This was a fascinating week featuring political shifts, increased market volatility, and a week-long drop in the stock prices of the mega-cap tech leaders that have been supporting the equity market indexes the past couple of years. This week, we’re focused on higher retail sales and wondering if anything will slow the consumer. Higher jobless claims make people think the Fed is almost 100% certain to cut rates by September. China is trying to keep its banks from imploding. Treasury Secretary, Yellen, is shortening the duration of the government bond market leading to larger auctions with less comparative demand. (Don’t worry – we’ll explain.) Finally, I address some critics who insist that all would be fine if we could just get people to pay more in taxes. As usual, DKI Interns, Alex Petrou and Andrew Brown, come through with their usual high-quality work and excellent analysis.

This week, we’ll address the following topics:

-

Retail sales stronger than expected. Rate cut expectations still increased?!

-

Jobless claims come in high. Rate cut expectations increased.

-

The Magnificent Seven’s Awful Terrible Week.

-

China throws liquidity at its banking sector.

-

Treasury auctions getting larger and weaker.

-

Tax receipts vs government spending: Which one is out of line?

Ready for another week of waiting for rate cuts (or Godot)? Let’s dive in:

-

Strong Retail Sales and Possible Rate Cuts:

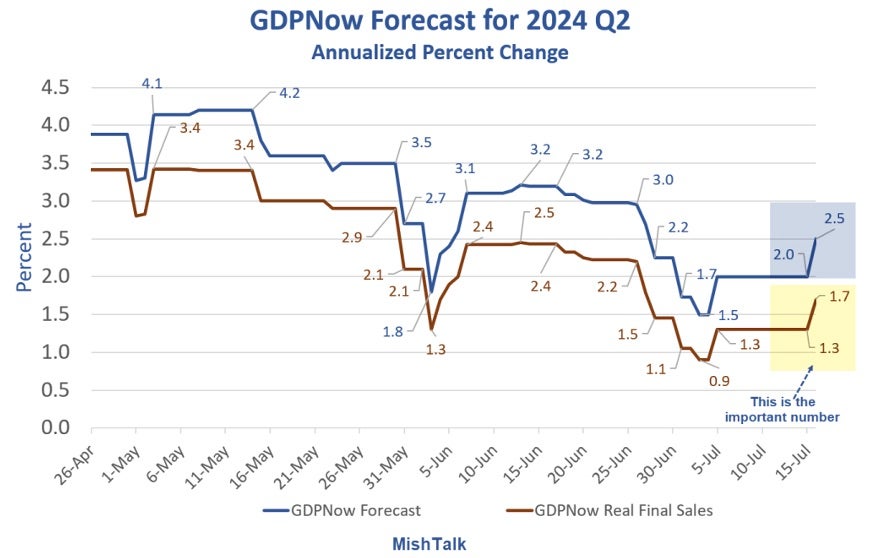

Recent adjustments to the GDPNow model, which estimates U.S. economic growth in real-time, indicate a more robust second quarter for 2024 than initially anticipated. The nowcast has increased from 2.0 percent to 2.5 percent, fueled by stronger than expected retail sales and a rise in personal consumption expenditures from 1.6 percent to 2.1 percent. Real final sales also improved, climbing from 1.3 percent to 1.7 percent.

Graph from https://mishtalk.com/economics/better-than-expected-retail-sales-boosts-gdpnow-nowcast/

DKI Takeaway: This marker of economic strength complicates the case for a Federal Reserve rate cut. Despite the market pricing in a 98.1 percent probability of a rate cut in September, up from 67 percent a month ago, this optimism may be misplaced. The Fed typically responds to weaker economic conditions or subdued inflation, neither of which align with the current robust retail sales data and GDP projections. With consumer spending proving resilient, the Fed may find it prudent to maintain current rates to avoid fueling inflation further. Analysts projecting a high probability of a rate cut might also be underestimating the Fed's cautious stance. The central bank is likely to weigh the solid economic data heavily against market expectations. Considering these indicators, it appears more plausible that the Fed will hold off on rate cuts (or at least more plausible than the market thinks). DKI maintains its position that the Fed, and specifically Chair Jerome Powell, are more concerned about reigniting inflation by cutting rates too soon. Additionally, cutting rates before an election could be perceived as politically motivated, a scenario the Fed is keen to avoid in order to maintain the perception of political neutrality.

-

Jobless Claims Come in High:

For the week ending July 13th, initial jobless claims in the United States surged to 243,000, up from 223,000 the previous week. This increase of 20,000 claims exceeded the original estimate of 229,000 by 14,000. Several factors may have contributed to this unexpected rise. One significant factor was Hurricane Beryl, which impacted Houston last week, potentially leading to a temporary increase in jobless claims due to disruptions in businesses and employment. Additionally, the end of a U.S. holiday period can sometimes lead to fluctuations in jobless claims as seasonal employment adjusts. Despite the caveats, this is a sign of a cooling labor market.

This isn’t even close to awful, but the recent trend hasn’t been great.

DKI Takeaway: This week’s spike in claims is significant as the unemployment rate continues its gradual ascent to the highest level since January 2022 (4.1%). With the labor market showing signs of cooling, there is increasing pressure for the Federal Reserve to consider pivoting towards rate cuts. Many are hopeful that a rise in unemployment might prompt such a move by Chair Powell. However, the Federal Reserve must navigate its dual mandate carefully. Although inflation is decreasing, it has yet to reach the 2% target, and unemployment is on the rise. Ultimately, the Fed will need to prioritize one objective over the other, with inflation remaining the biggest threat lurking in our economy.

-

The Magnificent Seven’s Awful Terrible Week:

After a week of economic uncertainty, tech stocks experienced a sharp decline. A major factor was former President Trump’s statement that the U.S. would not defend Taiwan if attacked by China, and suggesting that Taiwan should pay the U.S. for its defense. This caused a sell-off in chip stocks such as Nvidia NVDA, Taiwan Semiconductor TSM, and Advanced Micro Devices AMD. Microsoft MSFT also faced challenges due to a cybersecurity attack, which led to a drop in its stock price. Additionally, Netflix NFLX had a good quarter, but guided to 3Q revenue of $9.73 billion which was below the consensus estimate of $9.83 billion.

A bad week with NVDA and META down more than 10% from the prior week.

DKI Takeaway: A widespread tech sell-off has been anticipated for months. Over the past two years, we've witnessed a surge in the mega-cap Magnificent 7, but with the tech sector priced for perfection, it doesn’t take much for these stocks to fall. These companies have become expensive, and as the economy slows down, the tech sector may follow suit. Over the next couple of weeks, earnings reports from several of the Magnificent 7 will provide key indicators of market direction. Additionally, Tesla has reported a 24% drop in car registrations and Apple has seen multiple quarters of declining device sales, reflecting broader economic trends and product competition.

- China Throws Liquidity at its Banking Sector:

Amid rising deflationary pressures and a contracting property market, China is taking aggressive steps to stabilize its economy. @Peruvian_Bull recently reported on Substack (https://substack.com/home/post/p-146489585) that the People's Bank of China (PBoC) has injected over $100 billion into the banking system, marking the highest liquidity levels since February 2024. This move comes in response to a banking crisis where 40 Chinese banks have collapsed recently. Commercial banks are also facing declining profits with net interest margins dropping to historic lows of 1.73% by September 2023.

Malinvestment has put Chinese banks at risk. Graph by TradingView.

DKI Takeaway: As property investments contracted by 8% in 2023 and transaction volumes fell sharply, the PBoC's aggressive liquidity injection aims to stabilize the system and prevent further economic decline. The substantial liquidity boost underscores the gravity of the current economic situation and the lengths to which Chinese policymakers are going to manage deflationary pressures and support the financial system. @LynAldenContact, in a recent MacroVoices episode (https://open.spotify.com/episode/5U4QfgkraOEe0w1JJi6jBS?si=ac550bf98e074bbf), highlighted ongoing weaknesses in China’s housing market and consumer consumption, despite strong industrial production. She pointed out that these trends echo Japan’s disinflationary period, whereby highly indebted private debt bubbles lead to a rotation from the private sector to the public sector. The years of propping up the housing market is starting to show in a slow-motion unravelling on malinvestment. Referring to both Peruvian Bull and Lyn Alden this ‘intervention’ by the PBoC is not the largest liquidity injection by the Chinese government; however, if these issues persist, it is likely this will not be the end of China’s issues as this indebted system continues to unravel.

- Treasury Auctions Getting Larger and Weaker:

A long-standing DKI opinion is that government spending levels are unsustainable and are worsening. The government funds this excess spending through bond issuance, with each auction revealing different dynamics. Since COVID, Treasury Secretary, Janet Yellen, has shifted bond issuances toward the front of the yield curve, moving from long-dated bonds to short-term debt. This trend is concerning, as similar patterns were observed in Zimbabwe before its hyperinflation in the 2000s and more recently in Venezuela. These countries relied on short-term debt to manage immediate cash flow issues, which ultimately exacerbated their economic instability. The risk of this is shorter-term debt needs to be refinanced more frequently which causes the size of government bond auctions to increase.

Graph from Apollo Academy. That’s a big increase, especially for shorter-term bonds.

DKI Takeaway: Each auction tells its own story and Treasury traders measure each auction’s success using key metrics like the bid-to-cover ratio and the auction tail. The bid-to-cover ratio compares the number of bids to the quantity accepted, indicating demand. The auction tail measures the difference between the highest accepted yield and the expected yield, with a large positive tail signaling weaker-than-expected demand. More detail on this subject can be found in an insightful thread by James Lavish @JamesLavish (https://twitter.com/jameslavish/status/1577334009092198400). Looking ahead, U.S. Treasury issuance is expected to reach record levels later this year. Some argue that such trillions of dollars of issuance could be a sign encouraging a cut in the Fed Funds Rate (FFR) by September. However, it's crucial to remember that bond yields are determined by the market, not directly by the FFR. In addition, the market for US Treasuries is deep, but everything has demand limits depending on price.

- Tax Receipts vs Government Spending:

As part of the 5 Things a couple of weeks ago, we talked about how Fed Chairman, Powell, called out Congressional overspending as unsustainable. The Fed has been trying to slow the economy and reduce inflation through rate hikes. Congress and the White House (aided by the Treasury Department) have been engaging in trillions of dollars of inflation-causing stimulus spending while many in Congress insist that Powell lower the fed funds rate to make the borrowing costs of all that extra debt less expensive. When I pointed out that Powell is correct that Congress is both causing inflation and incurring debts that are unpayable, I got some pushback on Twitter/X. Several thought the real problem was tax cuts that were denying the government the “revenue” it needed to pursue all spending plans regardless of value. Let’s take a look at whether the data supports that.

That’s a big increase in tax collections with a bigger increase in spending.

DKI Takeaway: The growth in the size of government has become exponential. To me, it seems clear that with tax collections of $5 trillion, the government has the means and opportunity to do plenty. As quickly as tax collections have grown, government spending has grown even faster. I understand the concept that taxing the “rich” can be a way to pay for benefits for the poor. However, as the government spends more, that additional stimulus, which is focused on consumption, not investment, is creating inflation. Inflation works fine for the wealthy who can take on fiat-denominated debt to buy hard assets. It’s been terrible for less affluent people who can only save in depreciating dollars and who have been facing increasing budgetary issues due to rising rent along with higher food and fuel prices. While I understand both sides of this argument, I continue to believe we’d all (rich and poor) be better off with a government that is a more modest part of the economy.

Information contained in this report, and in each of its reports, is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied. DKI makes no representation as to the completeness, timeliness, accuracy or soundness of the information and opinions contained therein or regarding any results that may be obtained from their use. The information and opinions contained in this report and in each of our reports and all other DKI Services shall not obligate DKI to provide updated or similar information in the future, except to the extent it is required by law to do so.

The information we provide in this and in each of our reports, is publicly available. This report and each of our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion in this and in each of our reports are precisely that. Our opinions are subject to change, which DKI may not convey. DKI, affiliates of DKI or its principal or others associated with DKI may have, taken or sold, or may in the future take or sell positions in securities of companies about which we write, without disclosing any such transactions.

None of the information we provide or the opinions we express, including those in this report, or in any of our reports, are advice of any kind, including, without limitation, advice that investment in a company’s securities is prudent or suitable for any investor. In making any investment decision, each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable, based on this or any of its reports, or on any information or opinions DKI expresses or provides for any losses or damages of any kind or nature including, without limitation, costs, liabilities, trading losses, expenses (including, without limitation, attorneys’ fees), direct, indirect, punitive, incidental, special or consequential damages.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

date | ticker | name | Price Target | Upside/Downside | Recommendation | Firm |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.