Wall Street’s early February optimism evaporated under inflation’s stifling heat, raising questions about the staying power of 2023’s early rally.

It wouldn’t be surprising if markets consolidate further in March as participants struggle with the possibility that interest rates are a long way from pausing, let alone easing. With inflation still stubborn, a disappointing Q4 earnings season mostly in the books, and fresh Federal Reserve input straight ahead, it might be challenging for stocks to mount a March test of last summer’s peaks.

March means most states turn their clocks ahead (don’t forget) and that there’s a lighter company reporting calendar. The lower flow of earnings traffic could open a lane for increased focus on the Fed and geopolitics, especially China’s reopening and continued tensions between the United States, China, and other nations.

Fed in spotlight

Still, the Fed probably remains front and center as spring approaches. Most prominent is the March 21 – 22 Federal Open Market Committee (FOMC) meeting, which includes updated central bank economic and rate projections. Many analysts believe the Fed will raise its projection for terminal, or peak, rates from the 5% to 5.25% range in December’s dot-plot.

Investors don’t need to wait long in March for the Fed’s impact, however. Fed Chairman Jerome Powell is scheduled to offer his semiannual testimony to the U.S. Senate’s Banking Committee on Tuesday, March 7.

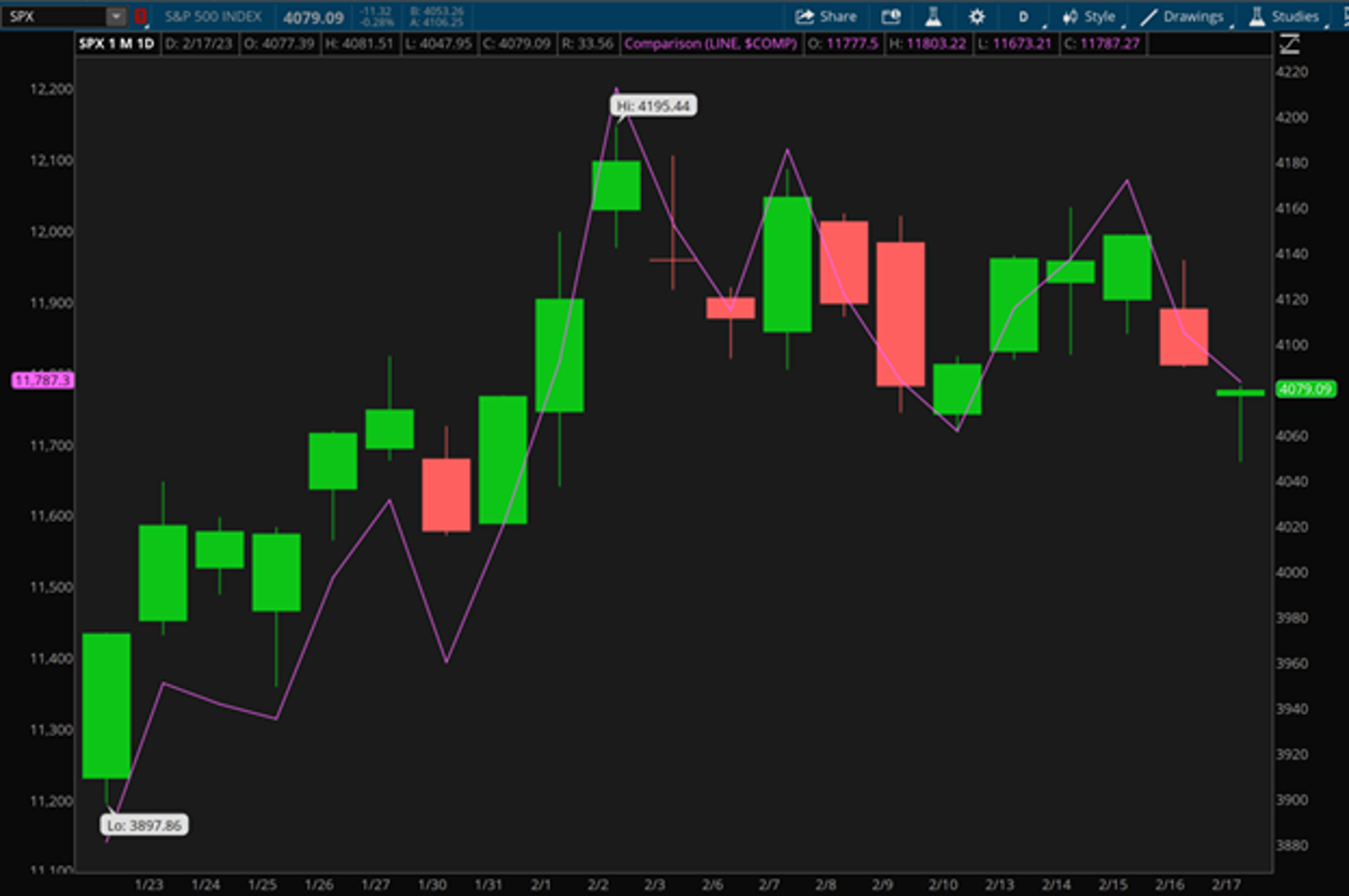

Questions from Congress to Powell often cover a wide range of topics, but this year, inflation is likely top of mind. Despite recent powerful jobs and Retail Sales data that helped raise major indexes to five-month highs during parts of February, the economy seems unable to put troublesome 2022 inflation behind it. Two alarming reads on inflation in mid-February changed Wall Street’s mood. The January Consumer Price Index (CPI) and Producer Price Index (PPI) were a stomach-churning one-two punch.

January headline CPI climbed 0.5% and core CPI, stripping out food and energy, rose 0.3%. Headline PPI rose a dizzying 0.7% in January, with core PPI up 0.5%. All these data points were above December’s levels and above analysts’ average estimates. Together, the two reports shifted investor thinking in a big way. When you look at them in the company of January’s tremendous jobs growth of more than 500,000 and a Retail Sales pop of 3%, ideas of a cooling economy melt like March snow.

Not long ago, common wisdom suggested the Fed had made progress fighting inflation. November and December CPI and PPI looked a lot better than readings earlier in 2022, and many economic indicators suggested a resilient consumer despite higher prices. That theory is now in question. How long can consumers hold out if prices keep rising? And if companies decide to eat their rising input costs, how long before their already narrowing profit margins compress further?

After the unpleasant January inflation reports, Fed speakers sounded more resolute about fighting rising costs. Notably, Cleveland Fed President Loretta Mester said in mid-February that she might’ve voted in favor of a half-point rate hike at the last FOMC meeting when rates rose a quarter-point. St. Louis Fed President James Bullard, though not a voting member of the FOMC this year, suggested he might support a half-point hike in March.

There’s a lot of symbolism in these remarks. Until recently, most analysts had penciled in one or two more quarter-point hikes by midyear, but most believed the 75- and 50-basis-point hikes of 2022 were in the past. Easing inflation, the theory went, would mean less pressure on the Fed. It could simply stair-step rather than use the elevator. The Treasury market penciled in a mid-2023 pause followed by a late-2023 cut in rates.

Now the Fed could come under more pressure to consider a half-point hike at its March meeting after more color from February’s Nonfarm Payrolls, Retail Sales, CPI, and PPI. All hit the tape in coming weeks.

February’s Payrolls report might attract more scrutiny than usual after the Labor Department reported jobs growth of 517,000 positions in January versus pre-report estimates of 190,000. If the February data—due March 10—doesn’t fall sharply from January’s swollen level, that would provide more evidence of a robust labor market despite recent rate hikes, possibly raising inflation fears further.

One month isn’t a trend, and the January inflation and jobs data should be seen as a snapshot. But the government also recently revised November and December’s price growth data upward, suggesting earlier numbers weren’t a blip. Market participants might feel like Dorothy waking up in Kansas, wondering if January and its hopes of turning a corner on prices were all a dream.

Also, don’t lose sight of China. Its reopening has major implications for economic growth here and in Europe. One date to watch is March 14, when China releases early 2023 data on industrial production and retail sales, according to Trading Economics. Those numbers might provide a hint of whether China’s successfully returning to normal—or struggling.

Check the register

Big-box retailers usually report their year-end results in mid-to-late February, but interestingly, some of these numbers are arriving later this year. Early March puts retail in Wall Street’s store windows. While some behemoths like Walmart (WMT) and Home Depot (HD) already reported and Target (TGT) is due the last day of February, the first week of March brings expected results from Lowe’s (LOW), Best Buy (BBY), Nordstrom (JWN), and Macy’s (M).

How will retailers see the picture as they report Q4 results? Did consumers close their wallets overall, or did they simply divert that spending toward travel, dining out, and other “experiences” that were so limited during the worst days of the pandemic?

Remember—what happens in households often portends what’s next for the global economy. After all, consumer spending comprises roughly 70% of Gross Domestic Product (GDP). While Retail Sales did perk up in January, it’s important to note that many of the big stores soon reporting earnings will be covering a period that includes December, when many consumers froze their spending in the retail economy that had been so robust since the pandemic.

Looking back at Q4 earnings results, it was likely the first earnings season in more than two years with year-over-year profit declines for S&P 500® companies. Though the final bell won’t ring until retailers are through reporting in early March, analysts believe S&P 500 earnings probably fell 4% to 5%, and some are starting to take a red pen to their Q1 and Q2 estimates as well. Research firm CFRA recently lowered its Q1 and Q2 S&P earnings per share (EPS) forecast to –5.1% and –5%, respectively. The firm sees EPS up just 0.1% for the full year of 2023.

Barely budging Q1 and 2023 EPS growth isn’t likely what investors want to contemplate as they plan their spring breaks and watch college hoops. Unfortunately, that’s exactly what narrowing margins, stubborn inflation, and a stalwart Fed often portend.

Image sourced from Shutterstock

TD Ameritrade® commentary for educational purposes only. Member SIPC.

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.