Exports became even more important to China's economy in recent years as COVID curbed domestic consumption and a credit crunch squeezed property development. Now, Western demand for Chinese containerized exports has dropped just as the post-COVID rebound in Chinese domestic spending is faltering.

"People really expected China to come out and really accelerate but the Chinese recovery has been really poor," said Ole Slorer, head of infrastructure and energy at investment bank BTIG, at the Marine Money Week conference on June 22.

Chinese stimulus is still believed to be coming, but there is growing sentiment that it won't be big enough — or raw materials-intensive enough — to jump-start bulk commodity shipping rates. "After the global financial crisis, China engaged in a mega-stimulus. We should not expect to see a mega-stimulus this time around," said Duncan Wringley, chief China economist at Pantheon Macroeconomics, during a presentation on June 20.

As for China's all-important containerized exports, the spot rates tell the story: The Freightos Baltic Daily Index for the China-North America West Coast lane put spot rates at just $1,190 per forty-foot equivalent unit on Tuesday. That's down 17% from June 6 and 14% year to date.

Average spot rates in USD per FEU. (Chart: FreightWaves SONAR)

Exports Playing A Bigger Role In Steel Demand

"China drives everything in the dry bulk shipping world and everyone seems to be waiting for this big stimulus, which always seems to be right around the corner," said Serafino Capoferri, associate director of asset manager Macquarie, at Marine Money Week.

Shipping rate optimism rests on stimulus in the property and infrastructure sectors that would hike demand for steel and thus demand for imported volumes of iron ore and metallurgical coal.

Macquarie's Serafino Capoferri. (Photo: Marine Money/David Butler)

But Capoferri stressed the importance of Chinese exports to steel, and by extension, Chinese dry bulk imports. "One point that is very important to make, especially when you're thinking in terms of stimulus, is that since the pandemic, the manufacturing sector has played a much bigger role when it comes to overall steel consumption in China.

"Very often in this industry [shipping] we think it's all about property development, but in reality, manufacturing's share of total steel demand has grown, really driven by this export boom we've seen since 2020. Clearly, China remains the factory of the world, and exported goods contain a lot of commodities and a lot of steel."

The best example of steel use in exports (albeit noncontainerized) is automobiles. Chinese auto exports have tripled since 2020.

Altogether, Macquarie estimates China indirectly exported 143 million tons of steel via goods exports last year, or 14% of production, not including direct exports of finished steel. The numbers "highlight how important manufacturing has become and how exposed China is to the ex-China cycle," said Capoferri.

‘Pronounced Slowdown' Of Exports In 2nd Half?

Wringley said, "Demand is slowing down and where's that demand slowing down? Number one, on the external side of things. Manufacturing is cooling, quite obviously."

China's goods exports bounced in March then fell back. "The strongest reason for the bump in March was the catch-up with back orders that built up during the zero-COVID policy and the exit [infection] waves as zero-COVID was dropped," Wringley said.

"That brief catch-up period has already begun to fade as we go into June and the second half of the year. If you look around the world, global demand is clearly slowing. If you look at other Asian countries like Korea, exports have been falling quite sharply.

"There will be a little bit of a cushioning effect as China has managed to diversify exports to nontraditional markets, like Belt and Road [supply chain partner countries], like — notoriously — Russia, and to some other countries. But I think that can only partly mitigate what is going to be a pronounced slowdown of exports in the second half of the year."

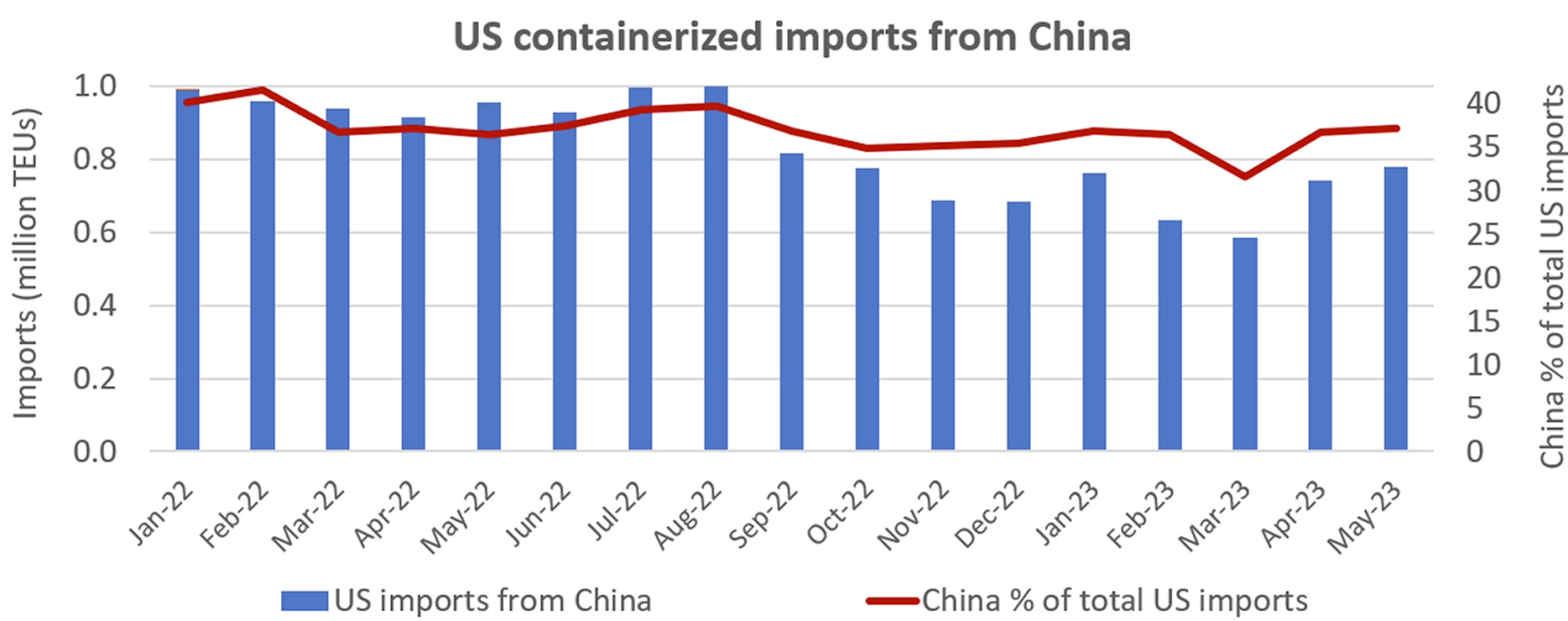

Data from Descartes shows that U.S. containerized imports from China have followed the same pattern as the broader market, falling back from one-off COVID-era peaks. U.S. imports from China in January to May were down 26% from the same period last year.

(Chart: FreightWaves based on data from Descartes Datamyne)

‘They Don't Want Another Big Debt Hangover'

According to Pantheon, manufacturing accounts for 27.5% of production inputs to Chinese GDP, with construction at 53.5%, services at 12.1% and other production at 6.9%.

Dry bulk shipping has historically benefited from Chinese stimulus that spurs construction. But Wringley said there are risks that "are holding back the government from pushing the traditional stimulus pedals in the property sector or really boosting infrastructure."

"They don't want another big debt hangover," he said. In addition, "there are just fewer economically productive opportunities for investment" in property development and infrastructure. "The more you try to accelerate infrastructure, the more local governments reach for those ‘white elephant' projects."

Wringley believes there will be stimulus, but "it will be pretty limited stimulus."

Stimulus Upside: ‘Nothing Too Cray-Cray'

According to Capoferri, "There's no question the government is moving more and more toward supporting the economy, but we don't think we're going to see a big push on property this time around. The structure of the Chinese economy has changed. Services are much more important than they used to be, and manufacturing as well.

"The property sector faces a lot of structural challenges. It‘s obviously a saturated market in the sense that urbanization is slowing and demographics are not as favorable, so pushing that sector would bring risks, particularly around financial stability, and we think the Chinese leadership is aware of this.

"That's why we think these hopes of a big push for property have been consistently disappointed. The market has been waiting for a property stimulus for 12-18 months and it hasn't happened.

"What we think is more likely is more targeted support measures around other sectors. And within the infrastructure basket, we think it will focus on areas like the power grid and the energy transition — and unfortunately [for commodity shipping], those are not super steel-intensive."

Pessimism on stimulus upside for dry bulk rates is growing. "New stimulus measures could bring a little boost to the market, but nothing too ‘cray-cray," said ship brokerage BRS.

Crude Imports Strong But ‘Signs Of Weakness' Emerge

Amid the daunting outlook for container exports and unexceptional outlook for dry bulk imports, China's liquid bulk imports have outperformed. Liquefied gas carriers transporting propone from the U.S. to China are in high demand, and Middle East-to-China oil volumes supported a temporary spike in supertanker rates earlier this month.

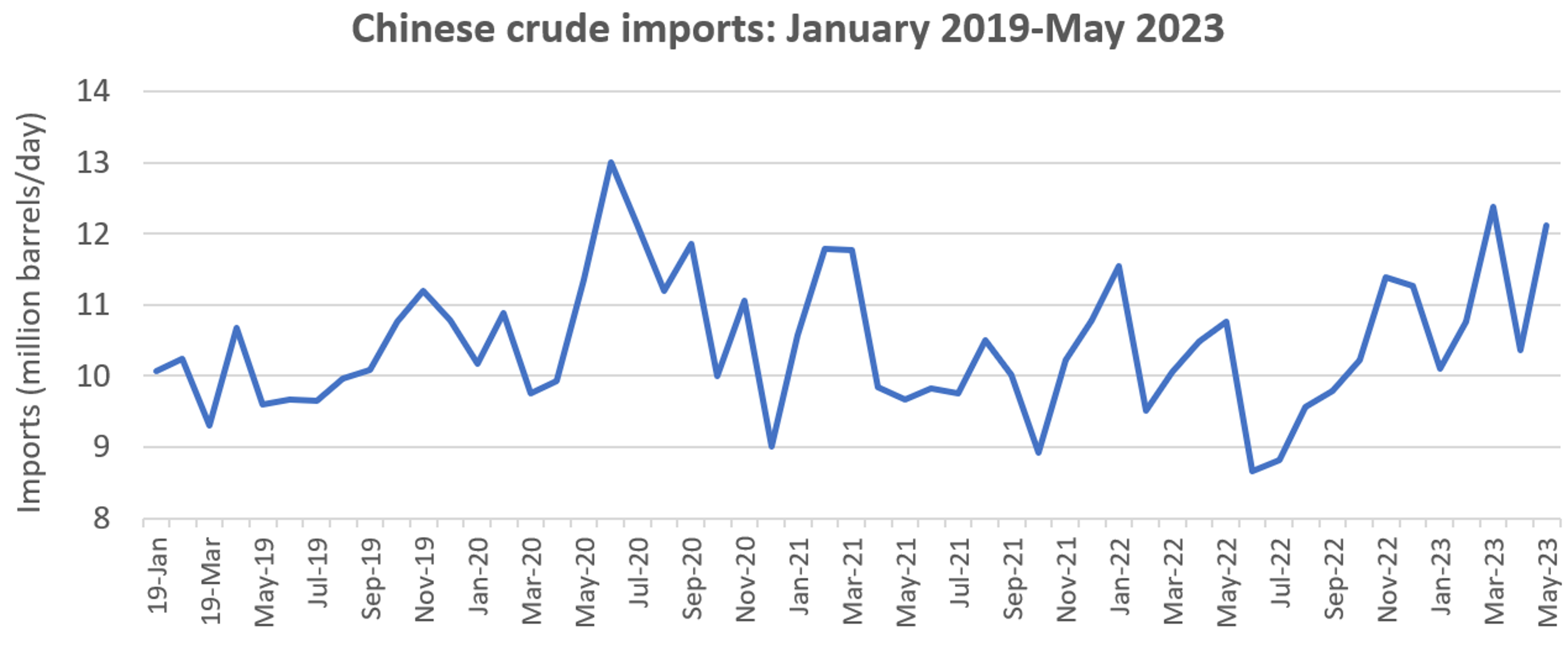

According to data from price-reporting agency Argus, China's crude imports averaged 12.1 million barrels per day (b/d) in May and 12.3 million b/d in March. The only two months on record with higher volumes were June and July 2020, when COVID heavily depressed crude prices.

(Chart: FreightWaves based on data from Argus)

Yet here too, there are bearish signs that Chinese shipping volumes may not grow as much as hoped.

Ship brokerage Braemar said Wednesday the Chinese National Petroleum Co. cut its 2023 forecast for China's year-on-year oil demand growth to 3.5%, from 5.1%.

Brokerage and consultancy Poten & Partners said Friday that "jet fuel demand growth is lagging … [and] one of the key reasons is China. While domestic flights are booming, international flights are lagging." Poten said "growth in China's international flights has been focused on regional flights with destinations in Southeast Asia" — short-haul routes that consume much less fuel than long-haul routes to North America and Europe.

Argus said in mid-June that crude prices had eased "on slower-than-anticipated Chinese demand growth."

Argus reported Friday that "Chinese crude imports … continue to pile up in storage tanks" while apparent refined products demand — refinery output plus net products trade — dropped by 560,000 b/d in May versus April. "Chinese oil demand remained high in May but emerging signs of weakness suggest a significant pullback is in the cards," warned Argus.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.