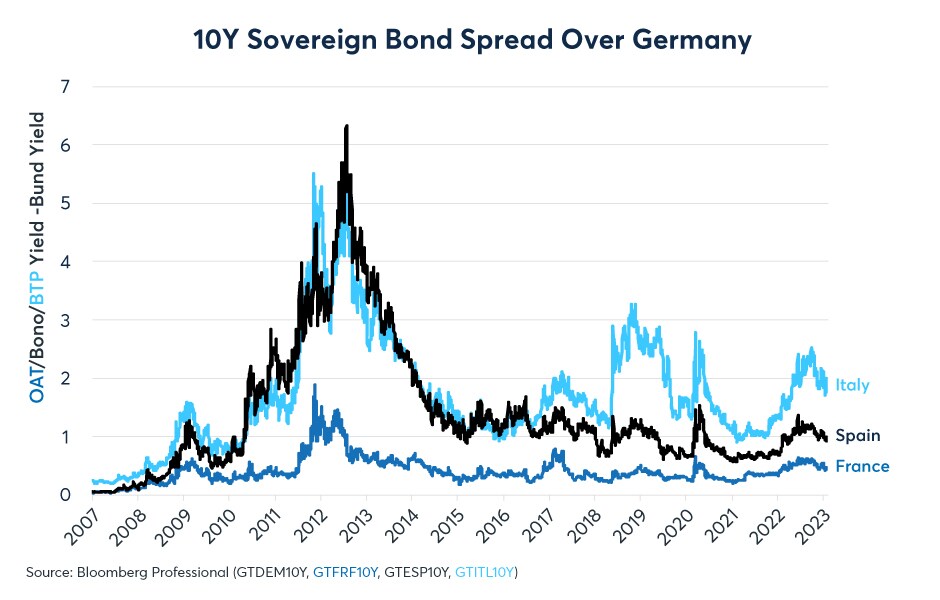

There may be one final reason why €STR futures are pricing a lower equilibrium level of rates for Europe than SOFR does for the U.S.: the memory of the 2008-2012 eurozone crisis. Following the ECB’s 2005-2008 tightening cycle and the onset of the global financial crisis, sovereign spreads widened dramatically within the eurozone, pushing Greece into default and nearly doing the same for Portugal, Ireland, Italy and Spain. For the moment, intra-European spreads (measured relative to the German Bund), have not widened dramatically, but the possibility does exist given the ECB’s 300 bps of rate increases (Figure 5).

Figure 5: Intra-European spreads widened in 2022 but not to 2011-12 levels

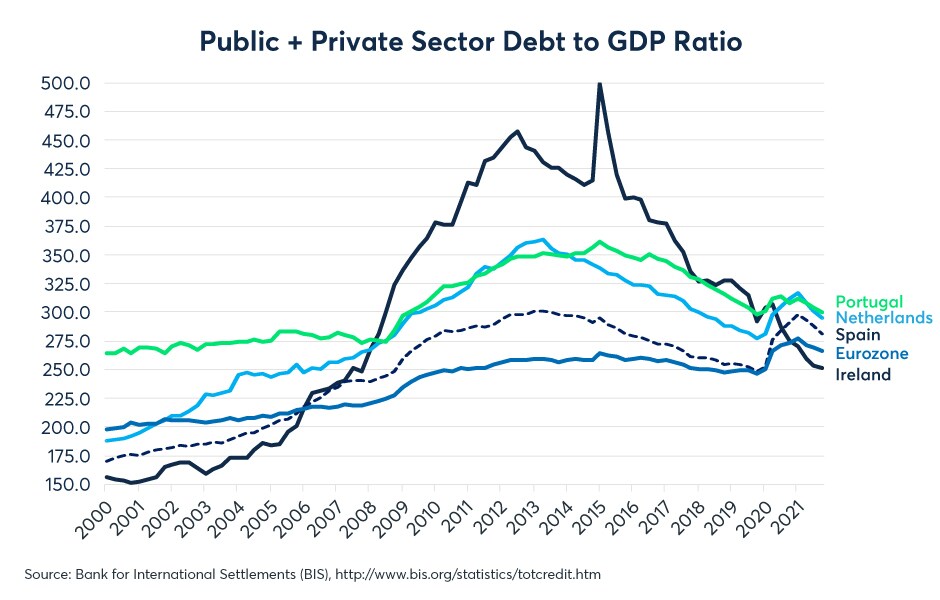

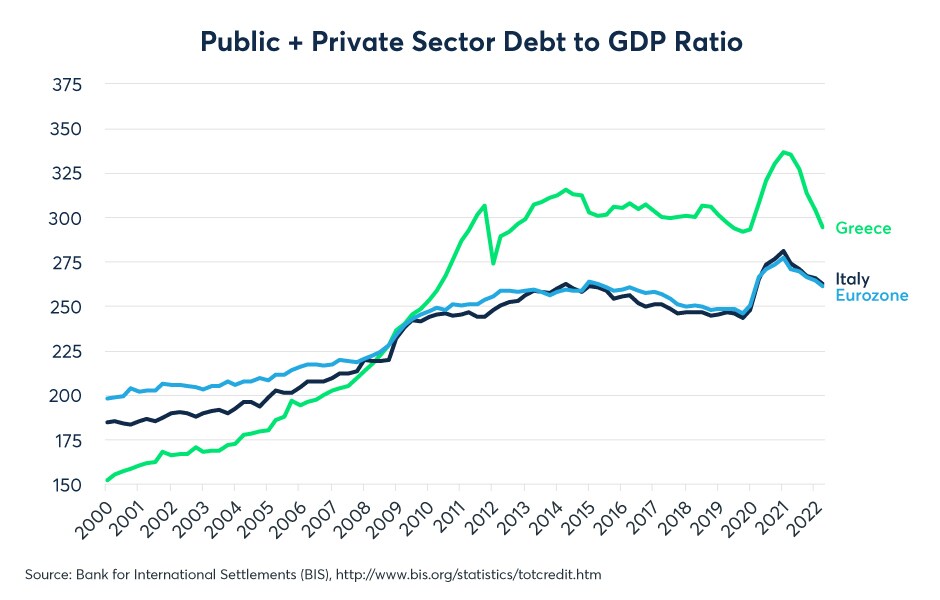

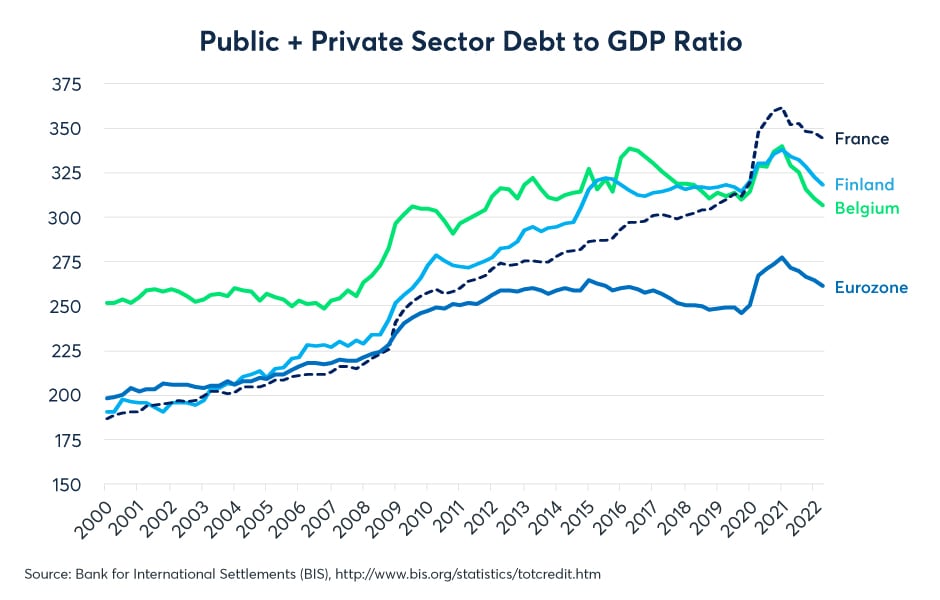

Some of the hardest hit nations during the previous eurozone crisis have been deleveraging. Ireland, Portugal and Spain, for example, have spent the past decade on a massive debt reduction campaign (Figure 6). However, Greece and Italy have not substantially changed their leverage ratios and may still be vulnerable to a re-widening of sovereign spreads within the zone (Figure 7). Finally, other nations, notably Belgium, Finland and France have seen sharp increases in their leverage ratios over the past decade (Figure 8). France is second only to Japan in terms of debt ratios, with public and private sector debt totalling over 350% of GDP. But the difference is that Japan is a single sovereign issuer emitting debt into a currency that it’s central bank controls. By contrast, France, like its eurozone peers, issues debt into a common currency and has no direct control over its central bank.

Figure 6: Some of the eurozone nations used the period of low rates to deleverage

Figure 7: Greek and Italian debt ratios haven’t changed much since 2010

Figure 8: Belgium, Finland and especially France have levered up on debt

For France and its eurozone peers, it didn’t matter much how high debt levels were when interest rates were stuck at zero. However, now that they have soared to 3% and seem likely to continue to rise a bit further, servicing the debt could become an issue. This fear of a second eurozone crisis may explain, in part, why €STR futures are not pricing ECB rates to match or exceed those of the Fed even though ECB rates remain far below the level of core inflation.

Image sourced from Shutterstock

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.