Intuitive Surgical, Inc. ISRG will report second-quarter 2024 earnings on Jul 18. The Zacks Consensus Estimate for sales and earnings is pegged at $1.97 billion and $1.53 per share, respectively. Earnings per share estimates for ISRG have remained stable at $6.26 and $7.32 for 2024 and 2025, respectively, over the past 60 days.

Estimate Movement

Image Source: Zacks Investment Research

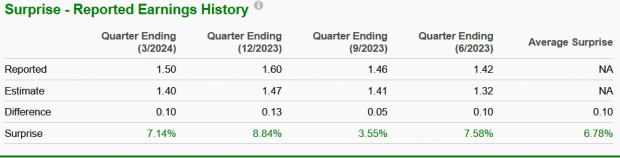

In the last reported quarter, ISRG delivered an earnings surprise of 8.84%. Its earnings beat estimates in each of the trailing four quarters, delivering an average surprise of 5.83%.

Image Source: Zacks Investment Research

Earnings Whisper

Our proven model does not conclusively predict an earnings beat for ISRG Holding this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. This is not the case here.

ISRG has an Earnings ESP of 0.00% and a Zacks Rank #2 at present.

Factors to Note

The Instruments & Accessories segment is likely to report robust second-quarter results on the back of rising da Vinci procedure volume as seen in the past few quarters. However, an unfavorable currency movement is expected to have partially offset the gains from recovering demand in procedures. Meanwhile, a rise in the proportion of recurring revenues buoys well for ISRG.

Moreover, the recovery in China on the back of strong procedure growth following COVID-related setbacks in the past year is likely to have boosted sales in the soon-to-be-reported quarter.

ISRG reported sales of $1.89 billion in the first quarter, indicating growth of 11% year over year. Per management, da Vinci procedures grew approximately 16% worldwide in the to-be-reported quarter. The company recorded first-quarter sales of $1.16 billion from instruments and accessories, implying a year-over-year improvement of 18%.

However, Intuitive Surgical's da Vinci capital placements are likely to have been on the lower side due to continued supply-chain challenges adversely impacting the availability of semiconductor components and growing capital spending pressure on hospitals amid rising inflationary pressure.

The FDA's approval for the use of ISRG's next-generation da Vinci 5 robotic system in March is likely to have brought additional revenues during the second quarter. On its second-quarter earnings call, the company may provide an update on the launch uptake.

During the first quarter, the company placed 313 systems compared with 312 in the prior-year quarter. Intuitive Surgical's da Vinci capital placements are likely to have benefited from rising demand outside the country. The company placed 165 systems in the first quarter compared with 171 in the prior-year quarter in ex-U.S. markets.

The single port platform's growth is expected to have been driven by additional clinical indications and clearances in markets beyond the United States and Korea. However, System revenues decreased 2.1% to $418 million during the first quarter.

Intuitive Surgical launched its Ion in 2023, beginning with the United Kingdom. The availability of Ion catheters in Europe is likely to have brought additional revenues during the second quarter.

The company may also provide a view on the uptake in the region. ISRG's digital products, like the Intuitive Hub and the recently launched Case Insights, are likely to have shown rising adoption.

However, increased robotic competition and government policy changes in China, higher logistics costs amid supply-chain challenges and rising inflationary pressure are likely to have hurt sales and increased expenses in the to-be-reported quarter.

Price Performance & Valuation

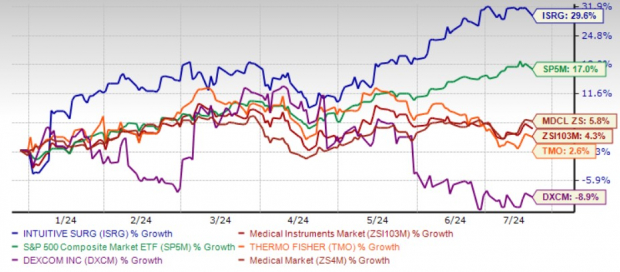

Intuitive Surgical's shares have appreciated 29.6% on a year-to-date basis, significantly above the industry's 4.3% growth. Meanwhile, the company's shares have outperformed the S&P 500 Index's rise of 17% and Zacks Medical sector's growth of 5.8%.

ISRG has also outperformed Thermo Fisher Scientific's TMO 2.6% return and DexCom's DXCM 8.9% decline year to date.

Year-to-Date Price Performance

Image Source: Zacks Investment Research

Now, let us look at the value Intuitive Surgical offers to its investors at current levels.

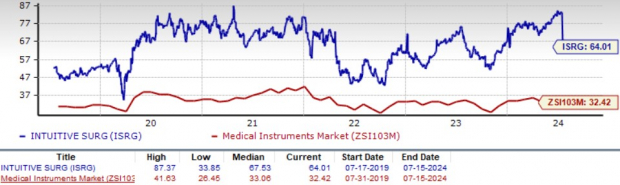

Currently, ISRG is trading at a premium, with a forward 12-month P/E of 64.01X compared with the industry's 32.73X but slightly lower than the median of 67.53X, reflecting a moderately high valuation.

ISRG's P/E F12M Graph

Image Source: Zacks Investment Research

Investment Thesis

Intuitive Surgical is likely to continue with its strong performance in 2024 on the back of continued growth in the company's da Vinci procedure volume, coupled with strong Ion procedure growth. ISRG is also increasing the pricing of procedures that should aid in 2024 sales growth. Improving procedure volume, along with better system placements and services across all markets, should drive top-line growth this year.

The launch of da Vinci SP in Europe and da Vinci 5 in the U.S. market should drive system placements higher. However, ongoing supply-chain constraints, although easing, are likely to hurt the availability of devices. Weakness in bariatric procedures and challenges in China are likely to offset growth in the upcoming quarters.

Conclusion

ISRG's unfavorable Earnings ESP does not indicate any significant move following the earnings result. We believe that investors should not rush into buying the stock now. Although ISRG has a favorable Zacks Rank, the Style Score of D does not reflect a major strength in the stock. The company's high valuation may have factored in the strong fundamentals, including growth in procedures and installed base. Investors should add the stock to their watchlist and track it for cheaper valuation.

While current shareholders should hold their position, new investors should wait for the stock to retract some of its recent gains, providing a better entry point.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.