This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

AT-A-GLANCE

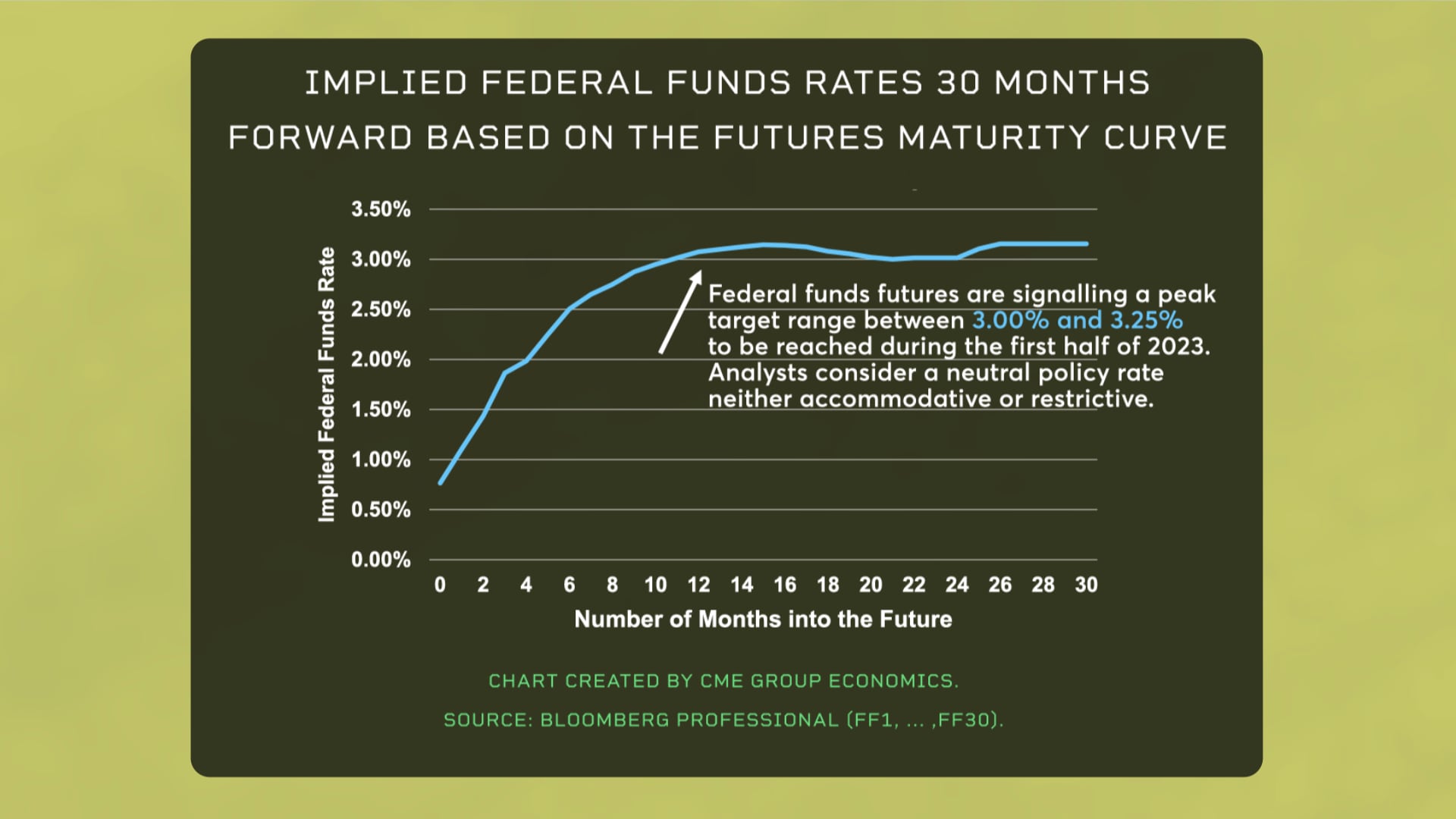

- Recessions do not tend to happen when the Fed is in “neutral”

- Profit margin compression is a challenge for equity valuations, but it does not necessarily signal a recession

- Equity markets hit a downdraft in April and early May, in part, because market participants sensed the risk of a recession was rising. Let’s unpack five key factors that are influencing recession probabilities.

1. The Federal Reserve and higher interest rates

According to the federal funds futures market, market participants expect the Fed to raise short-term rates to about 3% by early 2023 and then take a pause. Most analysts would consider a 3% short-term interest rate as in the neutral territory, neither accommodative nor restrictive. Recessions do not tend to happen when the Fed is in “neutral”. Recessions are much more likely only when the Fed moves rates well into restrictive territory.

Scan the above QR code for more expert analysis of market events and trends driving opportunities today!

2. There was massive fiscal stimulus during the pandemic, financed by the Fed buying bonds

The fiscal stimulus is not being repeated and the Fed has just commenced to shrink its balance sheet, which means it will no longer purchase large quantities of U.S. Treasury and Mortgage-Backed securities each month. With less demand, bond prices have fallen and yields have risen.

Just as Fed bond purchases supported equities, reducing the Fed’s balance sheet is a headwind for equities because the higher U.S. Treasury yields raise the bar for equities in the portfolio allocation process. But taking the Fed out of the bond price discovery process does not signal a recession. It allows bond and equity markets to more fully consider inflation risks to valuations, and it potentially cools off a hot housing market.

3. Rising input and wage costs

Many corporations are likely to face profit margin compression due to higher input costs and rising wages trying to catch up with inflation. Profit margin compression is a challenge for equity valuations, but it does not necessarily signal a recession.

4. High oil prices

The Ukraine conflict has sent oil prices, and then gasoline prices, soaring. This factor contributes to rising recession risk and rising input costs, but so far the U.S. economy is coping with the energy price shocks.

5. China is decelerating sharply

The Covid-zero policy’s implications for a weaker Chinese economy are not good for certain commodities as China growth slows. However, a weaker China is more likely to be reflected in Chinese yuan depreciation than in contributing to a U.S. recession.

The bottom line is that U.S. growth is certainly slowing back to trend growth after the rapid rebound to the pandemic shock, but that does not necessarily mean a recession is around the corner. Equity markets had many additional headwinds besides recession risk that contributed to a re-assessment of valuations in April and early May.

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.