During the last three months, 13 analysts shared their evaluations of EQT EQT, revealing diverse outlooks from bullish to bearish.

The table below offers a condensed view of their recent ratings, showcasing the changing sentiments over the past 30 days and comparing them to the preceding months.

| Bullish | Somewhat Bullish | Indifferent | Somewhat Bearish | Bearish | |

|---|---|---|---|---|---|

| Total Ratings | 1 | 5 | 7 | 0 | 0 |

| Last 30D | 0 | 1 | 0 | 0 | 0 |

| 1M Ago | 0 | 0 | 4 | 0 | 0 |

| 2M Ago | 1 | 2 | 1 | 0 | 0 |

| 3M Ago | 0 | 2 | 2 | 0 | 0 |

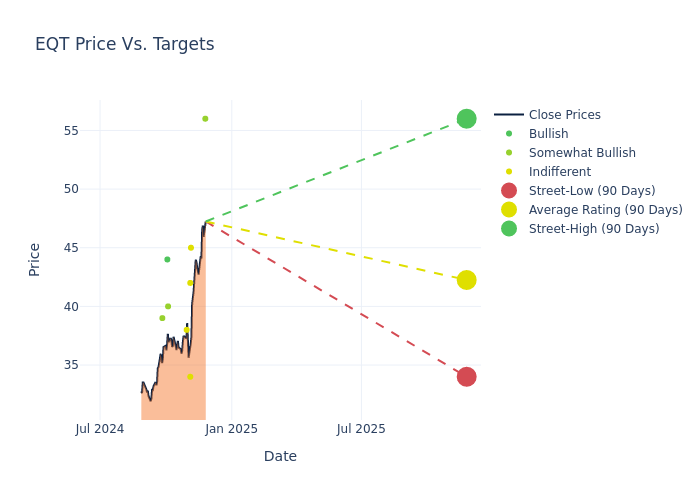

In the assessment of 12-month price targets, analysts unveil insights for EQT, presenting an average target of $41.54, a high estimate of $56.00, and a low estimate of $34.00. Witnessing a positive shift, the current average has risen by 3.64% from the previous average price target of $40.08.

Understanding Analyst Ratings: A Comprehensive Breakdown

In examining recent analyst actions, we gain insights into how financial experts perceive EQT. The following summary outlines key analysts, their recent evaluations, and adjustments to ratings and price targets.

| Analyst | Analyst Firm | Action Taken | Rating | Current Price Target | Prior Price Target |

|---|---|---|---|---|---|

| Devin McDermott | Morgan Stanley | Raises | Overweight | $56.00 | $45.00 |

| Nitin Kumar | Mizuho | Raises | Neutral | $45.00 | $41.00 |

| Mark Lear | Piper Sandler | Raises | Neutral | $34.00 | $32.00 |

| Josh Silverstein | UBS | Raises | Neutral | $42.00 | $40.00 |

| Mike Scialla | Stephens & Co. | Raises | Equal-Weight | $38.00 | $37.00 |

| Phillip Jungwirth | BMO Capital | Raises | Outperform | $40.00 | $39.00 |

| Nitin Kumar | Mizuho | Lowers | Neutral | $41.00 | $43.00 |

| Scott Gruber | Citigroup | Raises | Buy | $44.00 | $37.00 |

| Arun Jayaram | JP Morgan | Raises | Overweight | $39.00 | $37.00 |

| Josh Silverstein | UBS | Lowers | Neutral | $36.00 | $38.00 |

| Nitin Kumar | Mizuho | Lowers | Neutral | $43.00 | $45.00 |

| Devin McDermott | Morgan Stanley | Maintains | Overweight | $45.00 | $45.00 |

| Arun Jayaram | JP Morgan | Lowers | Overweight | $37.00 | $42.00 |

Key Insights:

- Action Taken: Analysts respond to changes in market conditions and company performance, frequently updating their recommendations. Whether they 'Maintain', 'Raise' or 'Lower' their stance, it reflects their reaction to recent developments related to EQT. This information offers a snapshot of how analysts perceive the current state of the company.

- Rating: Gaining insights, analysts provide qualitative assessments, ranging from 'Outperform' to 'Underperform'. These ratings reflect expectations for the relative performance of EQT compared to the broader market.

- Price Targets: Delving into movements, analysts provide estimates for the future value of EQT's stock. This analysis reveals shifts in analysts' expectations over time.

Assessing these analyst evaluations alongside crucial financial indicators can provide a comprehensive overview of EQT's market position. Stay informed and make well-judged decisions with the assistance of our Ratings Table.

Stay up to date on EQT analyst ratings.

Discovering EQT: A Closer Look

EQT Corp is an independent natural gas production company with operations focused in the Marcellus and Utica shale plays in the Appalachian Basin. At year-end 2023, EQT's proven reserves totaled 27.6 trillion cubic feet equivalent, with net production of 5.79 billion cubic feet equivalent per day. Natural gas accounted for 94% of production.

Financial Insights: EQT

Market Capitalization: Surpassing industry standards, the company's market capitalization asserts its dominance in terms of size, suggesting a robust market position.

Positive Revenue Trend: Examining EQT's financials over 3 months reveals a positive narrative. The company achieved a noteworthy revenue growth rate of 20.71% as of 30 September, 2024, showcasing a substantial increase in top-line earnings. As compared to competitors, the company surpassed expectations with a growth rate higher than the average among peers in the Energy sector.

Net Margin: The company's net margin is below industry benchmarks, signaling potential difficulties in achieving strong profitability. With a net margin of -24.72%, the company may need to address challenges in effective cost control.

Return on Equity (ROE): EQT's ROE is below industry averages, indicating potential challenges in efficiently utilizing equity capital. With an ROE of -1.7%, the company may face hurdles in achieving optimal financial returns.

Return on Assets (ROA): EQT's ROA lags behind industry averages, suggesting challenges in maximizing returns from its assets. With an ROA of -0.93%, the company may face hurdles in achieving optimal financial performance.

Debt Management: With a high debt-to-equity ratio of 0.68, EQT faces challenges in effectively managing its debt levels, indicating potential financial strain.

The Basics of Analyst Ratings

Experts in banking and financial systems, analysts specialize in reporting for specific stocks or defined sectors. Their comprehensive research involves attending company conference calls and meetings, analyzing financial statements, and engaging with insiders to generate what are known as analyst ratings for stocks. Typically, analysts assess and rate each stock once per quarter.

Analysts may enhance their evaluations by incorporating forecasts for metrics like growth estimates, earnings, and revenue, delivering additional guidance to investors. It is vital to acknowledge that, although experts in stocks and sectors, analysts are human and express their opinions when providing insights.

Breaking: Wall Street's Next Big Mover

Benzinga's #1 analyst just identified a stock poised for explosive growth. This under-the-radar company could surge 200%+ as major market shifts unfold. Click here for urgent details.

This article was generated by Benzinga's automated content engine and reviewed by an editor.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

date | ticker | name | Price Target | Upside/Downside | Recommendation | Firm |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.