Zinger Key Points

- Zeta Global shares have risen over 125% year-to-date.

- Technical analysis indicate short term pressure.

- Fundamentals remain strong but analysts don't have a 'buy' consensus.

- Don't face extreme market conditions unprepared. Get the professional edge with Benzinga Pro's exclusive alerts, news advantage, and volatility tools at 60% off today.

Zeta Global Holdings Corp ZETA, a marketing technology company specializing in AI-powered marketing solutions has outperformed the NYSE Composite index in 2024, while its peers have underperformed the market. Based on its fundamental and technical analysis, should you buy, sell, or hold the stock? Here’s what analysts are saying.

Shares of Zeta were up 1.23% at $18.97 per share as of Thursday’s close. The stock was up 125.83% this year outperforming NYSE Composite, which rose by 14.98%.

Its peers, Freshworks Inc FRSH was down 27.26%, and Temenos ADR TMSNY was down 21.52% in the same period.

The technical analysis of daily moving averages indicates a short-term bearish trend.

The stock ended at $18.97 apiece on Thursday. This was below its eight and 50-day simple moving average of $19.52 and $21.69, respectively. However, as per Benzinga Pro data, its current stock price was also lower than the 50-day moving average of $24.42, and its 200-day moving average of $24.42.

This implies that the stock is in a downtrend. On the other hand, the relative strength index of 38.38 suggests the stock’s movement is moderately oversold but still in the neutral zone.

Two Of Zeta’s Clients Merge

Zeta Global stands to benefit from Omnicom’s acquisition of Interpublic. David A. Steinberg, the co-founder, chairman, and CEO of Zeta, in a statement on Dec. 9 said that “We are proud of our extensive relationships with the top Holdcos, including both Omnicom and IPG, and believe that today's announcement is a positive one for the industry and Zeta. Like everyone else, we will be watching closely as this progresses and offer support as needed.”

During its investor summit, Zeta said it can leverage the combined entity’s vast data infrastructure and enhanced financial strength. This presents opportunities for Zeta to deepen AI-powered customer insights, expand scale and reach and accelerate growth.

New Acquisition By Zeta

Zeta Global’s acquisition of LiveIntent is projected to contribute "Vast data assets, direct channel capabilities and premium publisher network to the Zeta Marketing Platform. The integration of LiveIntent into the ZMP will expand gross margins while accelerating the shift of our revenue derived from agency customers to direct channels,” added Steinberg in a statement dated Oct. 8, 2024. This data foundation will further position Zeta to capitalize on the combined Omnicom-Interpublic entity, offering solutions to this major client segment.

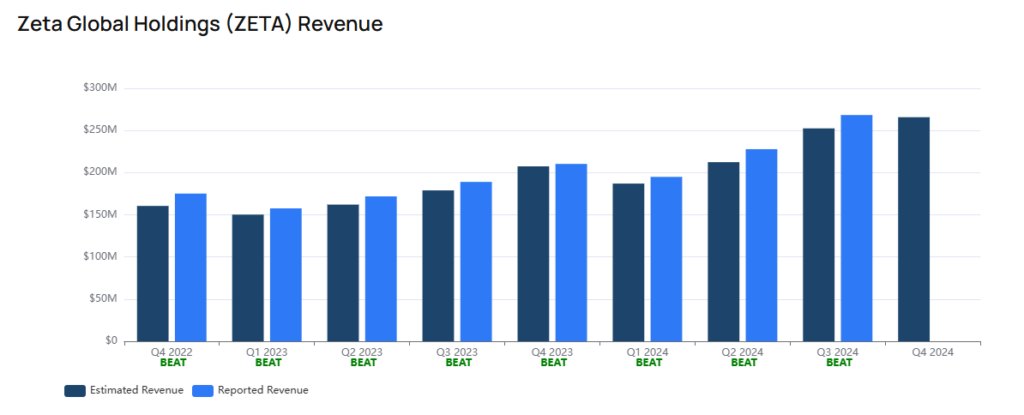

ZETA's Estimated Topline And Bottomline

Benzinga’s estimate for the fourth quarter revenue is pegged at $265.73 million, suggesting 26.34% growth from last year’s topline of $210.32 in the same quarter.

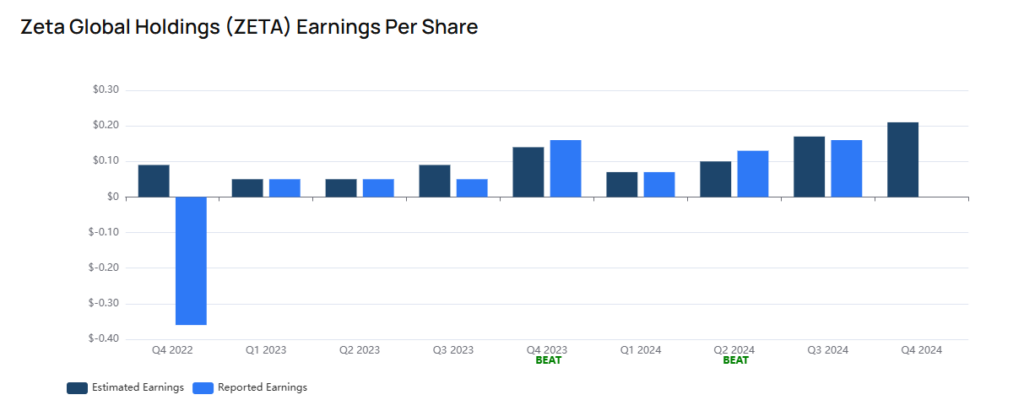

The consensus estimate for earnings in the fourth quarter is pegged at 21 cents per share, as compared to 16 cents in the same quarter of the previous fiscal, suggesting a 31.25% increase from the prior year’s actual.

Zeta Has Higher Liquidity To Meet Obligations

The company had a current ratio of 3.319 at the end of the third quarter, exceeding the industry average of 2.16, according to Benzinga Pro data. This ratio, indicating a robust ability to meet short-term obligations, has surged 67.7% from the previous quarter.

See Also: Should You Buy or Sell This Nvidia Rival? Analysts Weigh In As Technicals Signal A Downtrend

What Are Analysts Saying: According to Benzinga, Zeta has a consensus ‘hold’ with a price target of $32.59 based on the ratings of 17 analysts.

The highest price target out of all the analysts tracked by Benzinga is $45 issued by Craig-Hallum with a ‘buy’ rating on Nov. 12, 2024. Analyst Jason Kreyer highlights Zeta Global’s strong performance, driven by the successful LiveIntent acquisition and cross-selling opportunities. Analyst is positive on the deepening penetration within the existing $100 billion plus customer base by replicating successful high-spend customer relationships.

Goldman Sachs analyst Gabriela Borges initiated coverage on Zeta with a ‘neutral’ rating and announced a price target of $30 apiece. The note highlighted key medium-term risks. Including a possibility of its proprietary data’s value erosion as data accessibility and evolving consumer preferences may diminish, requiring continuous innovation. Strong 2024 performance, partly driven by one-time events, may make year-over-year comparisons challenging in 2025. Also, according to the analyst stricter privacy laws pose a long-term risk to Zeta’s data-driven business model, as evidenced by recent underperformance amid industry scrutiny.

The lowest target price was maintaining a ‘neutral’ from Credit Suisse was adjusted to $9.5 from $12 per share on Aug. 4, 2022. The average price target of $38.67 between Goldman Sachs, RBC Capital, and Needham implies a 105.13% upside for Zeta.

Read Next:

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

date | ticker | name | Price Target | Upside/Downside | Recommendation | Firm |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.