Frontline FRO is gearing up to announce its quarterly earnings on Wednesday, 2024-11-27. Here's a quick overview of what investors should know before the release.

Analysts are estimating that Frontline will report an earnings per share (EPS) of $0.45.

Frontline bulls will hope to hear the company announce they've not only beaten that estimate, but also to provide positive guidance, or forecasted growth, for the next quarter.

New investors should note that it is sometimes not an earnings beat or miss that most affects the price of a stock, but the guidance (or forecast).

Historical Earnings Performance

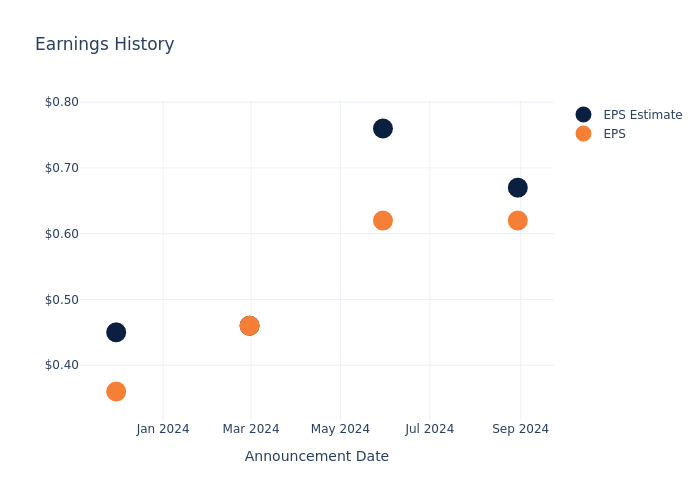

In the previous earnings release, the company missed EPS by $0.05, leading to a 0.0% drop in the share price the following trading session.

Here's a look at Frontline's past performance and the resulting price change:

| Quarter | Q2 2024 | Q1 2024 | Q4 2023 | Q3 2023 |

|---|---|---|---|---|

| EPS Estimate | 0.67 | 0.76 | 0.46 | 0.45 |

| EPS Actual | 0.62 | 0.62 | 0.46 | 0.36 |

| Price Change % | 4.0% | 1.0% | 0.0% | 1.0% |

Stock Performance

Shares of Frontline were trading at $19.03 as of November 25. Over the last 52-week period, shares are down 10.15%. Given that these returns are generally negative, long-term shareholders are likely unhappy going into this earnings release.

Insights Shared by Analysts on Frontline

Understanding market sentiments and expectations within the industry is crucial for investors. This analysis delves into the latest insights on Frontline.

Analysts have provided Frontline with 3 ratings, resulting in a consensus rating of Buy. The average one-year price target stands at $28.67, suggesting a potential 50.66% upside.

Comparing Ratings with Competitors

In this comparison, we explore the analyst ratings and average 1-year price targets of Plains GP Holdings, Scorpio Tankers and New Fortress Energy, three prominent industry players, offering insights into their relative performance expectations and market positioning.

- Plains GP Holdings received a Neutral consensus from analysts, with an average 1-year price target of $19.0, implying a potential 0.16% downside.

- As per analysts' assessments, Scorpio Tankers is favoring an Buy trajectory, with an average 1-year price target of $77.2, suggesting a potential 305.68% upside.

- For New Fortress Energy, analysts project an Buy trajectory, with an average 1-year price target of $15.0, indicating a potential 21.18% downside.

Analysis Summary for Peers

The peer analysis summary offers a detailed examination of key metrics for Plains GP Holdings, Scorpio Tankers and New Fortress Energy, providing valuable insights into their respective standings within the industry and their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| Frontline | Buy | 8.44% | $217.00M | 7.81% |

| Plains GP Holdings | Neutral | 5.57% | $929M | 2.24% |

| Scorpio Tankers | Buy | -7.97% | $131.75M | 5.50% |

| New Fortress Energy | Buy | 10.32% | $201.93M | 0.52% |

Key Takeaway:

Frontline ranks at the top for Revenue Growth and Gross Profit among its peers. It is in the middle for Consensus rating and Return on Equity.

All You Need to Know About Frontline

Frontline PLC is an international shipping company engaged in the seaborne transportation of crude oil and oil products. Group operates through the tankers segment. The tankers segment includes crude oil tankers and product tankers. Its geographical area of operation includes Arabian Gulf, West African, the North Sea, and the Caribbean. Frontline earns revenue through voyage charters, time charters, and a finance lease. It is also involved in the charter, purchase, and sale of vessels.

Key Indicators: Frontline's Financial Health

Market Capitalization Perspectives: The company's market capitalization falls below industry averages, signaling a relatively smaller size compared to peers. This positioning may be influenced by factors such as perceived growth potential or operational scale.

Revenue Growth: Frontline's revenue growth over a period of 3 months has been noteworthy. As of 30 June, 2024, the company achieved a revenue growth rate of approximately 8.44%. This indicates a substantial increase in the company's top-line earnings. When compared to others in the Energy sector, the company excelled with a growth rate higher than the average among peers.

Net Margin: Frontline's net margin surpasses industry standards, highlighting the company's exceptional financial performance. With an impressive 33.73% net margin, the company effectively manages costs and achieves strong profitability.

Return on Equity (ROE): The company's ROE is a standout performer, exceeding industry averages. With an impressive ROE of 7.81%, the company showcases effective utilization of equity capital.

Return on Assets (ROA): Frontline's ROA excels beyond industry benchmarks, reaching 2.87%. This signifies efficient management of assets and strong financial health.

Debt Management: The company maintains a balanced debt approach with a debt-to-equity ratio below industry norms, standing at 1.59.

To track all earnings releases for Frontline visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.