Stocks climbed last week with the S&P 500 rising 0.7% to close at 4,536.34. The index is now up 18.1% year to date, up 26.8% from its October 12 closing low of 3,577.03, and down 5.4% from its January 3, 2022 record closing high of 4,796.56.

In the stock market, do valuation metrics like price-to-earnings (P/E) multiples matter?

Of course they do!

However, they don’t appear to be very helpful when predicting short term moves in prices.

In a blog published on Tuesday, Nick Maggiulli of Ritholtz Wealth Management addressed “The Problem with Valuation.” Here’s a brief excerpt:

I think Nick’s right. And I think we sometimes take for granted how much the frictions and costs have come down for those seeking to trade or invest in stocks.

Average valuations have been higher in recent decades. (Source: Nick Maggiullli)

Jack pointed out that trading fees have been coming down for decades, which certainly justify higher valuation premiums — if it costs less to trade, then the returns you require should probably be lower.

Perhaps the most disturbing observation about P/E ratios comes from Goldman Sachs. In a research note published a little over a year ago, Goldman analysts concluded (emphasis added):

So just because you can calculate an average does not mean what you’re observing has a tendency to gravitate toward that average over time.

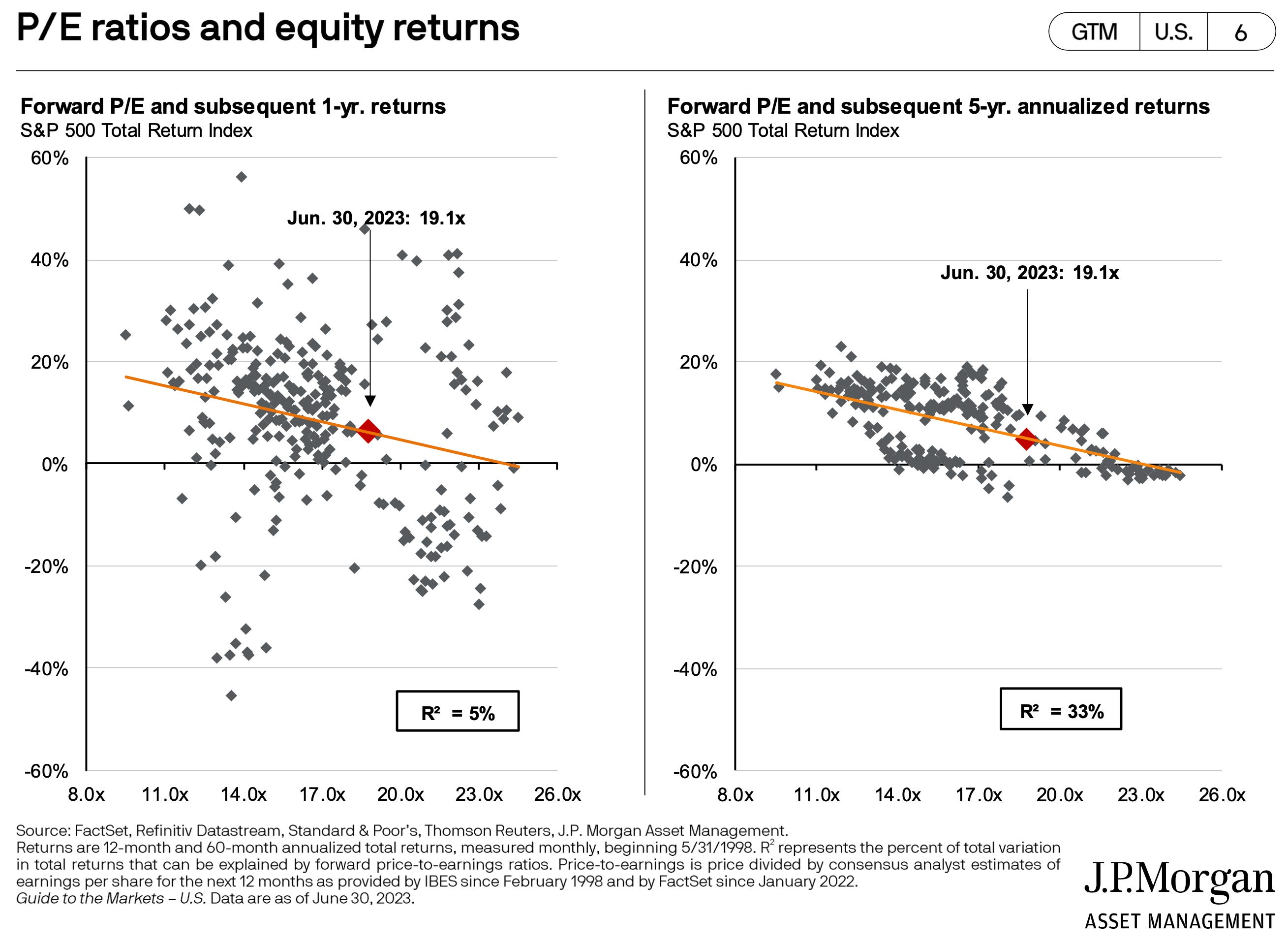

Maybe you’re not willing to accept what we’ve discussed here so far. Then, at least consider this: While there is some historical evidence that valuations may tell you something about long-term returns, that data also shows valuations tell you almost nothing about where stocks will go in the following 12 months.

P/E ratios don’t tell you much about the next year’s returns. (Source: JPMorgan Asset Management)

If this sounds familiar, it’s because it’s TKer Stock Market Truth No. 6: Valuations won’t tell you much about the next year.

To be fair, the chart on the right suggests there may be a relationship between valuations and longer term returns. Specifically, high valuations may mean lower average returns over rolling five year periods. But as Nick notes: “while future returns do seem lower, when we will experience them is anyone’s guess.“

The bottom line is that you should use valuation metrics like the P/E ratio with caution. Just because valuations are high at a given moment does not mean the next 12 months’ return will be weak.

A version of this post was originally published on Tker.co

© 2026 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

To add Benzinga News as your preferred source on Google, click here.