Growing competition for user attention, a weaker economy, and rising inflation are all hurdles for social media companies to overcome in the near term. Another hurdle is the resultant market skepticism. However, we believe that there’s more to the social media story as platforms shift their focus from user growth to maximizing and monetizing the time users spend on their platforms. New features and functions, like payments and social commerce, are designed to make these platforms increasingly multipurpose. In our view, these efforts can compound the addressable market for platforms and create ample runway for continued sales and earnings growth. Platforms that continue to execute on this vision can emerge as critical steppingstones for next generation of digital media experiences.

For these reasons, which we discuss in this blog piece, we encourage investors to look beyond the near-term challenges and not overlook, or undervalue, the optionality in the social media space.

Key Takeaways

- User and revenue growth for social platforms pulled forward significantly in 2020 and 2021. As a result, growth is harder to find in 2022, which we believe is weighing down stock performance. However, we believe near-term challenges are likely priced in after the market’s pullback this year.

- Social platforms gaining more user attention is a major contributor to the ongoing erosion of legacy media channels. We expect social platforms can continue to boost user engagement, and win more time share, through three main areas: format innovation, functional innovation, and their intertwined ecosystem of applications.

- Longer-term, we view social platforms as well-positioned to capture the shift to the emerging and future generations of the consumer internet that likely includes immersive experiences. We expect this shift to compound the total addressable market that social platforms can capture.

Social Platforms Have a Track Record of Evolving

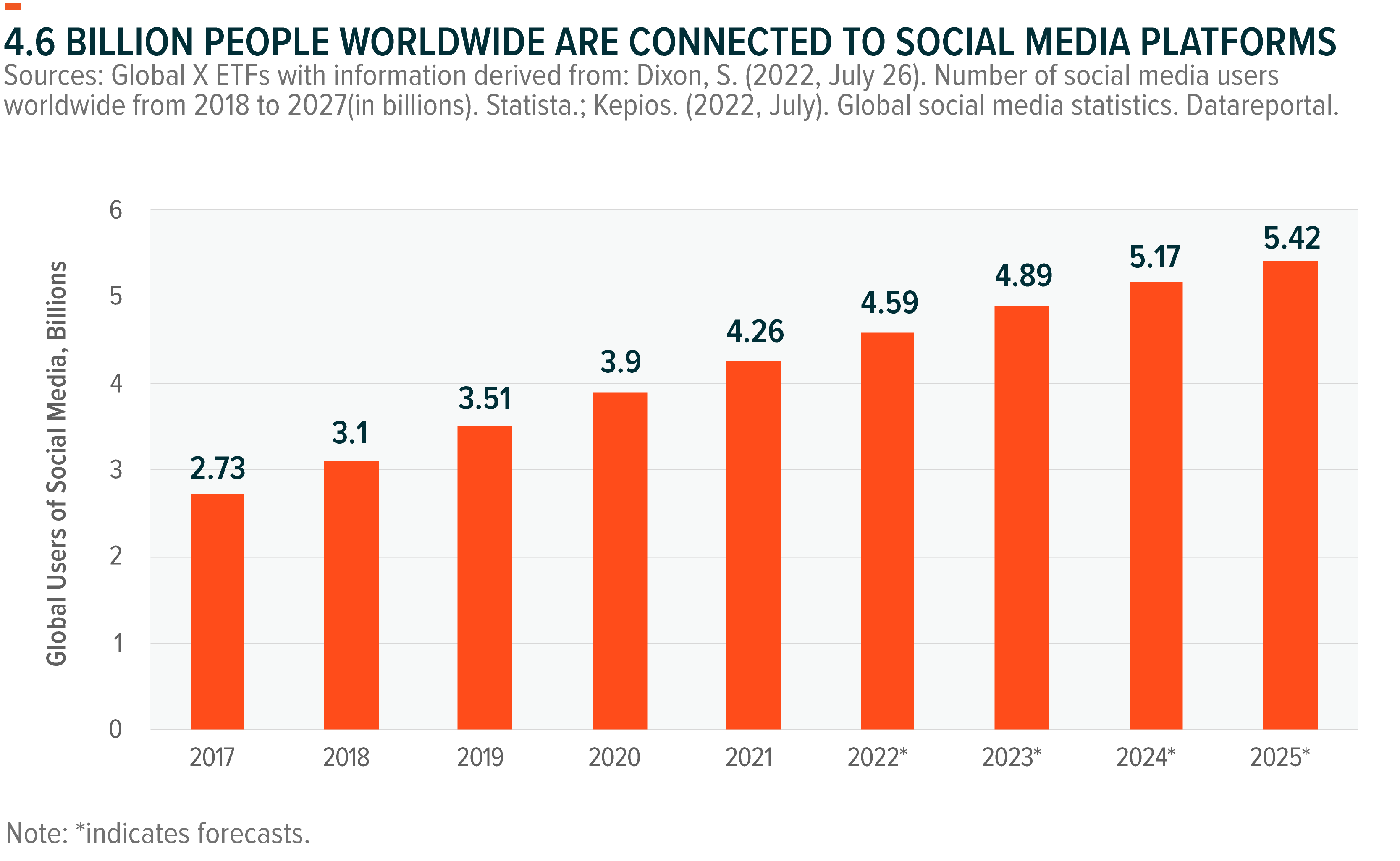

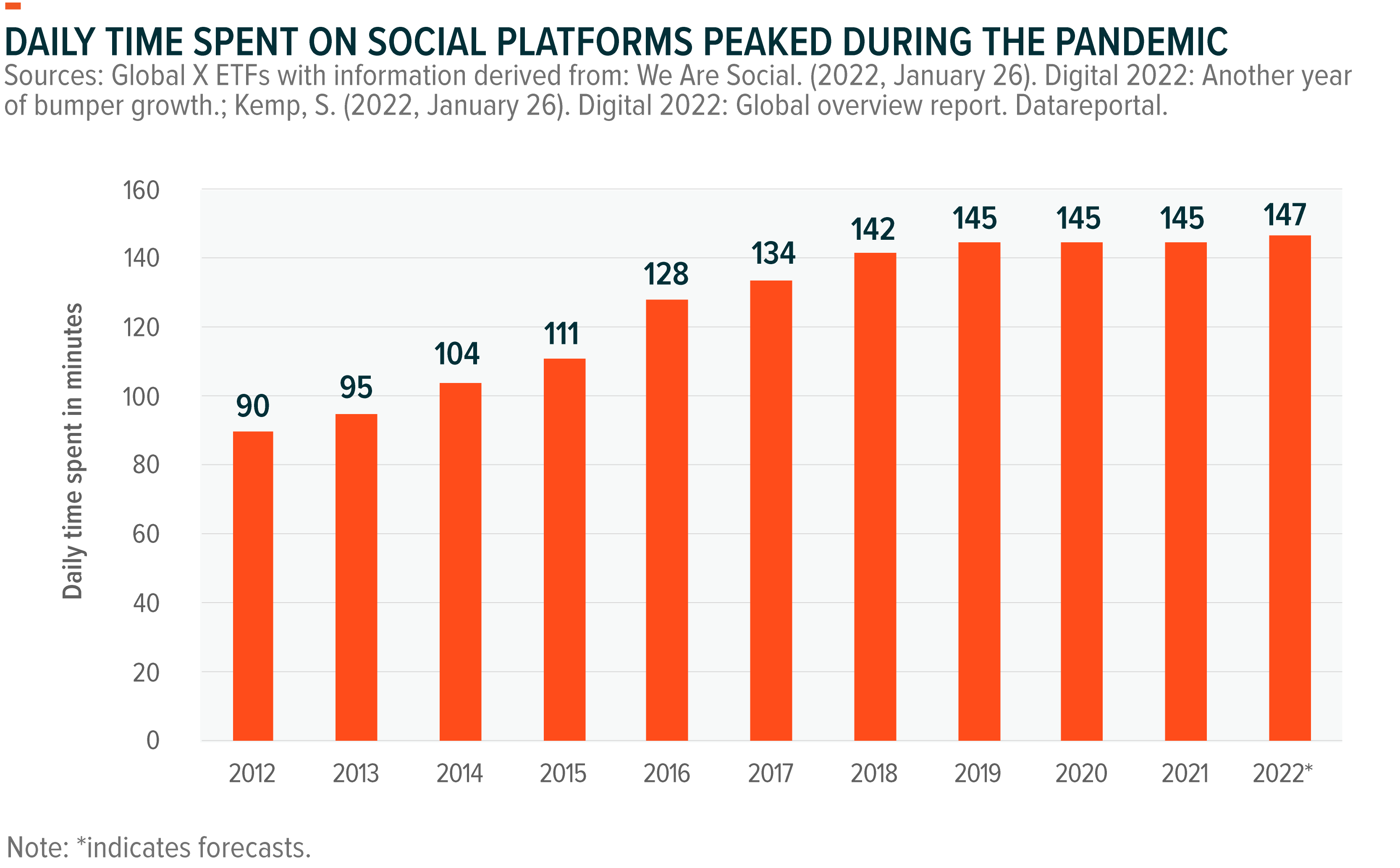

Social platforms are as old as the internet itself, with instant messaging, email, bulletin message boards, and online forums comprising the earliest versions. Platforms that focused on personal relationships took off in the 2000s, allowing users to migrate their offline relationships to the digital world. This migration ushered in a whole new paradigm of sharing information on the web. Friendster and Myspace paved the way, and then Facebook catapulted social networks into the middle of the Web 2.0 explosion. Today, approximately 4.6 billion people worldwide are connected to social media, and they spend 2.5 hours of their day on average on these platforms.1, 2

To manage the explosive growth phase of the last two decades, social platforms relied on digital advertising as the primary revenue source. Brands that were frustrated by the limitations of legacy ad channels like linear TV, where content is programmed for and consumed at set times, found the precise user targeting capabilities of the internet refreshing. That synergistic relationship helped digital advertising become a $520 billion market by 2021, with social media owning a 35% share.3

Ultimately, the COVID pandemic became a consequential catalyst to the social media growth story. Billions of people worldwide relied on social platforms to consume news, find verified information, keep tabs on what was happening in their communities, and discover bingeworthy content. Brands increased ad spending to chase the incremental user attention that was flooding these platforms, which brought windfall revenues and growth for the past 24 months.

As this COVID-induced growth cycle fades with leisure time returning to pre-2020 levels, investors are more skeptical about the prospects for the social internet platforms.4,5 Macro factors such as rising inflation, geopolitical tension, and foreign exchange headwinds certainly contribute to the current skepticism. However, we view these as transient near-term challenges that will likely have little material impact on these businesses and their opportunity sets over the long term.

A Rough 2022 Thus Far, But Challenges Could Be Priced In

We can identify four main concerns contributing to the market skepticism about the social media industry in 2022. First, the saturation of social media’s total addressable user base is a source of concern. Roughly 84% of the world’s population has access to a smartphone, or about 6.64 billion people.6 With 4.6 billion people on social platforms already, the limit on user growth is within sight.

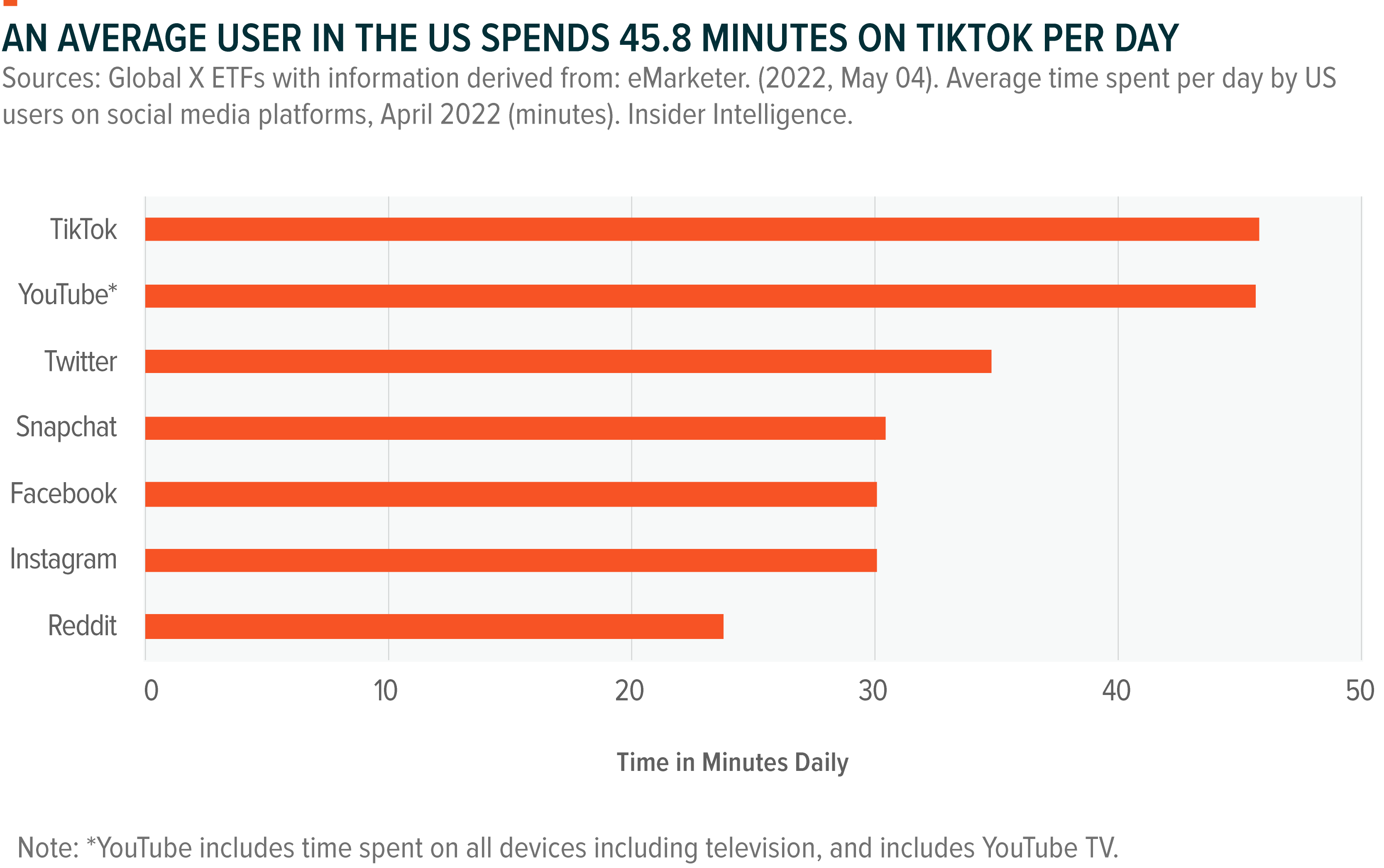

Second, social media is becoming increasingly competitive. TikTok and the rise of the short video format signals demand for bite-sized content, as opposed to text-based content designed for protracted consumption. On average, TikTok’s 110 million users in the U.S. are estimated to spend 45.8 minutes a day on the app in 2022 as per Insider Intelligence, which is up 83% since 2019.7 In this battle for user attention, platforms like Facebook, Instagram, and YouTube, as well as smaller platforms like Snapchat, Roblox, and Twitter may lose net share.

Third, the current macroeconomic conditions may affect social platforms’ financial flexibility and their ability to monetize user engagement. For example, consumer-focused brands are expected to cut back budgets due to inflation. Among them, big-box retailers, traditionally heavy spenders on online ads, may have to weigh the merits of ad spending as inventories pile up while consumers adjust their spending habits. After the COVID growth boost and with inflation and interest rates higher, demand appears to be resetting for e-commerce, streaming, digital health, and other online-heavy verticals.

Fourth, digital advertising is yet to fully recover from Apple tightening data sharing policies for iOS users. Apple’s introduction of App Tracking Transparency framework, which governs what user data developers can access, deprives digital ad platforms from extracting user data without consent. This change negatively affects the ad targeting abilities of almost all social platforms.8

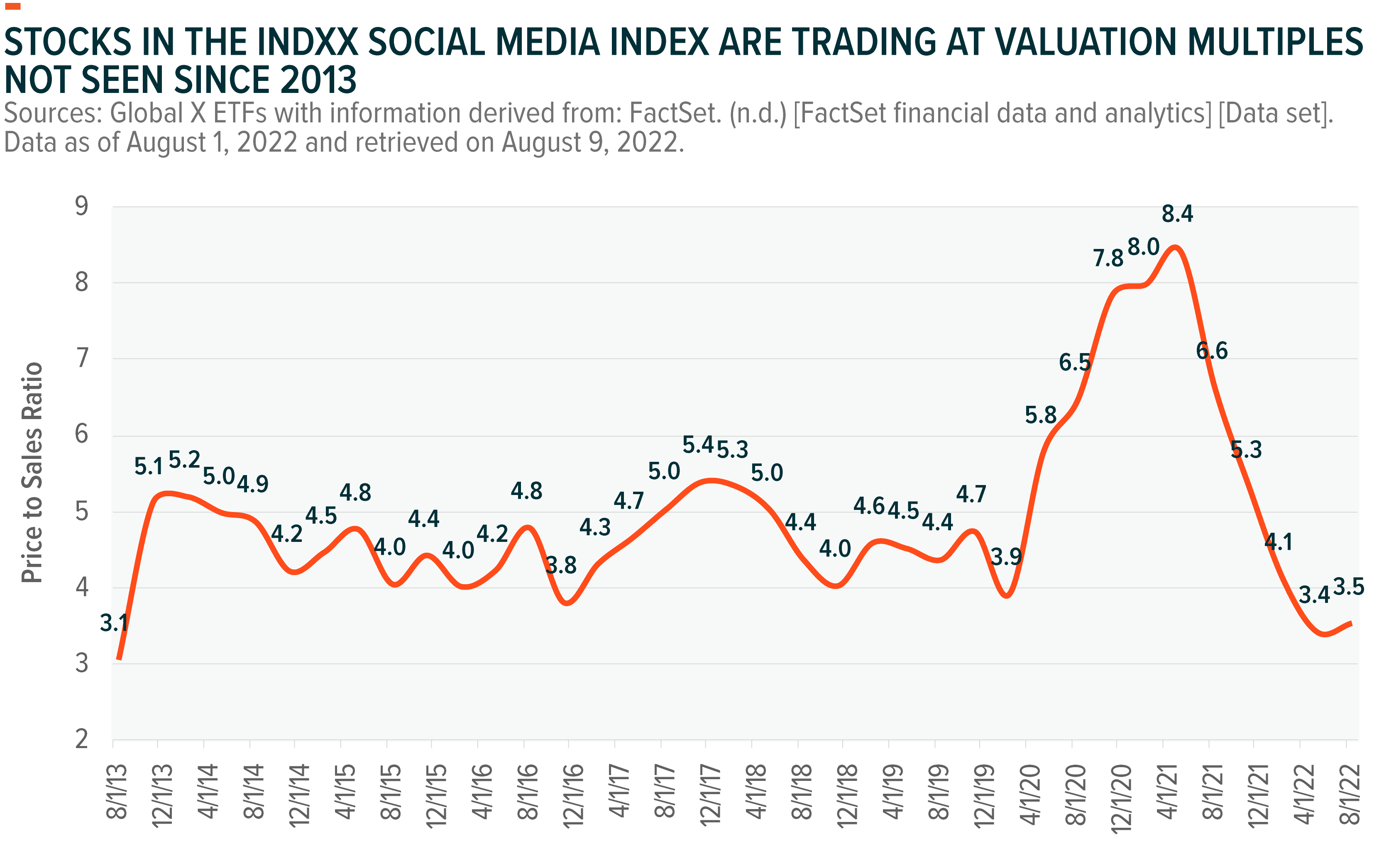

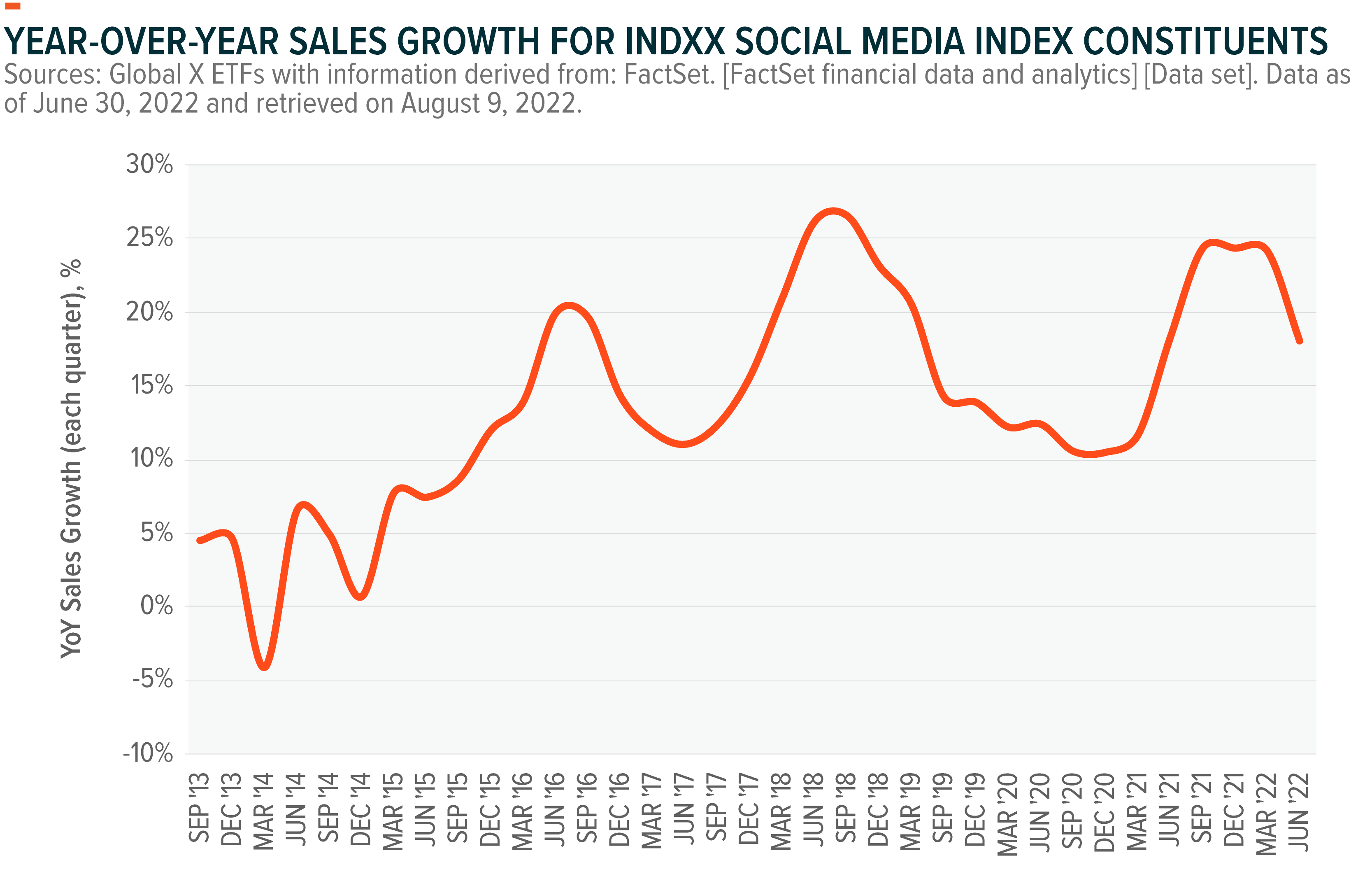

These concerns are valid. However, we believe that their impact is mostly played out on the stocks, and that any near-term weakness is likely already priced in after the market’s pullback year-to-date (YTD) until August 1, 2022. The Indxx Social Media Index is down 39.3% YTD, with valuations compressed to almost 10-year lows. The index traded at an average price-to-sales ratio of 3.5x, nearly 47% lower compared to August 1, 2021.

Another positive is that top-line growth has been relatively resilient. In the last 12 months, revenues for Indxx Social Media Index constituents are up 22.7% year-over-year (YoY), 10% higher than the year before. Growth for market leaders like Meta Platforms is softer, but in our view that decline is also a function of the compression in the broader digital ad market in 2022.

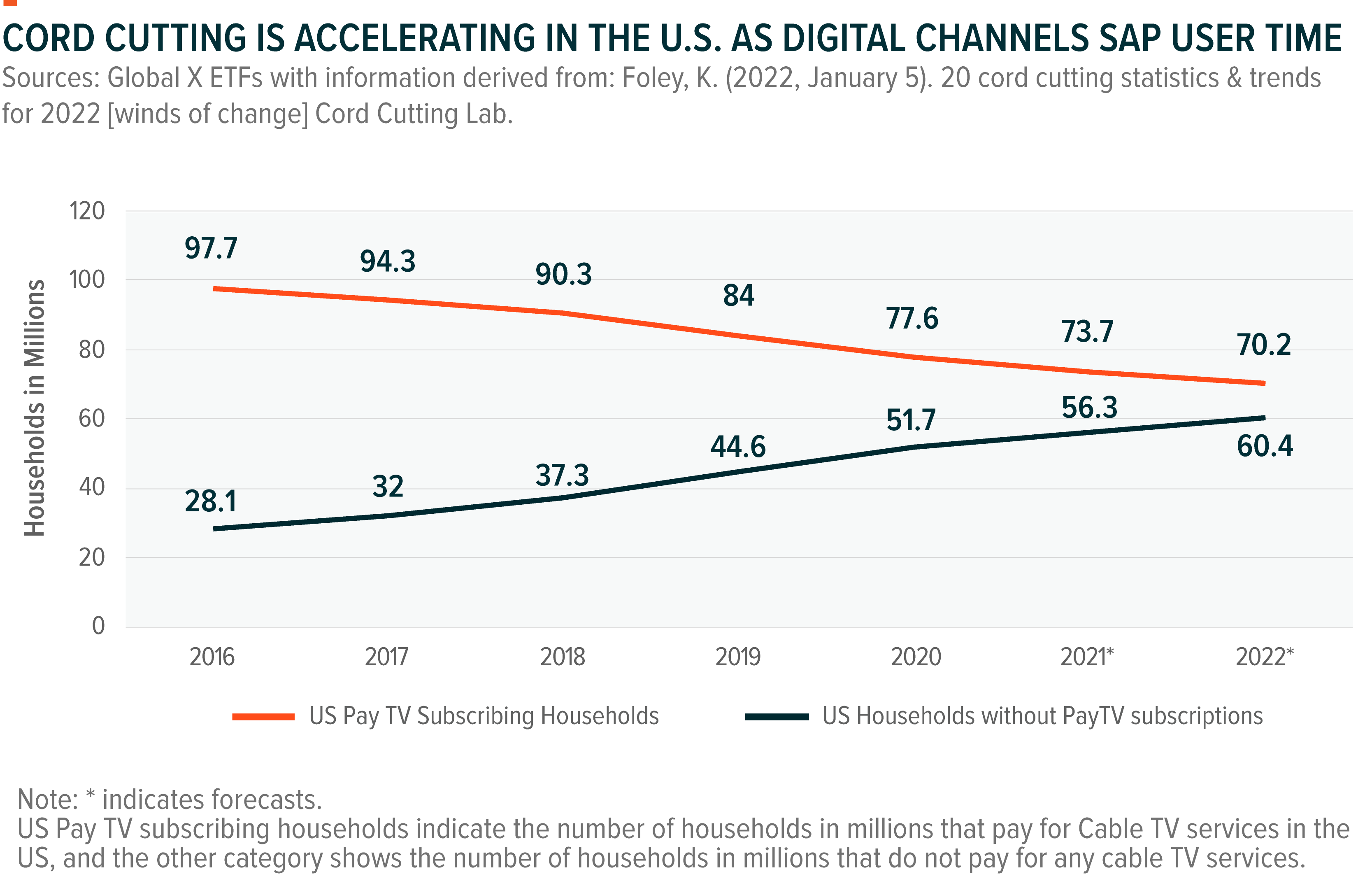

Social Media Is Winning the Time-Share War vs. Legacy Media

Social platforms gaining more user attention is a major contributor to the ongoing erosion of legacy media channels. In the U.S., the linear TV industry is going through a significant cord cutting wave. Similarly, longstanding forms of mass media, such as radio, newspapers, and magazines, are giving way to digital channels—and they still have significant room to give.9

Moreover, we expect social platforms can continue to boost user engagement, and take share from legacy media, through three main areas: format innovation, functional innovation, and their ecosystem of applications.

- Format innovation: Social internet platforms have relentlessly pursued product feature innovation. For example, web-based social quickly paved way for mobile social, and smartphone cameras paved the way for social experiences based on pictures. The latest fancy is short video. The audio social subcategory and podcasts on social media are taking off as well. With access to massive product and software engineering talent, we believe platforms will continue to use content shifts and product hooks to cement their time share gains on legacy and other non-social digital media channels, which rarely innovate as quickly.

- Functional innovation: As more services are bundled into these platforms, the utility value of social platforms increases, creating new value propositions. For example, social marketplaces are replacing online classified services. Social platforms now own a large share of online search for food, product, content, entertainment, and local services recommendations. These platforms are also emerging as the default communication and messaging channels for younger generations. Gen Z and younger prefer Snapchat for messaging over iMessage.10 In emerging markets, WhatsApp plays a central role in millions of users to access critical services.

- Ecosystem of applications: Leading internet franchises feature diverse portfolios of owned assets, which can help them capture user attention and diversify risk of meaningful user falloff. For example, Google has Search, YouTube, Maps, Android, Gmail, and a range of other consumer apps under its umbrella. Meta Platforms has a history of bold acquisitions, including Instagram and WhatsApp, and now counts 3.65 billion+ users across its family of apps11. Also, given these owned asset trends, we expect standalone applications to be less common, with social platforms likely to consolidate or be integrated with other services.

As user attention consolidates, we believe social platforms can translate these shifts to advertising dollars. The inherent benefits of digital advertising, including better user targeting and optimized spending, can continue to attract brands to the opportunity.

World of Opportunity Beyond Ads

Digital advertising comprises the bulk of social media revenues today, but we believe the industry has multiple avenues to kick-start growth in the short term, diversify their exposures, and keep investing for the long term.

- Creator services: Users increasingly favor content from individual creators and personalities, making access to leading creators potentially key for platforms to attract and retain audiences. Recognizing the trend, platforms want to capitalize on the opportunity by funding creator-led content and building tools and services to help creators better serve and monetize their base.12,13 Software tools designed to help creators understand their audience, improve content, receive payments, and discover brand partnership could eventually become major revenue streams for platforms.

- Social commerce: Social recommendations are now a significant factor in consumer purchase decisions.14 More than 30% of all product searches begin on social platforms today.15,16 Video commerce via live streaming on social channels, which is popular in China and Southeast Asia, is a new global trend. Platforms are integrating functionality to build native ecommerce stores in a bid to capitalize on the rise of digital solopreneurs and serve the increasing demand from small and medium-sized businesses (SMBs) for online sales. Also, secondary marketplaces inside social platforms are rising in popularity, addressing the $175 billion+ U.S. reselling industry.17

- Gaming and content services: According to one estimate, social gaming is expected to grow at a 16.1% compound annual growth rate (CAGR) from 2020–2027 to become a $57 billion market.18 Twitch, the category-leading platform, streams 1.5 billion hours of gameplay a month, serving an average of 2.5 million gamers a day.19 Meta Platforms and Alphabet-owned Google appear to have grand ambitions in gaming. Meta has been on a buying spree to solidify its gaming and virtual reality (VR) portfolio since 2019, buying Beat Games, Play Giga, Big Box VR, among others. Google launched cloud gaming service Stadia, acquired game developer Typhoon Studios, and secured key content deals.20

- Payments and Wallets: Historically, social platforms relied on legacy financial infrastructure for payment rails, with users directed to third-party platforms to enable transactions. But that practice is changing with large players like Meta and Google owning native digital wallets and keeping a fair bit of the commissions and fees for themselves. WeChat Pay, owned by Tencent and integrated with the WeChat communication system, is one of the most popular wallets in China.21 Social platforms are also experimenting with digital asset ownership, potentially creating opportunities to capture trading commissions and fees. A milestone could come from Instagram, which is expected to permit creators and collectors to showcase their Non-fungible Tokens (NFTs) starting in 2023.22

- Immersive experiences: The development cycle for completely immersive social experiences like the metaverse will likely be long, but we believe social platforms will play key role in enabling the next generation of consumer internet. The metaverse will draw from social platforms’ audiences, creators, and brands. To secure user buy-in, social platforms will be key in getting users to adopt avatars, purchase mixed-reality hardware, watch immersive content, and more. The platforms with well-established audiences are in the best position to win the eventual shift, an opportunity that could create trillions in economic value across consumer and enterprise use cases.23

Unexplored Optionality Compounds Social Media’s Total Addressable Market

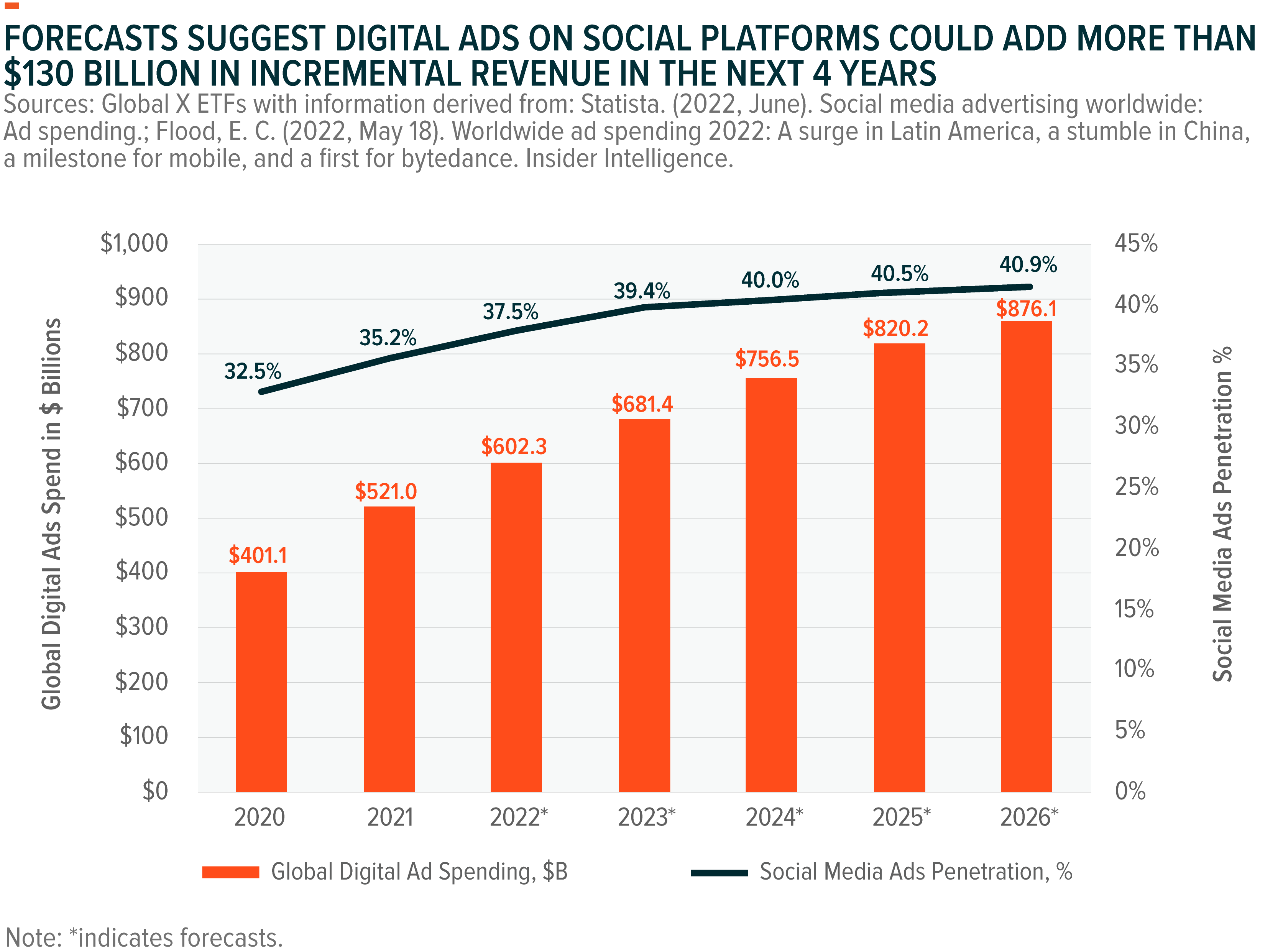

Digital advertising is expected to be a $600 billion market by year-end. Adding in promotional spending, advertising through offline channels, out-of-home marketing, radio, and other unmeasured categories, total global ad-spend for 2022 is estimated to be about $905 billion.24 In our view, digital advertising can address this entire pocket, and we expect a sizable portion of ad spending to move to social platforms.

Also, with a growing presence in emerging industries, social platforms have revenue opportunities beyond digital ads. Gaming is expected to be a $196.8 billion market in 2022.25 Global social commerce is an estimated $584 billion market at the end of 2021, with strong momentum in markets like China.26 The creator economy remains under-monetized at $100 billion.27,28,29 Estimates suggest that the metaverse could be a multi-trillion-dollar opportunity.30

Social Media Built for the Long-Term

Given these potential revenue sources, the long-term outlook for the social media industry looks bright, in our view. Social media platforms will likely remain prone to near-term macro challenges. And reinvestment that supports expansion into the above-mentioned emerging ventures could deflate profits in the next few quarters. However, we believe expansion in total engagement and impressions earned likely offsets the risks of these near-term headwinds. With valuations crawled back to three-year lows, the markets likely already priced these hurdles, potentially creating attractive opportunities for investors.

Related ETFs

HERO: The Global X Video Game & Esports ETF seeks to invest in companies that develop or publish video games, facilitate the streaming and distribution of video gaming or esports content, own and operate within competitive esports leagues, or produce hardware used in video games and esports, including augmented and virtual reality. Click the fund name above to view current holdings.

SOCL: The Global X Social Media ETF seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of the Solactive Social Media Total Return Index.

VR: The Global X Metaverse ETF seeks to invest in companies that are positioned to benefit from the development and commercialization of the Metaverse. This includes companies involved in the development of hardware and software that allow users to experience extended digital realities; creator platforms, where live streaming and other media content is shared in 3D simulations; creator economies, involving the development of applications involving digital payments, such as the creation and distribution of Non-Fungible Tokens (NFTs) and other digital asset payment gateways; as well as digital infrastructure/hardware, such as semiconductors, cloud computing technology and 5G infrastructure supporting digital media consumption.

Click the fund name for holdings information. Holdings are subject to change. Current and future holdings are subject to risk.

Image sourced from Shutterstock

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.