I spent the past week at Future Proof Festival, the premier conference for the wealth management industry. I participated on a panel, recorded a podcast, caught up with some old friends, and made many new ones!

My favorite part was seeing many existing subscribers and getting to know new subscribers who let me know what was and wasn’t working for them with TKer and the other newsletters out there. It was extremely helpful, and I expect to incorporate some tweaks in the coming weeks and months.

One thing most subscribers seem to value are the charts and stats I curate from all the research that hits my inbox.

So without further ado, here are some charts and stats!

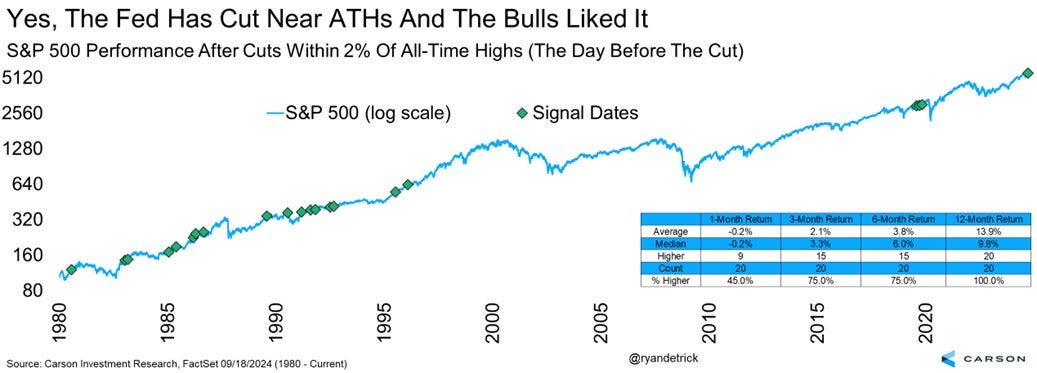

When The Fed Cuts Rates While Stocks Are At Record Highs

People often assume the Federal Reserve will cut interest rates only when the economy is in trouble. That’s sort of true, but there’s a lot of nuance.

One observation that many folks have been making is that the Fed’s recent rate cut is coinciding with a stock market near record highs. How can that make sense?

It actually happens to be the case that it’s not unusual for the Fed to cut rates with stocks near record highs. From Carson Group’s Ryan Detrick: “Here are the 20 times the Fed cut rates when the S&P 500 was within 2% of an [all-time high] (based on the day before the cut). Higher a yr later all 20 times and up 13.9% on avg. [Wednesday] was the 21st time.“

(Source: @RyanDetrick)

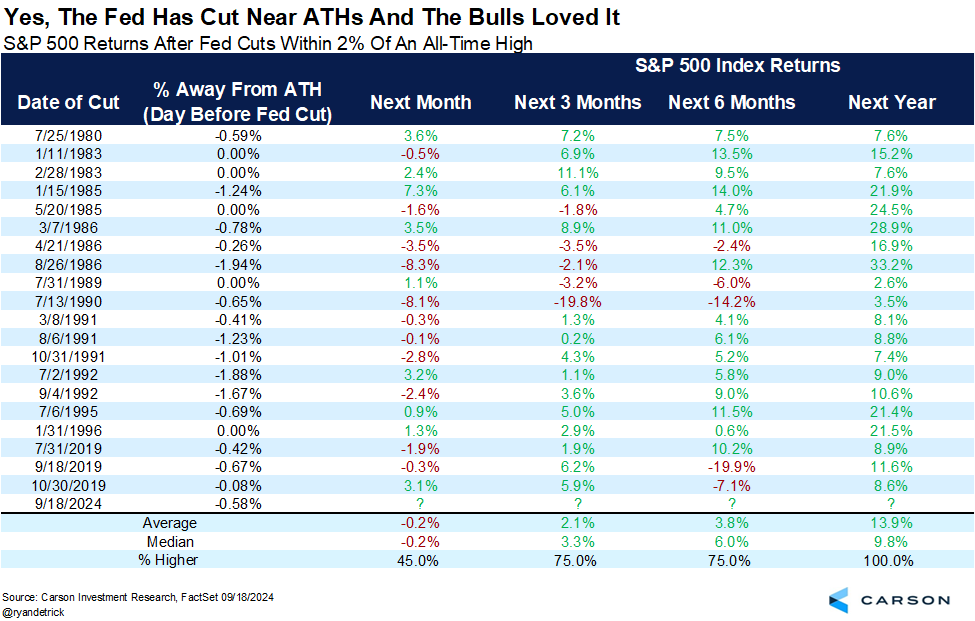

Here’s a more detailed look at those historical instances.

(Source: @RyanDetrick)

There’s a lot to be said about monetary policy. For our purposes, one thing we can say is that a rate cut when stocks are at record highs historically hasn’t been a bad sign for long-term investors.

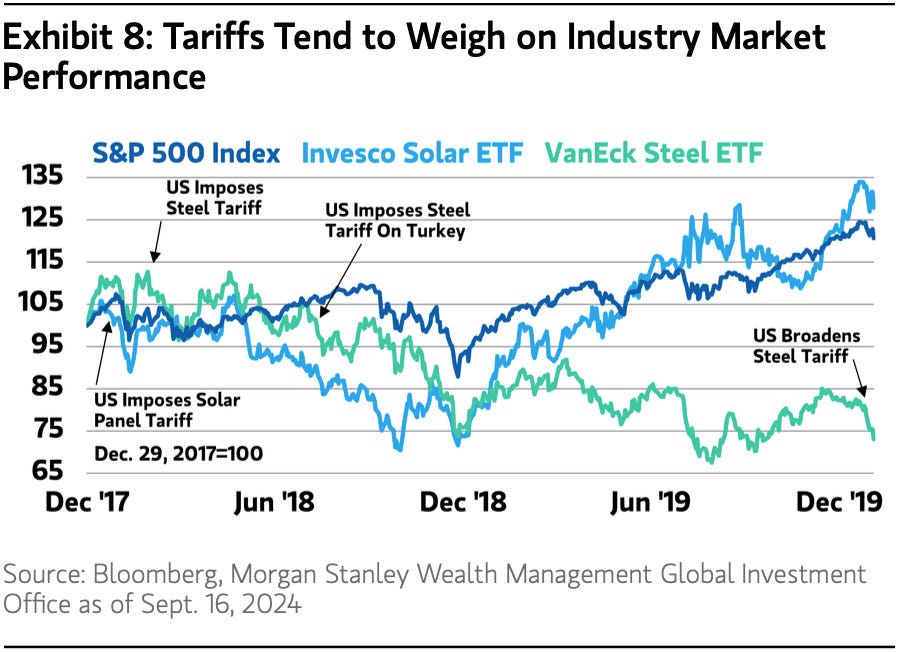

Tariffs Are Bad For Exposed Industries

That outlook for policy is a hot topic these days as the presidential nominees make their pitches ahead of the U.S. presidential election.

One controversial proposal involves tariffs on goods imported into the U.S.

Generally speaking, tariffs are considered bad news for the industries exposed. From Morgan Stanley Wealth Management: “In January 2018, Trump imposed tariffs on solar panels and washing machines of 30% to 50%. In March 2018, he imposed tariffs of 25% on steel and 10% on aluminum from most countries, which, according to Morgan Stanley & Co. Research, covered an estimated 4.1% percent of US imports. Following these measures, industries impacted by the tariffs underperformed. For example, both the Invesco Solar ETF and the VanEck Steel ETF declined by more than 11% in the first six months following enactment (see Exhibit 8). Tariff related pressures and trade uncertainty at the time caused both solar and steel to underperform the S&P 500 until mid-2019.“

(Source: Morgan Stanley Wealth)

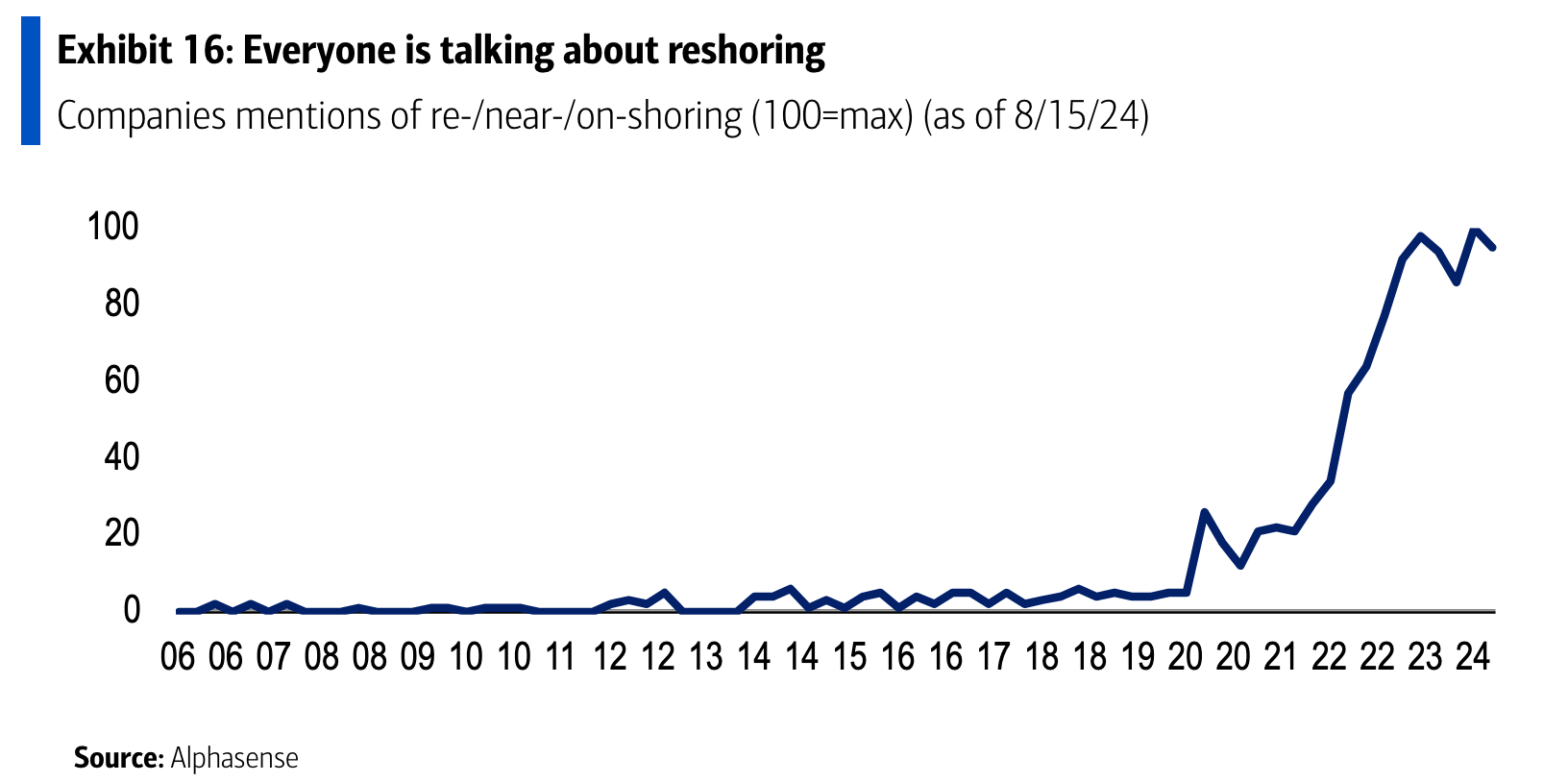

Reshoring Remains A Hot Topic

The COVID-19 pandemic exposed a lot of vulnerabilities in the global supply chain. Many big companies have responded by moving links of their supply chain to the U.S. or closer to the U.S.

And they continue to talk about these plans. BofA’s Savita Subramanian addressed it in a note to clients on Thursday: “Reshoring and near-shoring commentary is evident across a broad array of corporates. Reshoring mentions on earnings calls continue to climb…“

(Source: BofA)

This is could be bullish for capex spending, which is bullish for economic activity.

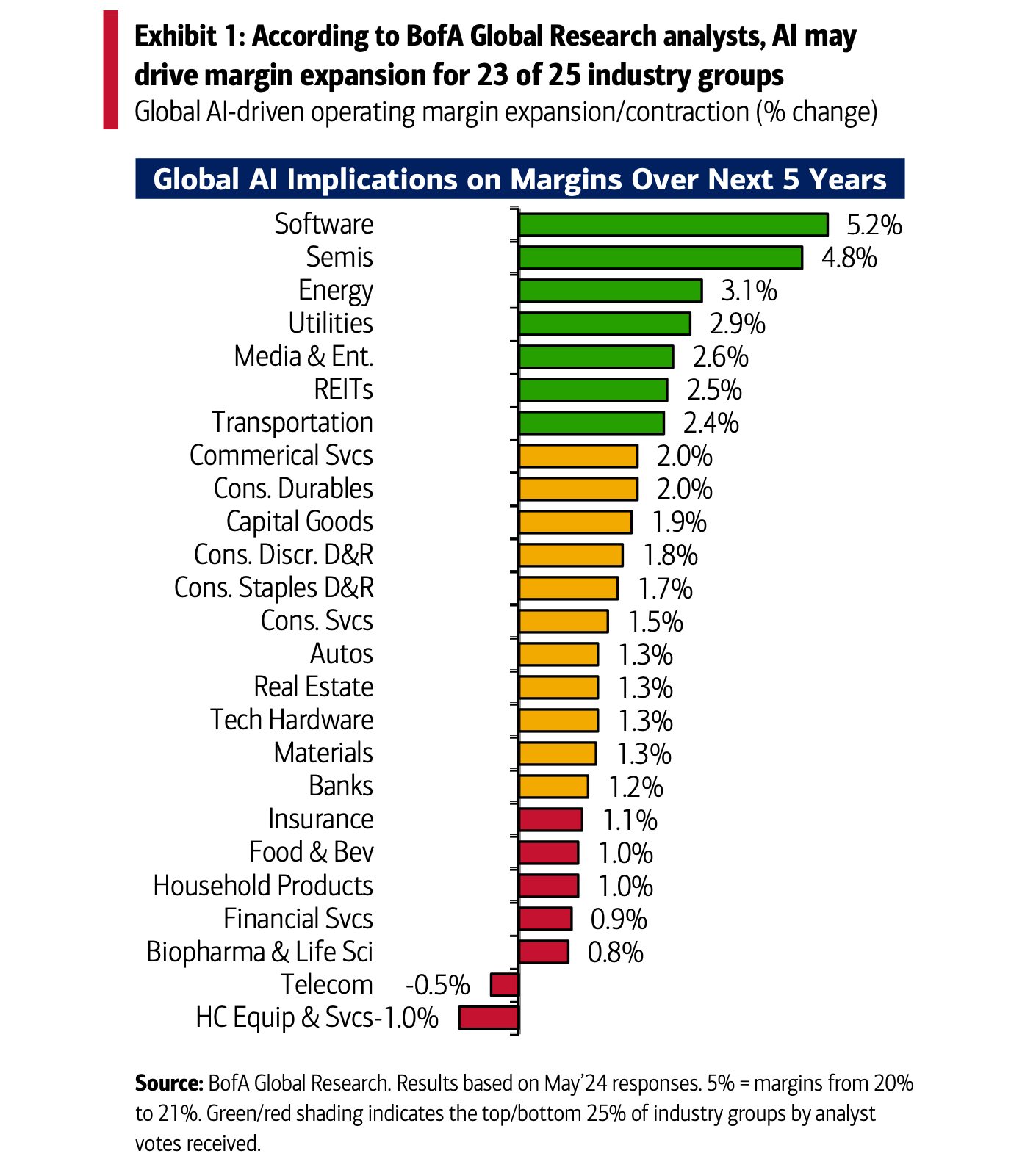

AI Is A Tailwind For Profit Margins

Stubbornly high profit margins continue to surprise many. Are they sustainable?

In the near-term, the answer seems to be yes. Analysts expect companies to benefit from operating leverage as modest revenue growth leads to strong earnings growth.

Longer term, companies are expected to benefit from improved efficiencies thanks to the deployment of AI-technologies.

BofA recently surveyed its analysts about the impact of AI: “BofA Global Research analysts found that enterprise AI implementations are moving from pilots to production, which could boost S&P operating margins by 200 basis points (bps) over the next five years, equivalent to approximately $55 billion in cost savings, annually. Surveyed analysts expect AI to drive margin expansion for 23 of the 25 industry groups globally, with implementations potentially boosting both semis and software margins by around five percent. They also note that companies within semis and software may also see AI-driven revenue increase by 34% and 25%, respectively, over the next five years.“

(Source: BofA)

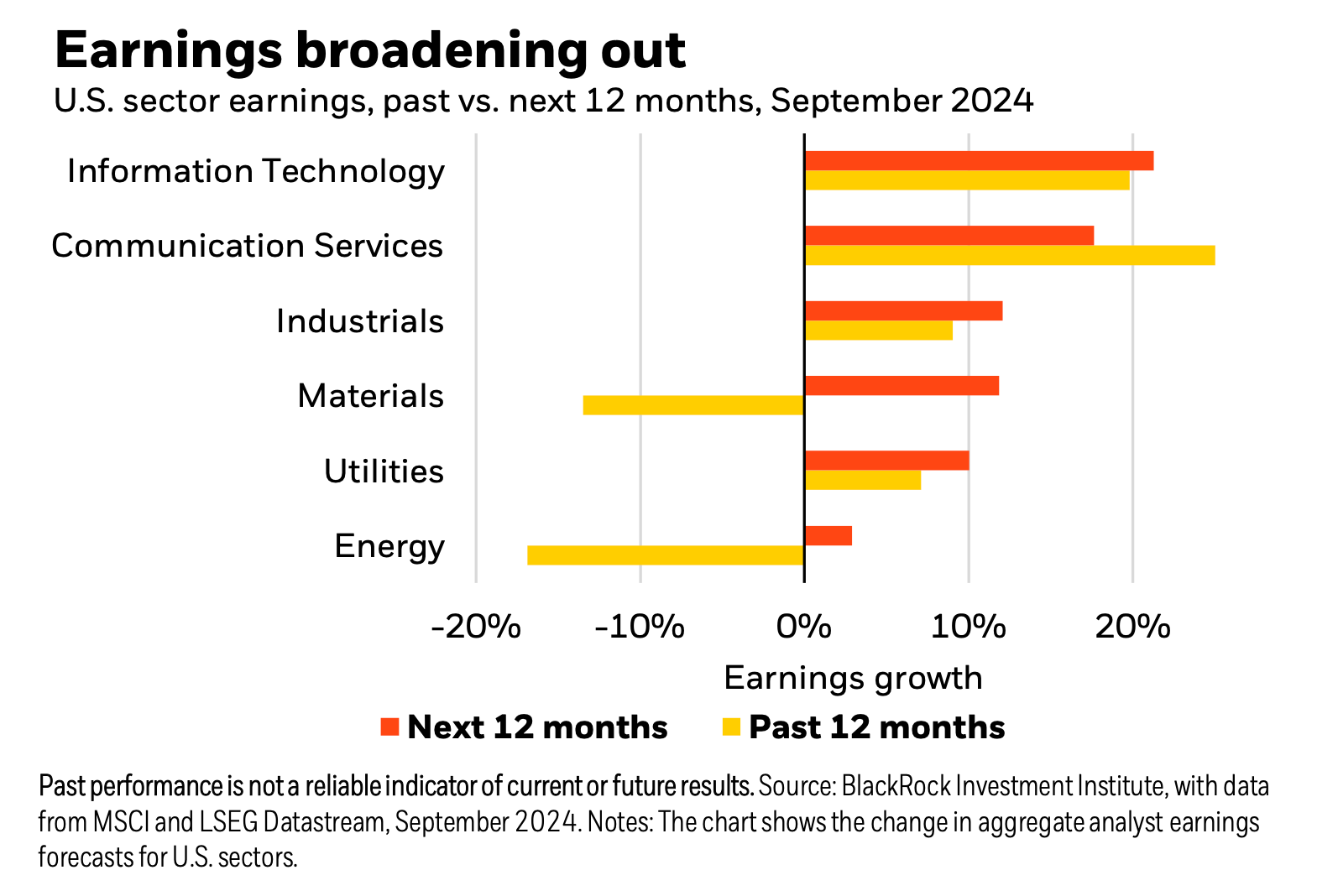

Earnings Growth Is Broadening Out

For a little while, earnings growth had been largely driven by the big tech and communication services companies, particularly the so-called “Magnificent Seven.”

Those concerned about market concentration can find solace in the fact that more companies across industries are expected to contribute to the stock market’s earnings prospects. From BlackRock’s Sept. 9 note to clients: “We see a narrowing gap in earnings growth between U.S. tech companies and the rest of the market – even if tech still leads the way – suggesting U.S. equity returns can broaden.“

(Source: BlackRock)

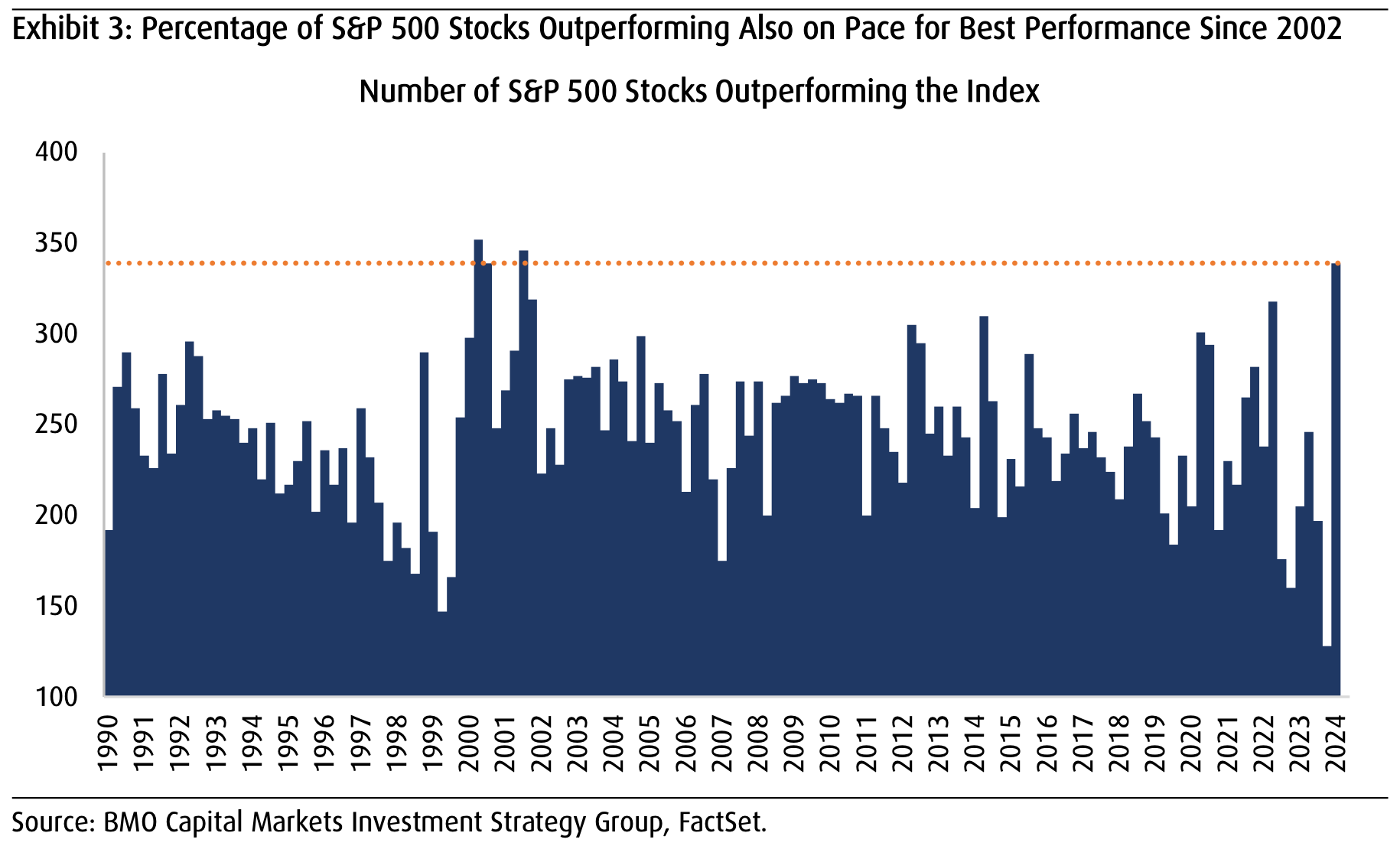

More Stocks Are Outperforming In Q3

As we always say, earnings are the most important long-term driver of stock prices (see TKer Stock Market Truth No. 5). And so if earnings growth prospects are broadening out, then it shouldn’t be too surprising to learn that stock price growth is broadening out.

BMO’s Brian Belski flagged an interesting stat about this topic in his note to clients on Thursday (emphasis added): “It is no secret that a handful of mega-cap tech stocks have been the driving force behind market gains for much of the past two years and this has led to concentration worries amongst investors given the bloated valuations of some of these stocks. However, an interesting development has occurred alongside the most recent market rebound during 3Q – these stocks have underperformed the rest of the index for the first time in nearly two years and is something we find reassuring since the S&P 500 is nearing records again without this segment of the market leading the way. In addition, participation levels have also improved dramatically since 3Q started as 339 S&P 500 stocks have outperformed the broader index – the highest level in about 22 years.“

(Source: BMO)

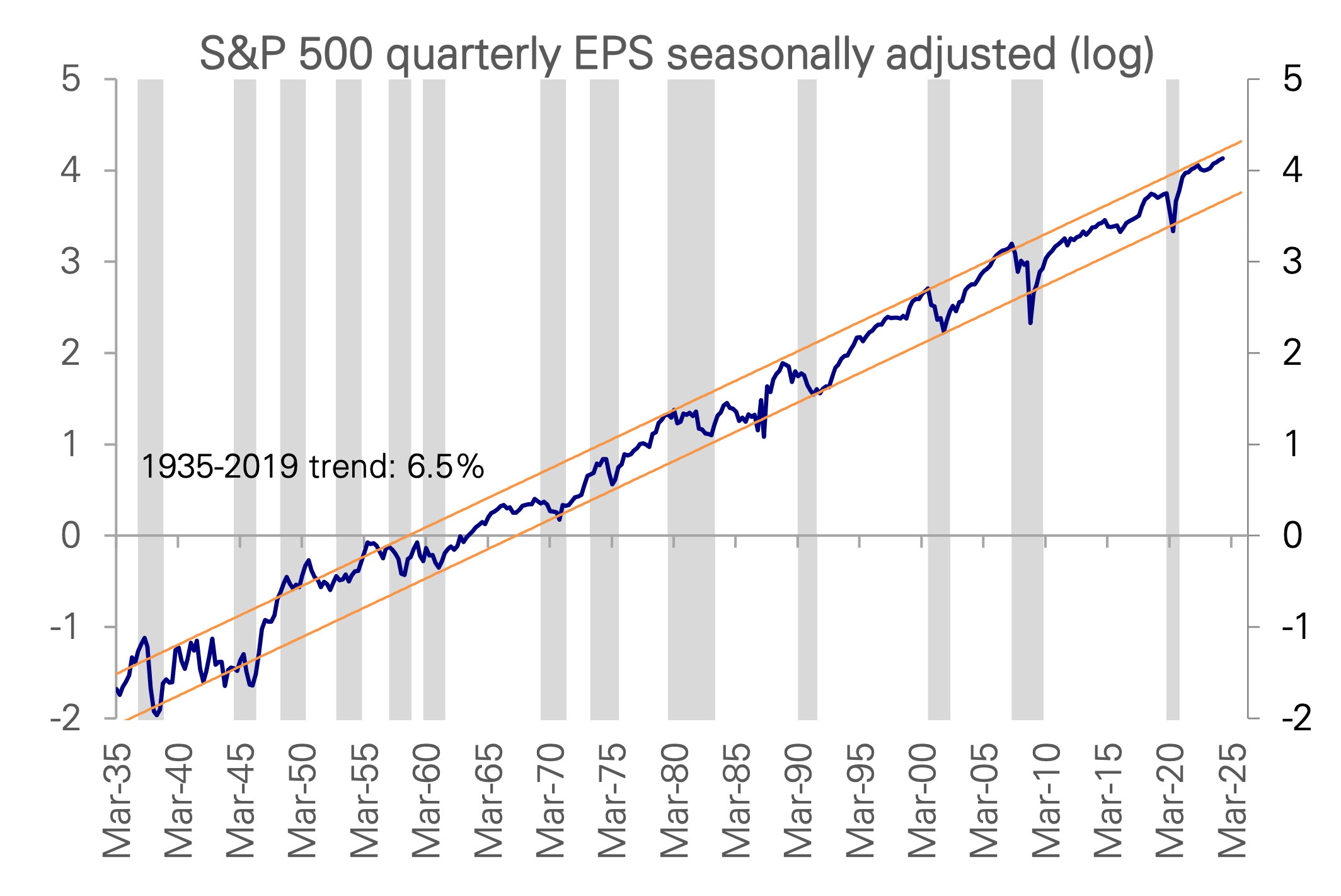

Earnings Usually Go Up

The U.S. stock market has been going up for a very long time. Why?

Because earnings have been going up for a very long time. Just take a look at this very long-term chart of S&P 500 earnings per share from Deutsche Bank:

(Source: Deutsche Bank)

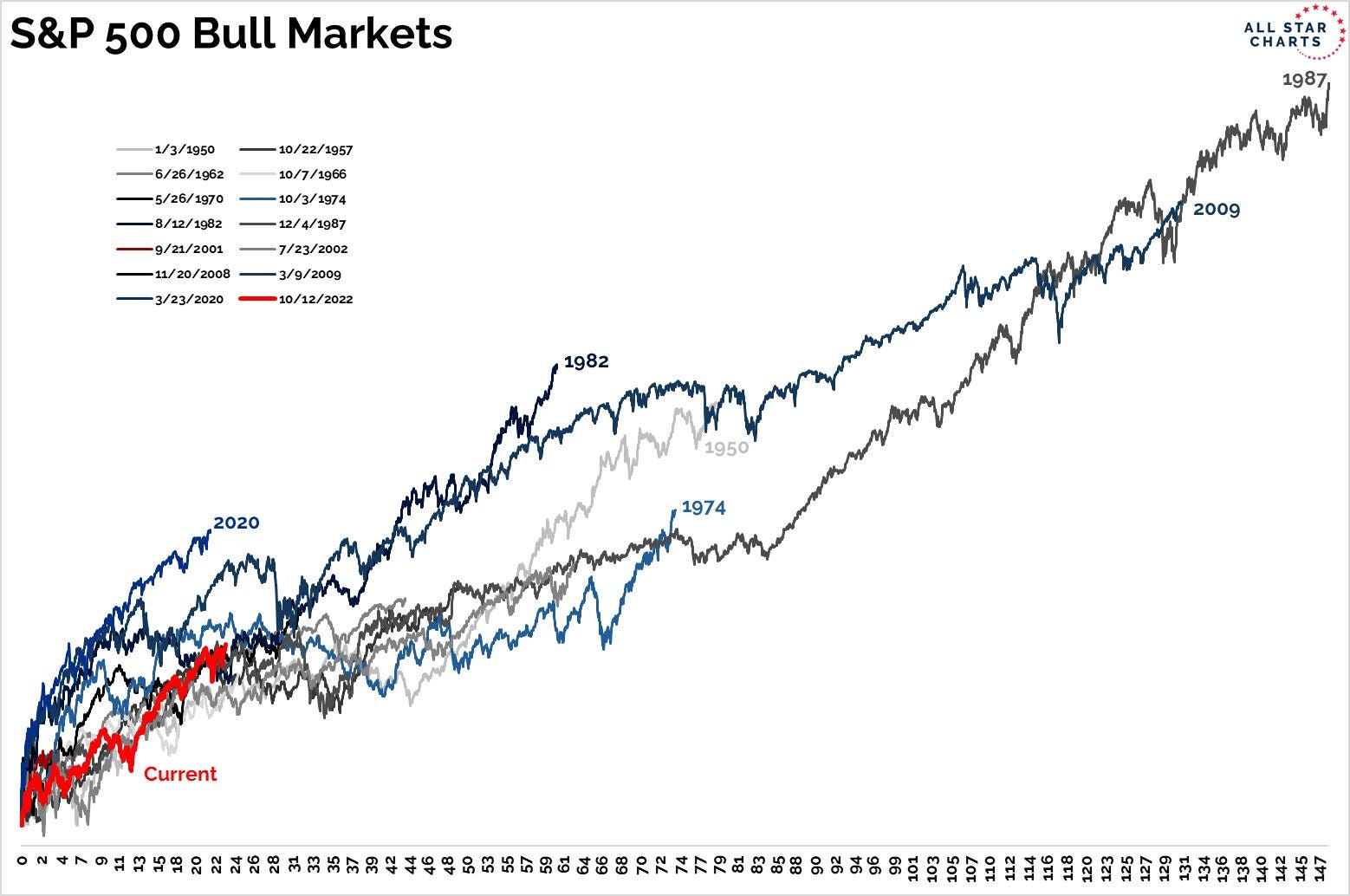

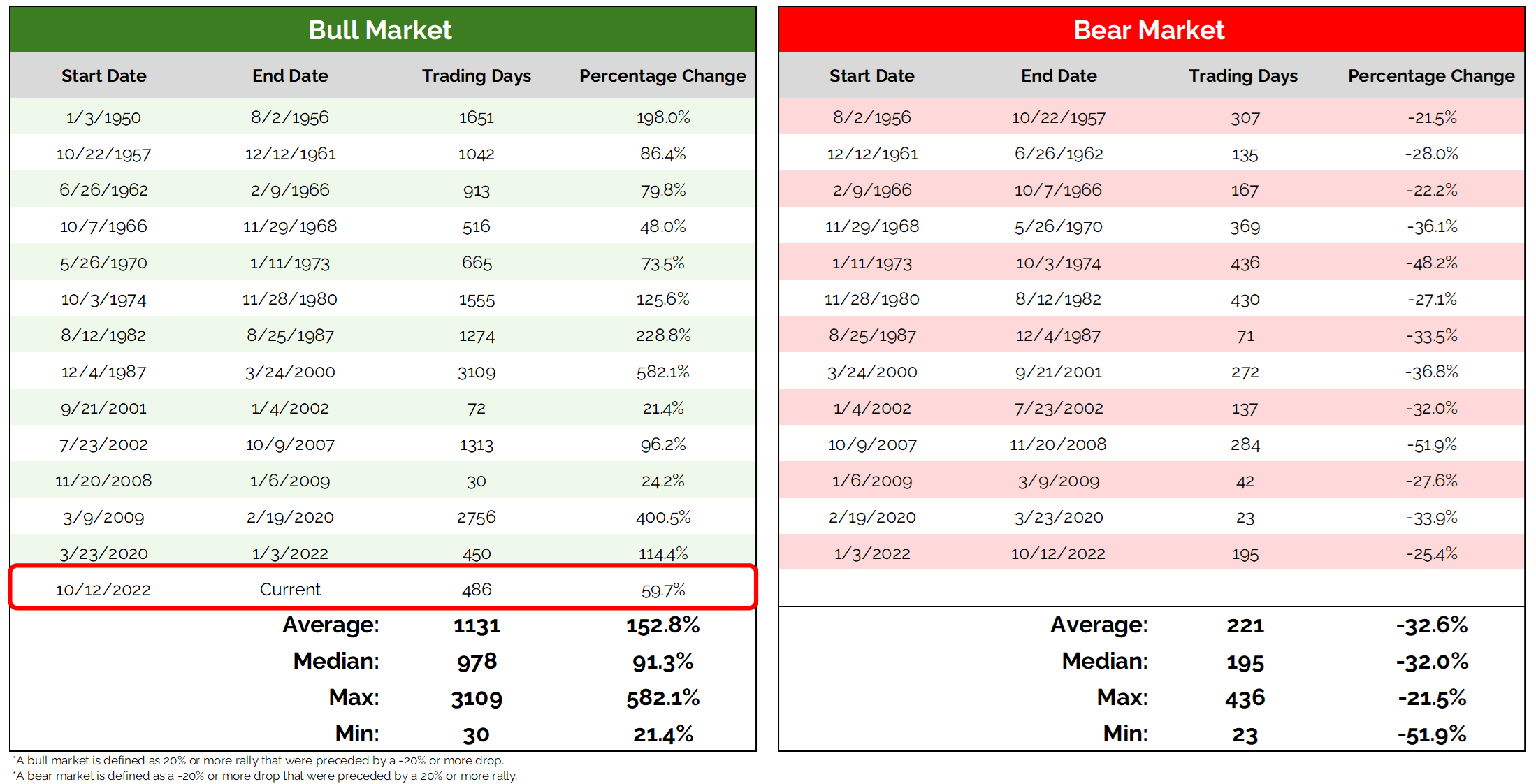

This Bull Market Is Young

We’re almost two years into this bull market. Does that mean we’re nearing the end of this rally?

On Friday, All Star Charts’ Grant Hawkridge charted the path of history’s bull markets. “So far, it is below-average,“ he said.

(Source: @GrantHawkridge)

Grant shared a more detailed look at the historical numbers. The median bull market lasted 978 trading days. The average was 1,131 days.

(Source: @GrantHawkridge)

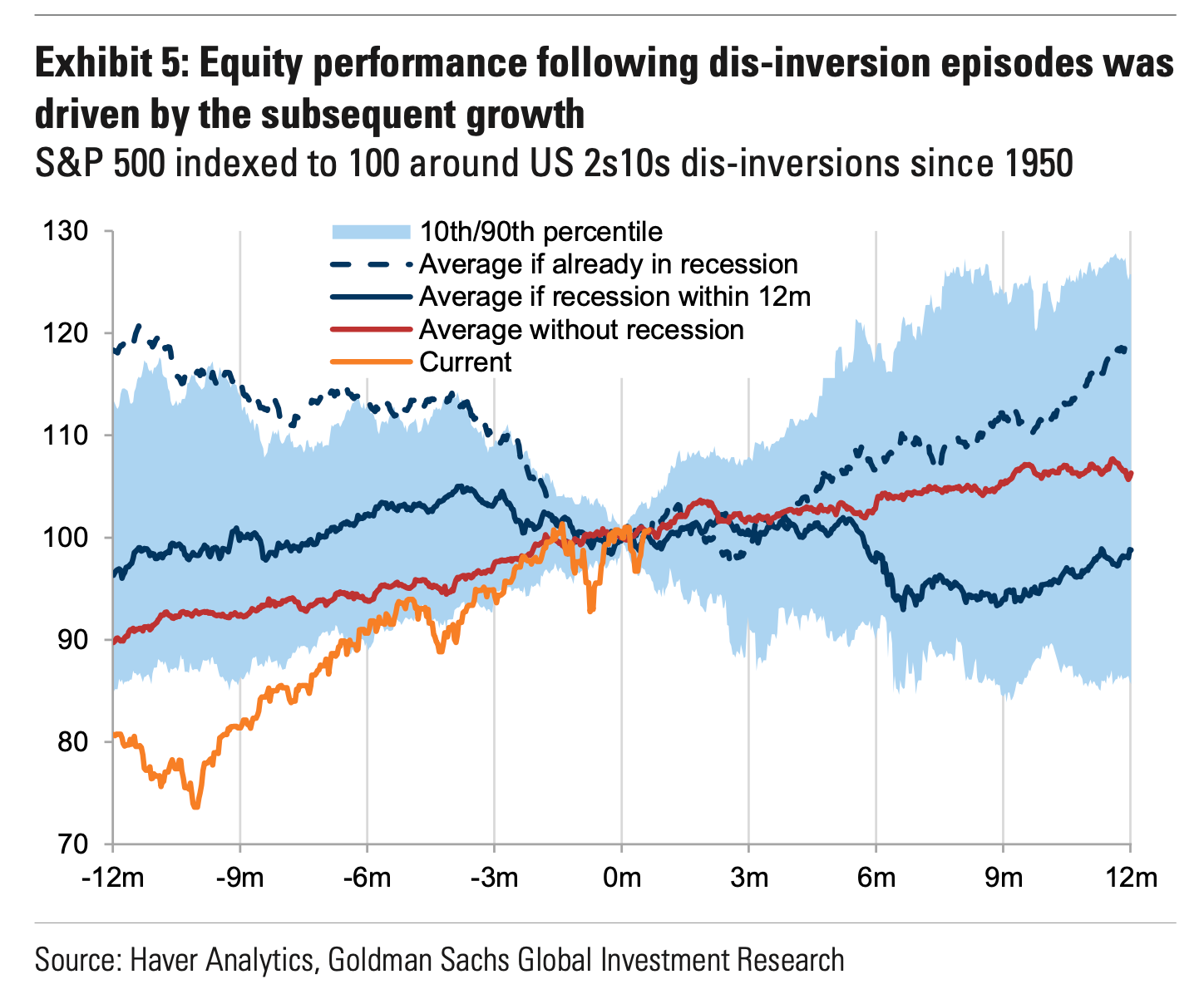

When The Yield Curve Disinverts

As TKer subscribers know, I’m not crazy about reading too much into single metric market indicators like the yield curve. More here and here.

That said, the yield curve gets a lot of attention and it recently disinverted.

Here’s what Goldman Sachs recently observed about yield curve disinversions and the stock market: “On average, US equities delivered the strongest forward returns if the US economy was already in a recession at the time of the US 2s10s dis-inversion – the market usually would have already sold off at the start of the recession and rebounded not long after the yield curve dis-inverted. Unsurprisingly, equity prices tended to consolidate if the yield curve dis-inversion was followed by a recession within the following year. On the other hand, equities typically delivered positive albeit low returns if the US economy avoided a recession.”

(Source: Goldman Sachs)

Long story short, the real signal comes from whether or not the economy goes into recession, which the yield curve hasn’t been particularly helpful in predicting lately.

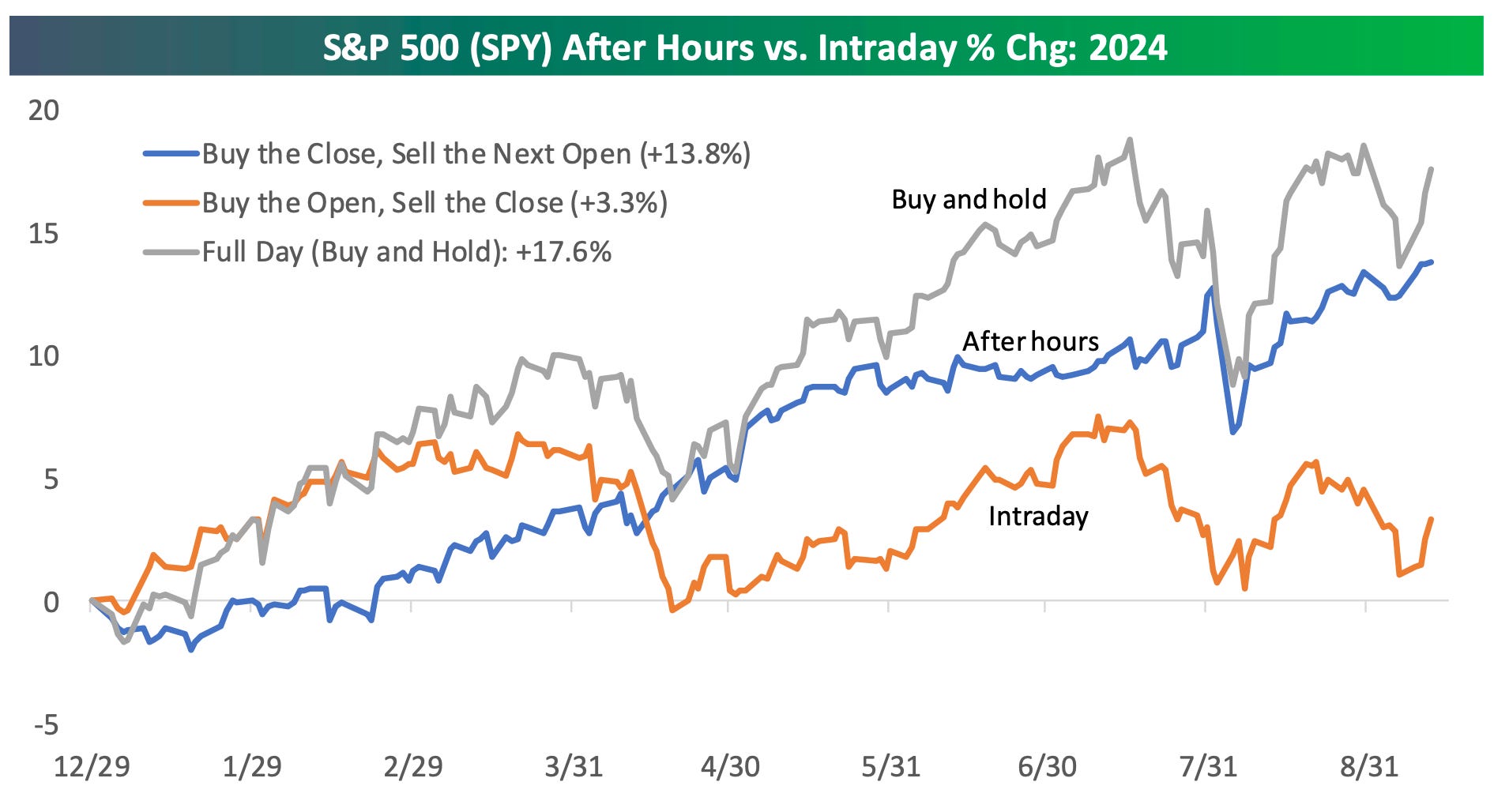

Much Of The Stock Market’s Gains Have Come When The Market Is Closed

Bespoke Investment Group makes some of the most fascinating observations in their killer research.

In their Sept. 13 note to clients, they observed: “…this year, nearly all of the market’s gains have come from moves outside of regular trading hours. As shown, had you hypothetically bought SPY at the close every day and sold it as the next open, you’d be up 13.8% this year. Had you done the opposite and bought SPY at the open every trading day and sold it at that day’s close, you’d be up just 3.3%.“

(Source: Bespoke)

Who knows what explains this phenomenon? And who knows if it’ll continue?

All I know is I’m not crazy about trading in and out of the market at such a high frequency.

In fact, one of my favorite quotes about investing comes from Bespoke’s Paul Hickey: “A one-day holding period, it’s a coin flip. The longer you’re willing to stick to it, the better. … Markets have never been down over a 16 year stretch or longer. Time heals in the markets.”

A version of this post was originally published on Tker.co.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.