Tilly's TLYS will release its quarterly earnings report on Thursday, 2024-12-05. Here's a brief overview for investors ahead of the announcement.

Analysts anticipate Tilly's to report an earnings per share (EPS) of $-0.37.

Tilly's bulls will hope to hear the company announce they've not only beaten that estimate, but also to provide positive guidance, or forecasted growth, for the next quarter.

New investors should note that it is sometimes not an earnings beat or miss that most affects the price of a stock, but the guidance (or forecast).

Past Earnings Performance

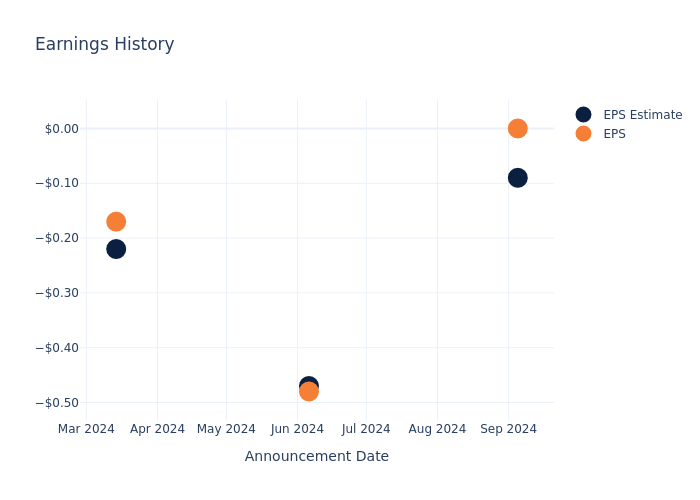

The company's EPS beat by $0.09 in the last quarter, leading to a 4.42% drop in the share price on the following day.

Here's a look at Tilly's's past performance and the resulting price change:

| Quarter | Q2 2024 | Q1 2024 | Q4 2023 | Q3 2023 |

|---|---|---|---|---|

| EPS Estimate | -0.09 | -0.47 | -0.22 | -0.07 |

| EPS Actual | 0 | -0.48 | -0.17 | -0.03 |

| Price Change % | -4.0% | -3.0% | -4.0% | -1.0% |

Tracking Tilly's's Stock Performance

Shares of Tilly's were trading at $4.44 as of December 03. Over the last 52-week period, shares are down 43.88%. Given that these returns are generally negative, long-term shareholders are likely bearish going into this earnings release.

Insights Shared by Analysts on Tilly's

Understanding market sentiments and expectations within the industry is crucial for investors. This analysis delves into the latest insights on Tilly's.

A total of 1 analyst ratings have been received for Tilly's, with the consensus rating being Neutral. The average one-year price target stands at $6.0, suggesting a potential 35.14% upside.

Comparing Ratings with Peers

The below comparison of the analyst ratings and average 1-year price targets of ThredUp, Citi Trends and Lulus Fashion Lounge, three prominent players in the industry, gives insights for their relative performance expectations and market positioning.

- The consensus outlook from analysts is an Outperform trajectory for ThredUp, with an average 1-year price target of $3.0, indicating a potential 32.43% downside.

- Citi Trends is maintaining an Neutral status according to analysts, with an average 1-year price target of $20.0, indicating a potential 350.45% upside.

- The consensus among analysts is an Neutral trajectory for Lulus Fashion Lounge, with an average 1-year price target of $2.0, indicating a potential 54.95% downside.

Summary of Peers Analysis

The peer analysis summary outlines pivotal metrics for ThredUp, Citi Trends and Lulus Fashion Lounge, demonstrating their respective standings within the industry and offering valuable insights into their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| Tilly's | Neutral | 1.82% | $49.92M | -0.05% |

| ThredUp | Outperform | -11.00% | $51.98M | -31.81% |

| Citi Trends | Neutral | 1.73% | $54.93M | -12.64% |

| Lulus Fashion Lounge | Neutral | -3.13% | $30.65M | -14.88% |

Key Takeaway:

Tilly's ranks at the bottom for Revenue Growth among its peers. It is also at the bottom for Gross Profit. For Return on Equity, Tilly's is at the bottom as well.

Get to Know Tilly's Better

Tilly's Inc works as a specialty retailer of casual apparel, footwear, and accessories for young men, young women, boys, and girls. It offers an unparalleled selection of relevant brands, styles, colors, sizes, and price points. It delivers branded fashion, and core styles for tops, outerwear, bottoms, and dresses. It also provides backpacks, hats, sunglasses, headphones, handbags, watches, and jewelry. It markets its products under the brand names of Vans, RVCA, Adidas, Nike SB, and Hurley among others. It operates its stores in malls, lifestyle centers, power centers, community centers, outlet centers, street-front locations, and also through e-commerce.

Tilly's: Financial Performance Dissected

Market Capitalization Perspectives: The company's market capitalization falls below industry averages, signaling a relatively smaller size compared to peers. This positioning may be influenced by factors such as perceived growth potential or operational scale.

Positive Revenue Trend: Examining Tilly's's financials over 3 months reveals a positive narrative. The company achieved a noteworthy revenue growth rate of 1.82% as of 31 July, 2024, showcasing a substantial increase in top-line earnings. As compared to its peers, the company achieved a growth rate higher than the average among peers in Consumer Discretionary sector.

Net Margin: Tilly's's net margin excels beyond industry benchmarks, reaching -0.04%. This signifies efficient cost management and strong financial health.

Return on Equity (ROE): Tilly's's ROE surpasses industry standards, highlighting the company's exceptional financial performance. With an impressive -0.05% ROE, the company effectively utilizes shareholder equity capital.

Return on Assets (ROA): Tilly's's financial strength is reflected in its exceptional ROA, which exceeds industry averages. With a remarkable ROA of -0.02%, the company showcases efficient use of assets and strong financial health.

Debt Management: Tilly's's debt-to-equity ratio is below the industry average at 1.69, reflecting a lower dependency on debt financing and a more conservative financial approach.

To track all earnings releases for Tilly's visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.