By Conor Sen

A wise man once said, "All you have is your name and your word." Indeed. That, in a nutshell, is LinkedIn's economic proposition. Professor Pinch and I have written a lot about the emerging data economy and how it represents the next phase of disruptive change for the Internet.

One of the key components of the data economy, I wrote, is that one of its functions will be quantifying the value of people and social groups, a "Moneyball for everyone" (see Social Media Trends: We'll All Soon Be Naked in the Data Economy). And it's LinkedIn, not Facebook, that is best positioned to capture the economic value of this movement.

(To read Alex Moore's article on Facebook and Google Solidarity, click here.)

I spent a couple hours last night watching interviews with Reid Hoffman, founder of LinkedIn. There's a Charlie Rose interview with him here, and Kevin Depew included his South by Southwest 2011 speech in Wednesday's Five Things You Need to Know: Doomsday Is the Next Speculative Bubble.TechCrunch has a glowing piece up saying that Hoffman is the entrepreneur to admire of the social web, not Mark Zuckerberg. His background is compelling, and began atypically for a Silicon Valley entrepreneur.

Graduating from Stanford with a BA in "symbolic systems," he then earned a MA in philosophy from Oxford University, not exactly a normal stepping stone to becoming an Internet visionary. He noted that he chose a career in entrepreneurship over academia because, "When I graduated from Stanford my plan was to become a professor and public intellectual. That is not about quoting Kant. It's about holding up a lens to society and asking 'who are we?' and 'who should we be, as individuals and a society?' But I realized academics write books that 50 or 60 people read and I wanted more impact." From there he went on to become one of the early PayPal guys, and then a successful angel investor, with stakes in Facebook, Zynga, and Flickr, among others. He notes that when he considers angel investments he focuses on marketplaces, networks, and platforms.

(To check out Kevin Depew's piece on Doomsday becoming the next speculative bubble, click here.)

So anyway, I like the data economy as an investment theme, I like LinkedIn's place in it (nobody other than Google (GOOG) or Facebook is better positioned), and I like LinkedIn's team, starting with Hoffman. What about the stock?

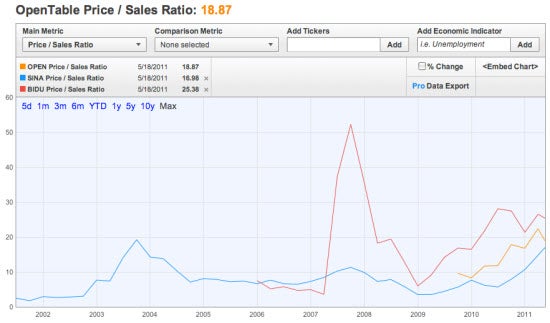

In 2010 it took in $243 million in revenues. In the first quarter of 2011 it took in $94 million, up 110% from $44.7 million a year ago. That makes trailing 12-month revenues $292 million. What sort of multiple does that deserve? For comparison, recent high-flyer Internet stocks like OpenTable (OPEN) SINA Corp (SINA), and Baidu (BIDU) trade at 18.9x, 17.0x, and 25.4x, respectively. Facebook 2010 revenues were roughly $2 billion, and with some estimating a current value of $70 billion, that'd put Facebook around 35x sales. LinkedIn going public at $4.5 billion, or 15.4x trailing 12-month revenues, seems entirely reasonable by comparison.

I expect this strong growth for LinkedIn to continue for years. Hoffman believes there's room for more than one online profile, with room for at least a social profile (Facebook) and a professional profile (LinkedIn). I agree, and actually believe LinkedIn's barriers to entry are higher than Facebook's. When it comes down to it, how valuable is that marginal high school friend posting Mafia Wars updates vs a marginal professional contact on LinkedIn who could one day lead to another job or professional opportunity?

(To read Raghu Gullappalli's analysis on the LinkedIn IPO and the potential of the Internet Bubble 2.0, click here.)

Hoffman envisions a world where LinkedIn, for example, would monitor analytics about trending skills and types of companies in a particular city, allowing users to see what skills are in demand and find resources to attain those skills to become more valuable in the marketplace. LinkedIn should eventually crush the business models of Monster.com (MWW), CareerBuilder, Robert Half (RHI), and Craigslist, among others.

Let's say LinkedIn grows revenues at 95% in 2011, 75% in 2012, 60% in 2013, 45% in 2014, and 35% in 2015. That would put 2015 revenues at $2.6 billion. Doesn't seem crazy. As the chart below shows, as recently as the end of 2005, Google, eBay (EBAY), and Yahoo (YHOO) all traded at price/sales ratios north of 10. These companies were all fairly mature growers at that point, as LinkedIn should be in 2015. Skype just sold for 10x revenues. And 10 times 2015 revenues of $2.6 billion would give LinkedIn a market cap of $26 billion. If I'm Microsoft (MSFT), Google, or Facebook I buy LinkedIn for $10 billion this morning, assuming they'd sell, and consider myself lucky.

I expect this strong growth for LinkedIn to continue for years. Hoffman believes there's room for more than one online profile, with room for at least a social profile (Facebook) and a professional profile (LinkedIn). I agree, and actually believe LinkedIn's barriers to entry are higher than Facebook's. When it comes down to it, how valuable is that marginal high school friend posting Mafia Wars updates vs a marginal professional contact on LinkedIn who could one day lead to another job or professional opportunity?

(To read Raghu Gullappalli's analysis on the LinkedIn IPO and the potential of the Internet Bubble 2.0, click here.)

Hoffman envisions a world where LinkedIn, for example, would monitor analytics about trending skills and types of companies in a particular city, allowing users to see what skills are in demand and find resources to attain those skills to become more valuable in the marketplace. LinkedIn should eventually crush the business models of Monster.com (MWW), CareerBuilder, Robert Half (RHI), and Craigslist, among others.

Let's say LinkedIn grows revenues at 95% in 2011, 75% in 2012, 60% in 2013, 45% in 2014, and 35% in 2015. That would put 2015 revenues at $2.6 billion. Doesn't seem crazy. As the chart below shows, as recently as the end of 2005, Google, eBay (EBAY), and Yahoo (YHOO) all traded at price/sales ratios north of 10. These companies were all fairly mature growers at that point, as LinkedIn should be in 2015. Skype just sold for 10x revenues. And 10 times 2015 revenues of $2.6 billion would give LinkedIn a market cap of $26 billion. If I'm Microsoft (MSFT), Google, or Facebook I buy LinkedIn for $10 billion this morning, assuming they'd sell, and consider myself lucky.

Clearly, LinkedIn could botch execution, competition for professional social networks could emerge, and hey, none of this really matters since the world is ending on Saturday and all. But investors snickering at LinkedIn's valuation should be careful about writing it off. LinkedIn looks like the most exciting US IPO since Google's in 2004, and there is no company going public in the near future, and that includes Facebook, Zynga, Groupon, and Twitter, that I am most interested in buying for the long-term.

(To read the rest, head on over to Minyanville.)

Clearly, LinkedIn could botch execution, competition for professional social networks could emerge, and hey, none of this really matters since the world is ending on Saturday and all. But investors snickering at LinkedIn's valuation should be careful about writing it off. LinkedIn looks like the most exciting US IPO since Google's in 2004, and there is no company going public in the near future, and that includes Facebook, Zynga, Groupon, and Twitter, that I am most interested in buying for the long-term.

(To read the rest, head on over to Minyanville.)

I expect this strong growth for LinkedIn to continue for years. Hoffman believes there's room for more than one online profile, with room for at least a social profile (Facebook) and a professional profile (LinkedIn). I agree, and actually believe LinkedIn's barriers to entry are higher than Facebook's. When it comes down to it, how valuable is that marginal high school friend posting Mafia Wars updates vs a marginal professional contact on LinkedIn who could one day lead to another job or professional opportunity?

(To read Raghu Gullappalli's analysis on the LinkedIn IPO and the potential of the Internet Bubble 2.0, click here.)

Hoffman envisions a world where LinkedIn, for example, would monitor analytics about trending skills and types of companies in a particular city, allowing users to see what skills are in demand and find resources to attain those skills to become more valuable in the marketplace. LinkedIn should eventually crush the business models of Monster.com (MWW), CareerBuilder, Robert Half (RHI), and Craigslist, among others.

Let's say LinkedIn grows revenues at 95% in 2011, 75% in 2012, 60% in 2013, 45% in 2014, and 35% in 2015. That would put 2015 revenues at $2.6 billion. Doesn't seem crazy. As the chart below shows, as recently as the end of 2005, Google, eBay (EBAY), and Yahoo (YHOO) all traded at price/sales ratios north of 10. These companies were all fairly mature growers at that point, as LinkedIn should be in 2015. Skype just sold for 10x revenues. And 10 times 2015 revenues of $2.6 billion would give LinkedIn a market cap of $26 billion. If I'm Microsoft (MSFT), Google, or Facebook I buy LinkedIn for $10 billion this morning, assuming they'd sell, and consider myself lucky.

Clearly, LinkedIn could botch execution, competition for professional social networks could emerge, and hey, none of this really matters since the world is ending on Saturday and all. But investors snickering at LinkedIn's valuation should be careful about writing it off. LinkedIn looks like the most exciting US IPO since Google's in 2004, and there is no company going public in the near future, and that includes Facebook, Zynga, Groupon, and Twitter, that I am most interested in buying for the long-term.

(To read the rest, head on over to Minyanville.)Market News and Data brought to you by Benzinga APIs

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Posted In:

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in