The Opposite Day Issue

This week, economic data decided to pull a George Costanza and do the opposite of everything it has been doing. DKI has highlighted the trend of inconsistent data in recent months, and this week, many of those inconsistent trends reversed. Confusing? Don’t worry, we’ll explain.

We also have some excellent fundamental news from Shockwave Medical ($SWAV), rising visitation in Macau (great for $LVS), and Japan enters recession. Plus, we highlight detailed comments on oil price projections from Tracy Shuchart (@chigrl) who did a fantastic webinar with DKI this week.

This week’s 5 Things contains 7 Things. Are we delivering extra value or just have difficulty counting. You decide.

This week, we’ll address the following topics:

-

The CPI comes in hot. Does this mean “higher for longer”?

-

The PPI comes in hot. Does this also mean “higher for longer”?

-

Retail sales came in weak while manufacturing exceeds expectations. This reverses our prior trend of weak manufacturing and strong consumer sales.

-

Shockwave Medical SWAV beats earnings expectations. The company isn’t just taking share. It’s growing the market.

-

Macau visitation for Chinese New Year well above expectations and rivaling the pre-pandemic 2019 numbers. Great news for Las Vegas Sands ($LVS).

-

Japan officially enters recession. The currency isn’t doing so great either. DKI has been highlighting problems with the Japanese central bank for well over a year.

-

Tracy Shuchart thinks oil remains range-bound this year. Does that mean there’s no opportunity? Of course not!

Ready for a new week of reversals? Let’s dive in:

-

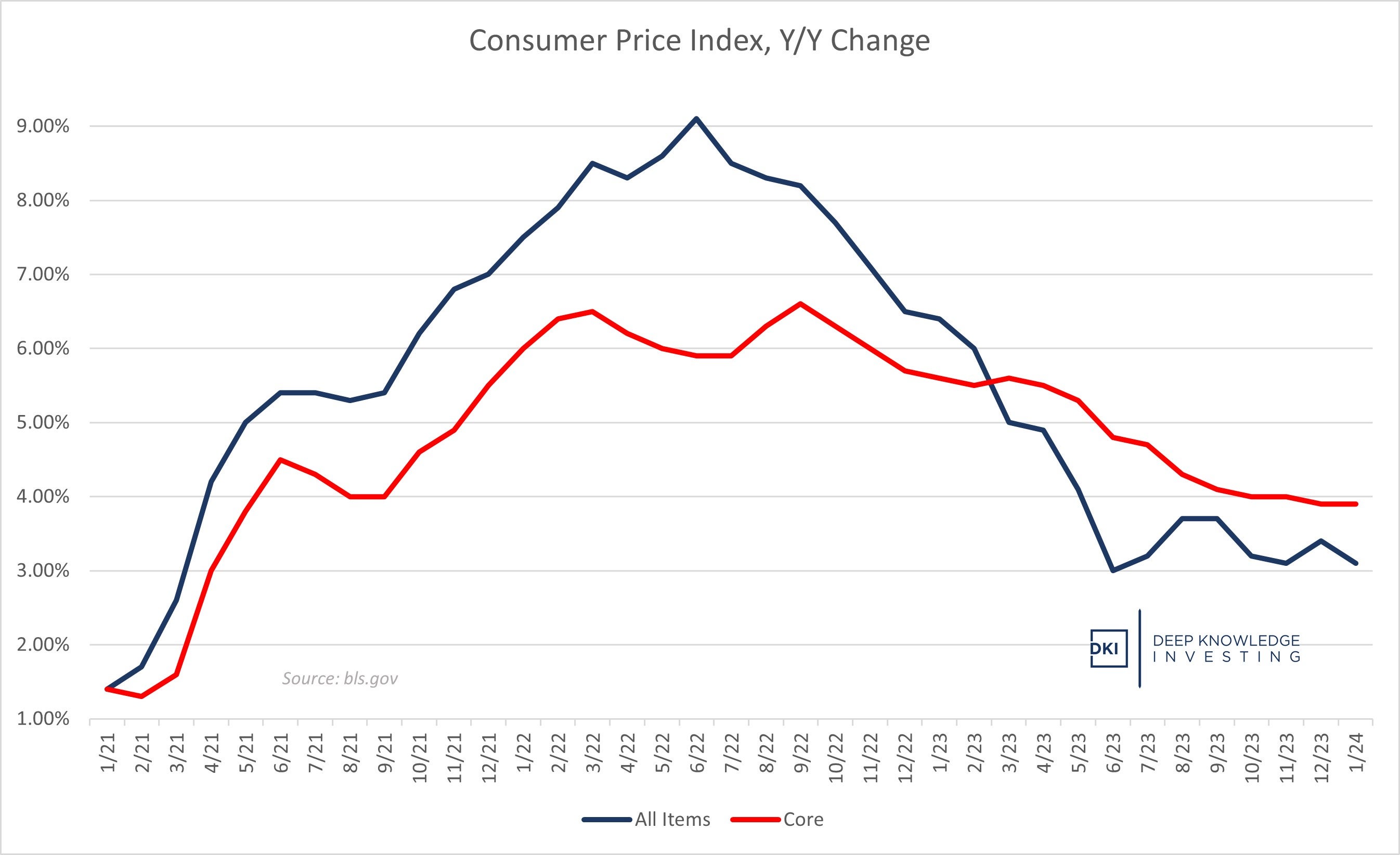

January CPI is Above Expectations:

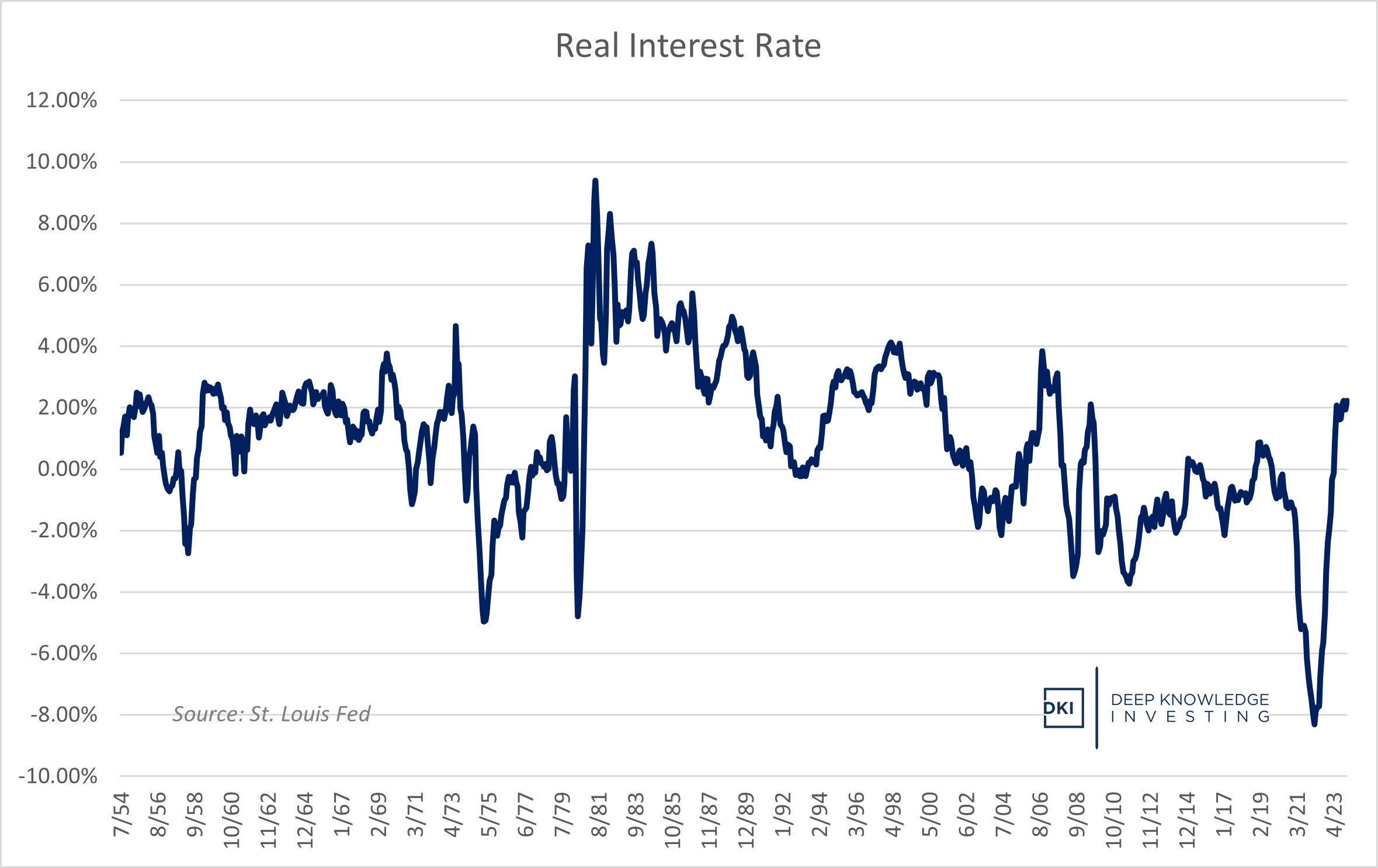

The January Consumer Price Index was up by 3.1% which was above the 2.9% expected. The Core CPI, which excludes food and energy, was up 3.9% for the year and up .4% from last month. That was above the 3.7% and .2% analysts had projected. Real interest rates remain around 2% which isn’t out of line from historical readings. Services prices up another 5.4% has been an ongoing (sticky) problem for the Fed. I continue to be skeptical at the food inflation numbers. The government is telling us that food at home is up 1.2%. Does that match your grocery bill?

CPI still above the 3% mark. Core CPI still about double the target. Both higher than expected.

Asset gatherers keep saying the Fed has overtightened. 2% Real rates seem ok to me.

DKI Takeaway: Asset gatherers, who get paid based on assets under management, have been begging the Federal Reserve to lower the fed funds rate and get the zero-interest rate/quantitative easing free-money party started again. The market had been expecting a rate reduction in January or March which then got pushed out to May. The hot CPI print is pushing first rate-cut expectations out to June. DKI has been saying all along that those who have been expecting 6 rate cuts (1.5%) this year will be disappointed. Say it with me: “higher for longer”.

-

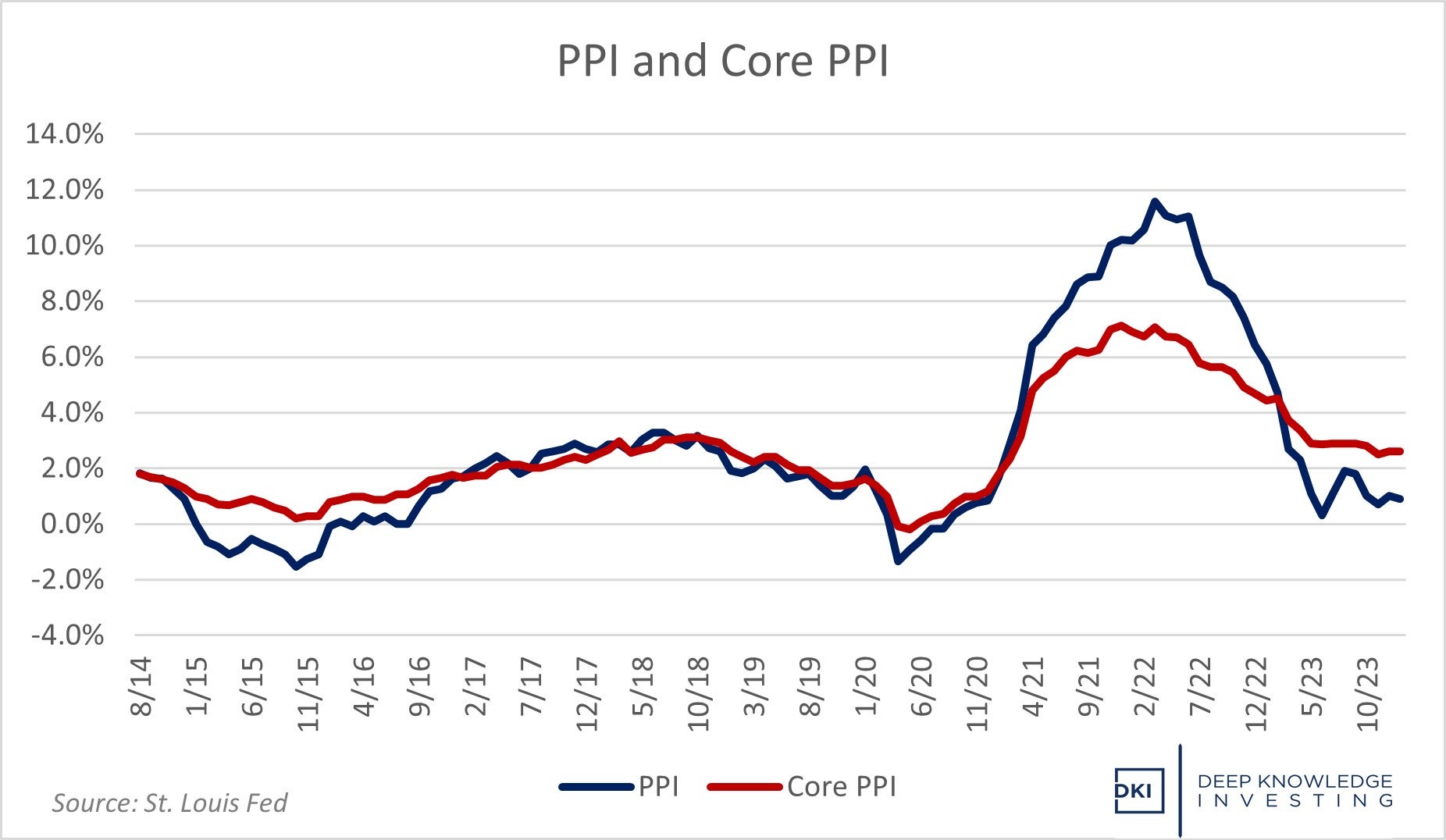

The PPI Agrees with the CPI:

The Producer Price Index (PPI) is like the wholesale version of the CPI. In general, a higher PPI means higher consumer prices are on the way. This week, the PPI was up .3% from last month vs expectations of .1%. This was a reversal from last month’s negative reading so we’ve gone from deflation back to inflation. Core PPI, which excludes food and energy, was an even bigger surprise. Core rose by .5% vs last month which was far above expectations for a .1% gain. To put this in perspective, a .1% gain annualizes to just 1.2%. A .5% monthly gain annualizes to 6.2%. One is well below the 2% annual target. The other is a disaster.

PPI up .9% vs last year is good. Core up 2.6% vs last year is ok. It’s the monthly that’s the problem.

DKI Takeaway: Last month, many were excited by the negative print for the monthly PPI. Because producer prices make their way into future consumer prices, there was hope that the CPI was about to fall as well. This month, we saw monthly increases in the PPI above expectations. The conclusion: “higher for lon…”. At this point, you all know the drill.

-

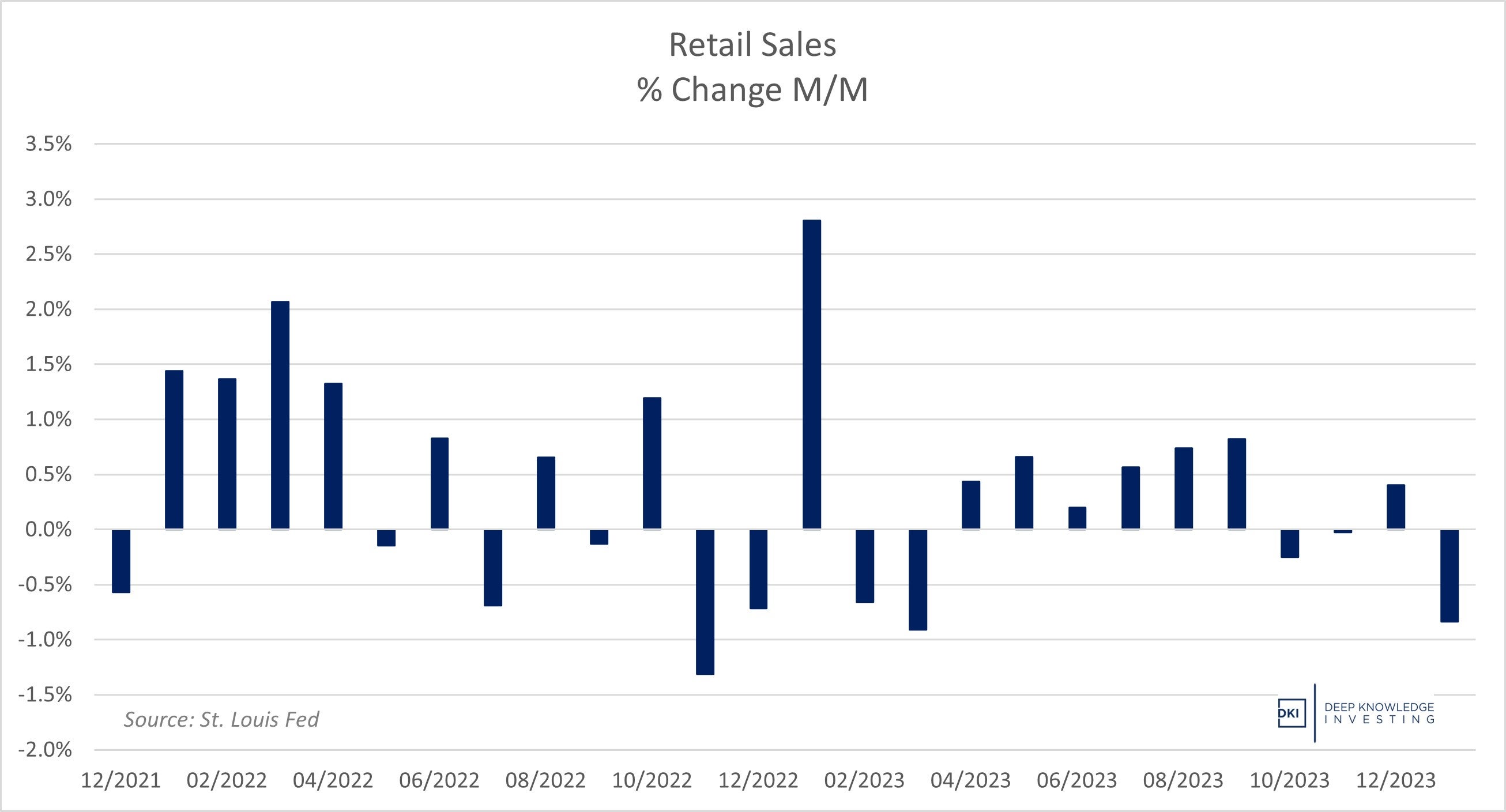

Retail Sales and Manufacturing Data Reverse:

Despite widespread dissatisfaction with the economy, the American consumer continued to spend…until January. Advance retail sales were down .8% for the month which was much worse than the negative .3% expected. Making things even rougher, last month’s strong retail sales of up .6% were revised down to .4%.

The “strength” of the economy just turned.

DKI Takeaway: DKI has been writing about how the strong consumer data didn’t match the very weak manufacturing data. This week, those trends reversed. The bad sales results were paired with a huge rebound in manufacturing. The Philadelphia manufacturing index was at 5 which is 16 points above last month and a huge beat against expectations for negative 8. The New York survey was negative 2. That doesn’t sound great until you compare it to the January reading of negative 44 and expectations of negative 15. We’ll be watching to see if recent strong consumer sales led these businesses to increase projections, and if recent sales weakness causes another future reversal.

-

Shockwave Medical ($SWAV) Beats Earnings Expectations and Grows the Market:

This week, Shockwave announced 4Q revenue growth of 41%. EPS of $1.16 were far above analyst expectations for $.89. The company highlighted international sales and peripheral sales as areas of future growth which is something DKI has written on previously. The new Costa Rican manufacturing facility will start production this year and will contribute to margins next year.

Procedure volume is up huge since Shockwave entered the market.

DKI Takeaway: The chart shows why we’re so bullish on $SWAV. Shockwave’s IVL device was approved in Q1 of 2021. Since then, it’s taken about 50% share for advanced procedures requiring mitigation of excessive calcification that can make placing a stent difficult and dangerous. More importantly, once IVL was approved, these advanced procedures went from about 11% of the market to 16%. More people are getting better care in difficult cases because of Shockwave. DKI subscribers started buying the stock at $191 in December. It’s in the mid-$260s as I write this.

-

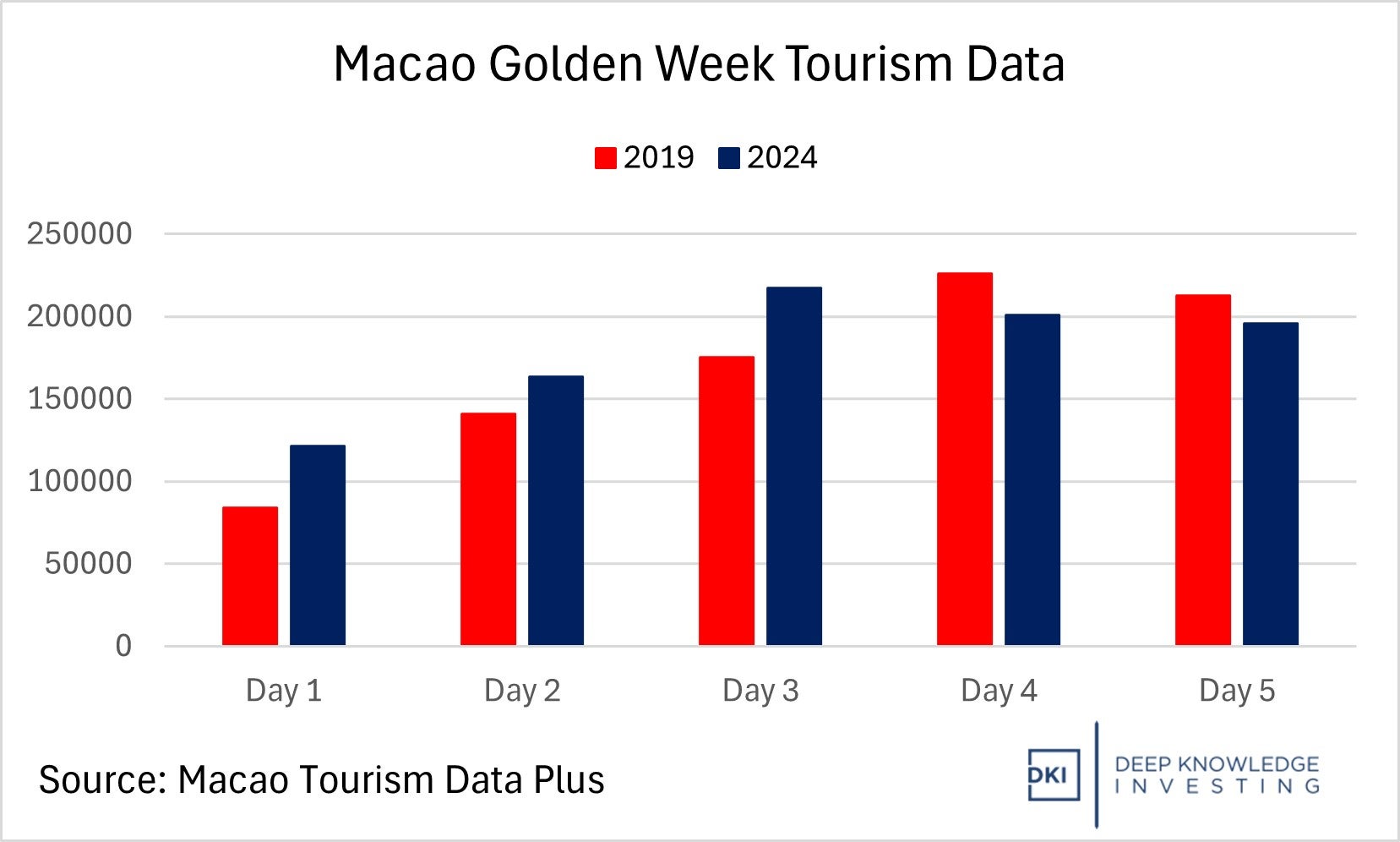

It’s Chinese New Year and Macau Visitation is Above Expectations:

Happy year of the dragon to all of you. In China, people are celebrating by returning to the Macau gambling tables at levels far above expectations. Visitation levels are challenging the pre-Covid 2019 numbers. Inside Asian Gaming reports that four days into an eight-day holiday, visitation is close to the 960k expected for the entire period. Visitation drops later in Chinese New Year, but it’s clear that the 2024 total will be well-above estimates.

We understand there have been concerns about the Chinese economy, but this looks like full recovery to us.

DKI Takeaway: DKI has been writing that Las Vegas Sands LVS stock represents full-recovery performance at a Covid-level distressed stock price. $LVS is up more than 20% in the last couple of months. Between 4Q stock buybacks and dividends, and a 1Q commitment to buy more of its own Macau assets through Sands China (1928.HK), $LVS has returned over $900MM of capital to shareholders in the last few months. If you want to know what we think its worth, or are interested in ideas like this, you’re welcome to subscribe.

-

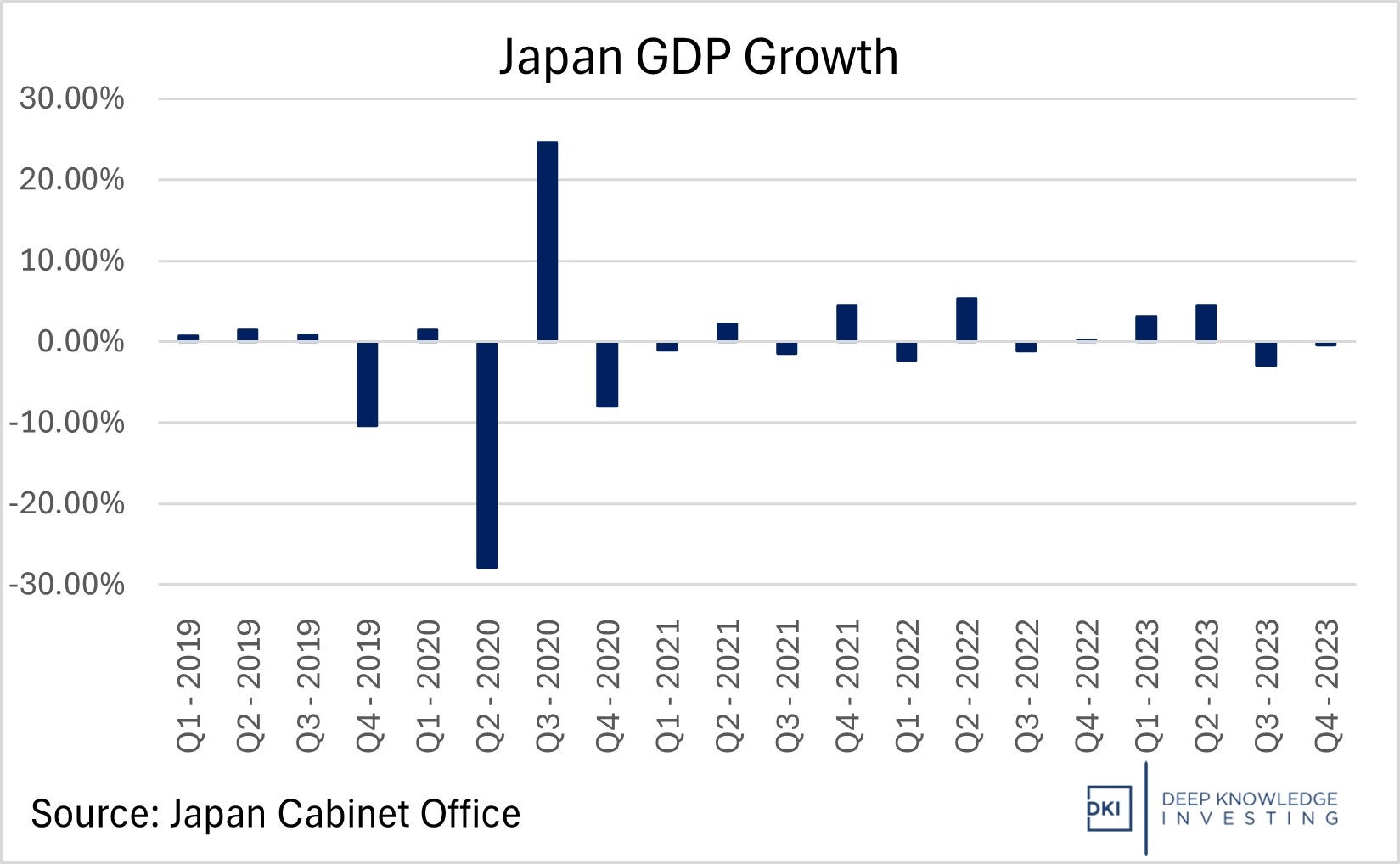

Japan Enters Recession – Yen Falls Again:

Not even a self-directed economic implosion in Germany could prevent Japan from falling from third to the fourth largest economy in the world. After years of up and down economic performance and decades of stagnation, Japan just recorded two straight quarters of GDP decline. Further complicating the economic picture there, the yen has fallen below 150 to the dollar again. Japan is a geographically small island nation and needs to import a lot including energy which is priced in dollars. Oil is getting increasingly expensive in yen.

It's not a terrible recession, but there’s no guarantee that GDP growth turns positive this quarter.

DKI Takeaway: DKI has been expressing concern about Japanese leverage since late 2022. Its massive debt was manageable as long as interest rates were around (or even blow) zero. With central banks all over the world raising rates, the Bank of Japan is stuck either watching the yen slide, or defending the yen and destroying the government budget as interest expense rises. Keynesian and modern monetary theory advocates love to claim that deficits and debt don’t matter. DKI disagrees. All this debt does is pull future demand forward. Here in the US, GDP growth is lagging growth in debt. Every dollar the government spends leads to less than a dollar of economic growth. As governments around the world take a greater role in the economy, growth is stalling and living standards are stagnating. Japan is our warning.

-

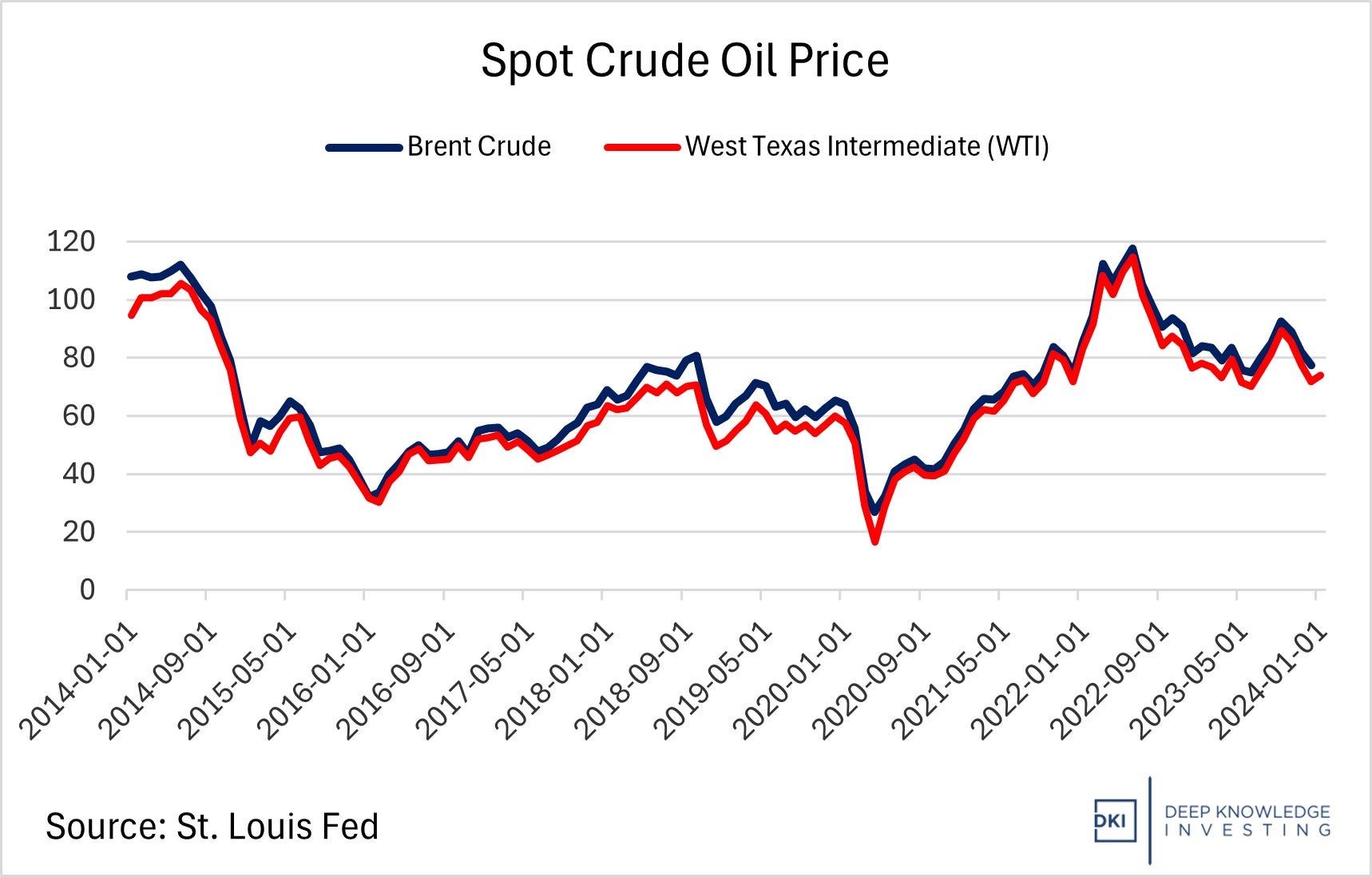

Tracy Shuchart (@chigrl) Gives Her Oil Prediction for the Year:

I had the pleasure of interviewing energy expert, Tracy Shuchart this week. We spoke for nearly an hour covering oil & gas, nuclear & uranium, precious metals, and geopolitics. The entire video is worth watching. Tracy outlined her thoughts on the oil market for this year. She thinks prices aren’t really out of line even though half the country is angry about high gas prices and energy investors are angry about oil prices below the 2022 highs. She thinks we stay range-bound for the rest of 2024 with a wide range.

Current prices are above the recent trend but below the 2022 highs.

DKI Takeaway: I think Tracy’s answer makes a lot of sense. If oil prices fall below the mid-$60s, we’ll lose US shale production. Close to or above $100 a barrel leads to worldwide economic stress. The Saudis don’t want oil prices to fall too far, but they also don’t want high prices to cause a worldwide recession. Long-term, energy demand will only grow and few exploration and production companies are investing much in future production additions. That means higher prices eventually.

Information contained in this report, and in each of its reports, is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied. DKI makes no representation as to the completeness, timeliness, accuracy or soundness of the information and opinions contained therein or regarding any results that may be obtained from their use. The information and opinions contained in this report and in each of our reports and all other DKI Services shall not obligate DKI to provide updated or similar information in the future, except to the extent it is required by law to do so.

The information we provide in this and in each of our reports, is publicly available. This report and each of our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion in this and in each of our reports are precisely that. Our opinions are subject to change, which DKI may not convey. DKI, affiliates of DKI or its principal or others associated with DKI may have, taken or sold, or may in the future take or sell positions in securities of companies about which we write, without disclosing any such transactions.

None of the information we provide or the opinions we express, including those in this report, or in any of our reports, are advice of any kind, including, without limitation, advice that investment in a company’s securities is prudent or suitable for any investor. In making any investment decision, each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable, based on this or any of its reports, or on any information or opinions DKI expresses or provides for any losses or damages of any kind or nature including, without limitation, costs, liabilities, trading losses, expenses (including, without limitation, attorneys’ fees), direct, indirect, punitive, incidental, special or consequential damages.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.