By Peter Atwater

So why was it we believed that you could accurately rate countries in the first place?

During the 2008 banking crisis, we all learned that despite their presumed safety, the triple-A ratings on a mortgage-backed security were only as good as the willingness and ability of the underlying individual borrowers to pay and the ability of the future to replicate some stress-test variation of the past. And, in the aftermath of the banking crisis, with that lesson painfully learned, policymakers and legislators demanded that issuers, underwriters, and the rating agencies do a better job of justifying and detailing to investors the underlying assumptions supporting these investments' ratings.

Yes, securities could be rated triple-A, but everyone needed to better understand all of the conditions' precedent.

At the time, I am sure that policymakers were focused solely on making certain that the issues around the underlying borrowers' ability to pay were disclosed. Homeowners would always pay if they could pay; and of course, homeowners would pay their mortgage first.

Unfortunately, neither is exactly how things are playing out; and we've seen that in real time, with rising strategic defaults in mortgages and the de-correlation of credit card default rates with unemployment and mortgage defaults. (Troubled homeowners are increasingly paying their credit cards first, because first means continued access to food and gas.)

(To read why the Mad Hedge Fund Trader thinks there will be no QE3, click here.)

Unlike “ability," what debt consumers are “willing” to pay today is entirely a function of their own personal confidence, history be damned.

And, at least to date, US consumer bankruptcy laws enable borrowers to make that choice.

What I believe policymakers missed in 2008, and some even now, is that fear causes willingness and ability to decouple. We saw that here first with the advent of strategic defaults at a consumer level, and in March 2010, the decoupling of willingness and ability took a far more serious turn when the people of Iceland voted via referendum to walk away from their obligations to foreign governments arising from the collapse of IceSave.

Not surprisingly, that decoupling of willingness and ability got little attention here. Iceland is a very small country; its banking sector was obviously overleveraged and oversized relative to the domestic economy; and we weren't involved. The “unwillingness” problem was, to borrow a word from the mortgage crisis, “contained." All other nations would continue to honor their obligations unless they were financially unable to.

What we missed then was the same thing we missed in the mortgage crisis. The first post-bubble, Fort Sumter moment always looks contained.

But what people also failed to grasp is that in public finance, there is only strategic default. “Willingness” trumps “ability” every time. As mayor of troubled Harrisburg, Linda Thompson put it to the Wall Street Journal last fall, "To disrupt [services] because we can't make a bond payment would just be unconscionable. And as a leader I couldn't do it...There are always ways to restructure our debt and work out with our debtors, but you can't have trash piling up in your neighborhoods. That's a health issue. You can't have chaos in your communities."

(To read why Satyajit Das thinks there's no way out of Europe's debt crisis, click here.)

That's the difference with public borrowers. It is all about choices, and who gets paid first.

Which brings me to this past week's ratings warnings from Moody's and S&P regarding the U.S.'s triple-A debt rating. Neither rating agency is at all suggesting that the potential downgrade is a function of economic ability. It is all a function of willingness -- political willingness -- and the choices Washington is or is not willing to make.

But please consider that since the agencies put their warnings out there, S&P has put on watch:

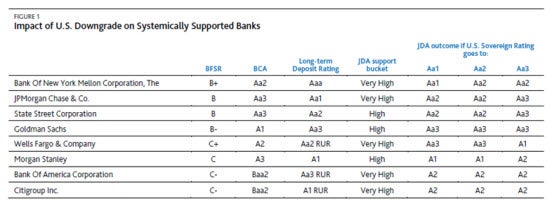

As if Bank of America BAC CEO Brian Moynihan didn't have enough problems, he must now worry about whether Washington is willing to meet its debt obligations!

(To read Peter Prudden's article on monetary stimulus, click here.)

But to step back, it is hard to believe that this level of interconnectivity and interdependence of government, sovereign, and even corporate debt ratings could have existed in the first place if people thought for a second that sovereign willingness to pay would matter more than sovereign ability to pay.

As noted above, sovereign willingness is entirely social mood-based, not financially driven. And there is no contractual obligation that can tie willingness. As we as a nation are now witnessing firsthand in real time, one either is or isn't willing to pay – period. The outcome is binary.

I suspect that in the aftermath of this sovereign debt crisis, economic historians will write volumes on the public bubbles underlying “Big Truth," as I call it, which was: "In developed nations, governments always meet their obligations.”

To read the rest, head on over to Minyanville.

As if Bank of America BAC CEO Brian Moynihan didn't have enough problems, he must now worry about whether Washington is willing to meet its debt obligations!

(To read Peter Prudden's article on monetary stimulus, click here.)

But to step back, it is hard to believe that this level of interconnectivity and interdependence of government, sovereign, and even corporate debt ratings could have existed in the first place if people thought for a second that sovereign willingness to pay would matter more than sovereign ability to pay.

As noted above, sovereign willingness is entirely social mood-based, not financially driven. And there is no contractual obligation that can tie willingness. As we as a nation are now witnessing firsthand in real time, one either is or isn't willing to pay – period. The outcome is binary.

I suspect that in the aftermath of this sovereign debt crisis, economic historians will write volumes on the public bubbles underlying “Big Truth," as I call it, which was: "In developed nations, governments always meet their obligations.”

To read the rest, head on over to Minyanville.

Market News and Data brought to you by Benzinga APIs- AAA' ratings on U.S. insurance groups

- ‘AAA' ratings on three U.S. clearinghouses, one CSD, and select government-sponsored entities (the Federal Home Loan Bank system, Fannie Mae and Freddie Mac among them)

- Navy Exchange Service Command ‘AA/A-1+' ratings

- Marine Corps Community Services ‘AA/A-1+' corporate credit rating

- Army & Air Force Exchange Service ‘AA/A-1+' ratings

- 125 FDIC-guaranteed ‘AAA' rated debt obligations issued by 30 financial institutions under the Temporary Liquidity Guarantee Program (TLGP)

- 8 federal leases and certain power-generation entities linked to the federal government

- 73 of the 206 rated funds managed in the U.S., Europe, and Bermuda

- 604 U.S.-structured finance transactions with an original issuance amount of $373.67 billion

As if Bank of America BAC CEO Brian Moynihan didn't have enough problems, he must now worry about whether Washington is willing to meet its debt obligations!

(To read Peter Prudden's article on monetary stimulus, click here.)

But to step back, it is hard to believe that this level of interconnectivity and interdependence of government, sovereign, and even corporate debt ratings could have existed in the first place if people thought for a second that sovereign willingness to pay would matter more than sovereign ability to pay.

As noted above, sovereign willingness is entirely social mood-based, not financially driven. And there is no contractual obligation that can tie willingness. As we as a nation are now witnessing firsthand in real time, one either is or isn't willing to pay – period. The outcome is binary.

I suspect that in the aftermath of this sovereign debt crisis, economic historians will write volumes on the public bubbles underlying “Big Truth," as I call it, which was: "In developed nations, governments always meet their obligations.”

To read the rest, head on over to Minyanville.© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Loading...

Posted In: PoliticsEconomicsdebt ceilingFinancialsOther Diversified Financial ServicesU.S debt ceiling

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in