Conagra Brands CAG is set to give its latest quarterly earnings report on Thursday, 2025-04-03. Here's what investors need to know before the announcement.

Analysts estimate that Conagra Brands will report an earnings per share (EPS) of $0.73.

The market awaits Conagra Brands's announcement, with hopes high for news of surpassing estimates and providing upbeat guidance for the next quarter.

It's important for new investors to understand that guidance can be a significant driver of stock prices.

Historical Earnings Performance

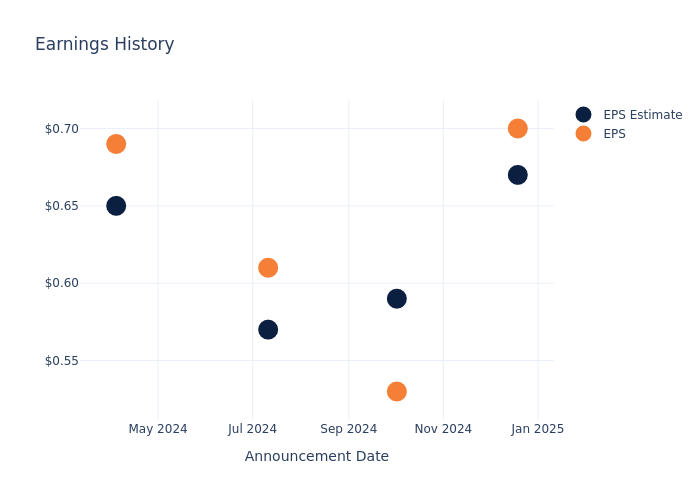

Last quarter the company beat EPS by $0.03, which was followed by a 1.12% increase in the share price the next day.

Here's a look at Conagra Brands's past performance and the resulting price change:

| Quarter | Q2 2025 | Q1 2025 | Q4 2024 | Q3 2024 |

|---|---|---|---|---|

| EPS Estimate | 0.67 | 0.59 | 0.57 | 0.65 |

| EPS Actual | 0.70 | 0.53 | 0.61 | 0.69 |

| Price Change % | 1.0% | -2.0% | -0.0% | 1.0% |

Tracking Conagra Brands's Stock Performance

Shares of Conagra Brands were trading at $26.6 as of April 01. Over the last 52-week period, shares are down 14.15%. Given that these returns are generally negative, long-term shareholders are likely unhappy going into this earnings release.

Analyst Opinions on Conagra Brands

For investors, staying informed about market sentiments and expectations in the industry is paramount. This analysis provides an exploration of the latest insights on Conagra Brands.

With 8 analyst ratings, Conagra Brands has a consensus rating of Neutral. The average one-year price target is $26.88, indicating a potential 1.05% upside.

Understanding Analyst Ratings Among Peers

The following analysis focuses on the analyst ratings and average 1-year price targets of JM Smucker, The Campbell's and Pilgrims Pride, three prominent industry players, providing insights into their relative performance expectations and market positioning.

- The prevailing sentiment among analysts is an Neutral trajectory for JM Smucker, with an average 1-year price target of $120.6, implying a potential 353.38% upside.

- The prevailing sentiment among analysts is an Neutral trajectory for The Campbell's, with an average 1-year price target of $40.1, implying a potential 50.75% upside.

- The prevailing sentiment among analysts is an Neutral trajectory for Pilgrims Pride, with an average 1-year price target of $48.0, implying a potential 80.45% upside.

Analysis Summary for Peers

The peer analysis summary provides a snapshot of key metrics for JM Smucker, The Campbell's and Pilgrims Pride, illuminating their respective standings within the industry. These metrics offer valuable insights into their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| Conagra Brands | Neutral | -0.41% | $846.70M | 3.25% |

| JM Smucker | Neutral | -1.94% | $878.10M | -9.11% |

| The Campbell's | Neutral | 9.32% | $819M | 4.46% |

| Pilgrims Pride | Neutral | -3.45% | $553.26M | 5.59% |

Key Takeaway:

Conagra Brands ranks in the middle among its peers for revenue growth. It ranks at the top for gross profit. It ranks in the middle for return on equity.

About Conagra Brands

Conagra Brands is a packaged food company that operates predominantly in the United States (over 90% of fiscal 2024 revenue). Most of its revenue comes from frozen food, including brands like Marie Callender's, Healthy Choice, Banquet, and Birds Eye. Conagra also sells snacks, shelf-stable staples, and refrigerated food through brands like Duncan Hines, Hunt's, Slim Jim, Vlasic, Orville Redenbacher's, Reddi-wip, Wish-Bone, and Chef Boyardee. The company primarily sells through the US retail channel, with just 9% of fiscal 2024 revenue coming from international markets and 10% from foodservice.

Unraveling the Financial Story of Conagra Brands

Market Capitalization: Indicating a reduced size compared to industry averages, the company's market capitalization poses unique challenges.

Revenue Growth: Conagra Brands's revenue growth over a period of 3 months has faced challenges. As of 30 November, 2024, the company experienced a revenue decline of approximately -0.41%. This indicates a decrease in the company's top-line earnings. As compared to competitors, the company encountered difficulties, with a growth rate lower than the average among peers in the Consumer Staples sector.

Net Margin: Conagra Brands's net margin surpasses industry standards, highlighting the company's exceptional financial performance. With an impressive 8.9% net margin, the company effectively manages costs and achieves strong profitability.

Return on Equity (ROE): The company's ROE is below industry benchmarks, signaling potential difficulties in efficiently using equity capital. With an ROE of 3.25%, the company may need to address challenges in generating satisfactory returns for shareholders.

Return on Assets (ROA): Conagra Brands's ROA is below industry averages, indicating potential challenges in efficiently utilizing assets. With an ROA of 1.35%, the company may face hurdles in achieving optimal financial returns.

Debt Management: Conagra Brands's debt-to-equity ratio is notably higher than the industry average. With a ratio of 0.96, the company relies more heavily on borrowed funds, indicating a higher level of financial risk.

To track all earnings releases for Conagra Brands visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.