After being the only one to finish 2016 in the red, the healthcare sector made a comeback in 2017 and finished the year up 21.7%, barely lagging the S&P 500’s (SPX) 21.83% increase. It’s still early in the year, but so far the sector’s performance has been in line with the SPX.

As is often the case, that could change once Q1 earnings season gets underway next month. For the quarter, the S&P 500 healthcare sector is expected to report 9.5% earnings growth and 6.5% revenue growth, according to FactSet. The projected earnings growth for the sector has increased over the past several months and back on Dec. 31, it was only 4.5%.

There are a few companies that have yet to confirm their earnings release dates. Here are some of the third-party consensus analyst estimates for ones that have announced their reporting dates:

- Johnson & Johnson JNJ reports before market open on Apr. 17. JNJ is expected by Wall Street consensus to report adjusted earnings per share (EPS) of $2.01 on revenue of $19.38 billion, compared to $1.83 on revenue of $18 billion in Q1 2017.

- Eli Lilly and Co LLY reports before market open on Apr. 24. Based on Wall Street consensus estimates, LLY is expected to report adjusted EPS of $1.13 on revenue of $5.47 billion, compared to $0.98 on revenue of $5.23 billion in Q1 2017.

- Merck & Co., Inc. MRK reports before market open on May 1. MRK is expected to report adjusted EPS of $0.98 on revenue of $9.94 billion, compared to $0.88 on revenue of $9.43 billion in Q1 2017

- CIGNA Corporation CI reports before market open on May 3. CI is expected to report adjusted EPS of $3.38 on revenue of $11.02 billion, compared to $2.77 on revenue of $10.34 billion in Q1 2017.

These are third-party consensus analyst estimates for some of the major healthcare companies that have yet to confirm earnings release dates (most are expected to report in mid-to-late April and early May):

- AbbVie Inc ABBV is expected to report adjusted EPS of $1.78 on revenue of $7.56 billion, compared to $1.28 on revenue of $6.54 billion in Q1 2017.

- Celgene Corporation CELG is expected to report adjusted EPS of $1.99 on revenue of $3.49 billion, compared to $1.68 on revenue of $3.04 billion in Q1 2017.

- CVS Health Corp CVS is expected to report adjusted EPS of $1.40 on revenue of $45.82 billion, compared to $1.17 on revenue of $44.51 billion in Q1 2017.

- Gilead Sciences, Inc. GILD is expected to report adjusted EPS of $1.61 on revenue of $5.39 billion, compared to $2.23 on revenue of $6.51 billion in Q1 2017.

- Pfizer Inc. PFE is expected to report adjusted EPS of $0.73 on revenue of $12.9 billion, compared to $0.69 on revenue of $12.78 billion in Q1 2017.

- United Health Group (UNH) is expected to report adjusted EPS of $2.92 on revenue of $54.85 billion, compared to $2.37 on revenue of $48.72 billion in Q1 2017.

Looking back at Q4 2017, 84% of the companies in the S&P 500 healthcare sector reported earnings above estimates, 5% were in line with estimates, and 11% came in below, according to FactSet.

HEALTHCARE SECTOR SINCE START OF 2018. The chart above shows the S&P 500 Healthcare Select Sector Index (IXV, orange line), compared to the S&P 500 (SPX, purple line) and the Nasdaq 100 (NDX, teal line). So far this year, the IXV’s performance has been in line with the SPX, but it has lagged the NDX by just under 5%. Chart source: thinkorswim® from TD Ameritrade. Not a recommendation. For illustrative purposes only. Past performance does not guarantee future results.

Volatility in Insurance and Providers

One of the big things that happened early on in the year was Amazon.com, Inc. AMZN, Berkshire Hathaway BRK, and JPMorgan Chase & Co. JPM announcement on Jan. 30 that the three would be teaming up to address U.S. employee healthcare. At the time, JPM CEO Jamie Dimon said “our goal is to create solutions that benefit our U.S. employees, their families, and, potentially, all Americans.”

Those aren’t exactly three companies you want to hear are entering your industry, especially when there are few details about the new partnership that the three said will be “free from profit-making incentives and constraints.” Following the announcement, shares of insurance providers (see below) were sharply lower, and other healthcare companies including CVS Health (CVS), Walgreens Boots Alliance Inc WBA and drug wholesaler AmerisourceBergen Corp. ABC, among others, also took a hit. One thing that remains to be seen is whether or not all of this will end up spilling over into other parts of the sector.

On top of the volatility driven by competitive pressures, drug pricing and other regulatory concerns have continued to come up from time to time, adding to some of the knee-jerk market swings.

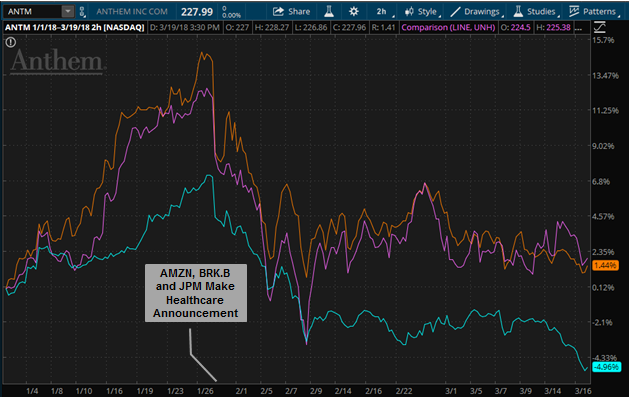

VOLATILITY IN HEALTHCARE An announcement on Jan. 30 from Amazon (AMZN), Berkshire Hathaway (BRK.B) and JPMorgan Chase (JPM) sent insurer stocks and other healthcare companies lower. The chart above shows Anthem (ANTM, orange line), United Healthcare (UNH, purple line) and Aetna (AET, teal line). Chart source: thinkorswim® from TD Ameritrade. Not a recommendation. For illustrative purposes only. Past performance does not guarantee future results.

M&A: Getting Bigger and Replenishing Pipelines

There were several major deals blocked by regulators in early 2017 on antitrust grounds. Insurers Aetna Inc AET and Humana Inc HUM merger got a no after a few years of trying, and Anthem (ANTM) and Cigna (CI) also got a no. Now, there are more deals in the works.

CVS Health (CVS) announced in December it had agreed to acquire AET for $69 billion. That deal is still under regulatory review and has yet to be approved. CI announced at the beginning of March that it had entered a definitive agreement to acquire pharmacy benefits manager Express Scripts for $52 billion. CI said it expects the deal to close before Dec. 31, 2018, pending regulatory approval.

While insurers and other healthcare companies have been looking to integrate, the drugmakers have been looking to replenish their pipelines. There’s been a couple of deals on the larger side in biotech since the start of 2018. On Monday, Jan. 22, French drugmaker Sanofi announced it would buy Biogen-spinout Bioverativ (BIVV) for $11.6 billion. The same day, Celgene (CELG) announced it would acquire Juno Therapeutics (JUNO) for $9 billion. Both of those deals closed in early March.

Some analysts interpreted the biotech deals as a sign there would be more M&A in 2018, spurred by tax reform and access to overseas earnings. At the same time, however, other analysts note that lofty valuations in the space might hold back further deals.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.