In the ever-evolving and intensely competitive business landscape, conducting a thorough company analysis is of utmost importance for investors and industry followers. In this article, we will carry out an in-depth industry comparison, assessing Williams-Sonoma WSM alongside its primary competitors in the Specialty Retail industry. By meticulously examining key financial metrics, market positioning, and growth prospects, we aim to offer valuable insights to investors and shed light on company's performance within the industry.

Williams-Sonoma Background

With a retail and direct-to-consumer presence, Williams-Sonoma is a player in the $300 billion domestic home category and $450 billion international home market, focused on expanding its exposure in the B2B ($80 billion total addressable market), marketplace, and franchise areas. Namesake Williams-Sonoma (160 stores) offers high-end cooking essentials, while Pottery Barn (186) provides casual home accessories. West Elm (122) is an emerging concept for young professionals, and Rejuvenation (11) offers lighting and house parts. Brand extensions include Pottery Barn Kids and PBteen (46) as well as Mark & Graham and Greenrow. Williams-Sonoma also has a business-to-business team that supports projects that range from residential to large-scale commercial.

| Company | P/E | P/B | P/S | ROE | EBITDA (in billions) | Gross Profit (in billions) | Revenue Growth |

|---|---|---|---|---|---|---|---|

| Williams-Sonoma Inc | 22.28 | 12.16 | 3.24 | 11.98% | $0.38 | $0.84 | -2.86% |

| Arhaus Inc | 19.06 | 3.82 | 1.03 | 6.41% | $0.05 | $0.14 | 0.87% |

| Haverty Furniture Companies Inc | 18.34 | 1.15 | 0.50 | 2.66% | $0.01 | $0.11 | -12.52% |

| Average | 18.7 | 2.48 | 0.77 | 4.54% | $0.03 | $0.12 | -5.83% |

Through a thorough examination of Williams-Sonoma, we can discern the following trends:

-

The current Price to Earnings ratio of 22.28 is 1.19x higher than the industry average, indicating the stock is priced at a premium level according to the market sentiment.

-

The elevated Price to Book ratio of 12.16 relative to the industry average by 4.9x suggests company might be overvalued based on its book value.

-

The Price to Sales ratio of 3.24, which is 4.21x the industry average, suggests the stock could potentially be overvalued in relation to its sales performance compared to its peers.

-

The company has a higher Return on Equity (ROE) of 11.98%, which is 7.44% above the industry average. This suggests efficient use of equity to generate profits and demonstrates profitability and growth potential.

-

Compared to its industry, the company has higher Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) of $380 Million, which is 12.67x above the industry average, indicating stronger profitability and robust cash flow generation.

-

Compared to its industry, the company has higher gross profit of $840 Million, which indicates 7.0x above the industry average, indicating stronger profitability and higher earnings from its core operations.

-

The company's revenue growth of -2.86% is notably higher compared to the industry average of -5.83%, showcasing exceptional sales performance and strong demand for its products or services.

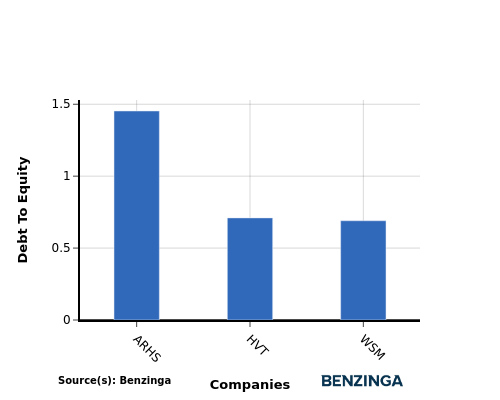

Debt To Equity Ratio

The debt-to-equity (D/E) ratio gauges the extent to which a company has financed its operations through debt relative to equity.

Considering the debt-to-equity ratio in industry comparisons allows for a concise evaluation of a company's financial health and risk profile, aiding in informed decision-making.

When examining Williams-Sonoma in comparison to its top 4 peers with respect to the Debt-to-Equity ratio, the following information becomes apparent:

-

When compared to its top 4 peers, Williams-Sonoma has a moderate debt-to-equity ratio of 0.69.

-

This implies that the company maintains a balanced financial structure with a reasonable level of debt and an appropriate reliance on equity financing.

Key Takeaways

The high P/E, P/B, and P/S ratios of Williams-Sonoma suggest that the company is trading at a premium compared to its peers in the Specialty Retail industry. On the other hand, the high ROE, EBITDA margin, gross profit margin, and revenue growth indicate that Williams-Sonoma is generating strong returns and growth relative to its industry counterparts.

This article was generated by Benzinga's automated content engine and reviewed by an editor.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.