A bond is an asset class meant for those looking for a relatively safer investment avenue. Usually, an investor adds bonds to his portfolio to mitigate any loss stemming from a decline in equities. As always, with less risk comes fewer returns. Therefore, returns from bonds most often trail the returns from risky bets such as equities.

It is an IOU obligation. Investors buying the bond lend money to the government, local bodies (municipal bonds) or companies in return for a promise to pay periodic interest payment and the principal when the term of the bond expires.

The bond market, which otherwise is called as debt or fixed income or credit market, is a market where bonds are bought and sold. With a lack of common exchange for bonds, bond trading usually happens over-the-counter, with the liquidity provided by dealers and other market participants.

The size of the bond market is supposed to be twice that of the stock market.

These fixed income securities, especially those issued by the government, have varied nomenclature depending on their tenure. If the tenure is one year or less, then they are called bills, which do not pay interest but are redeemable at a premium. The difference between the purchase price and the price paid at maturity would be the return on the investment.

Notes have maturity ranging between one year and 10 years. Those securities with a maturity period of more than 10 years are called as bonds.

See also: How The Markets Fared In July

In the case of bankruptcy of the issuer, bond holders can lay claim to the assets and cash flow of the issuer proportionate to their investment. The priority of the claims depend on the nature of the bond, ie, whether it is secured or unsecured (debentures) and if it is unsecured, then whether it is a senior or junior bond.

Before understanding the bond market dynamics, it is pertinent that one should have a good understanding of some key terms such as bond prices, face value, coupon rate or interest rate, maturity and yield to maturity.

Here's an example of an instrument:

Costco Wholesale Corporation COST recently announced a multiple debt offering of senior unsecured notes with different maturities.

The debt offering consisted of a tranche of notes worth $1 billion (principal amount) with coupon rate 2.15 percent and maturity date of May 18, 2021.

-

Price to Public: 99.825 percent Years to Maturity: four years Coupon Rate: (annual interest paid on the bond, expressed as a percent of the face value). The coupon rate on this note is 2.15 percent. Yield to Maturity: 2.196 percent

Mathematically, yield to maturity = (Coupon rate + ((Face Value- Price)/Years to Maturity))/((Face Value + Price)/2)

If the note is priced at par value (face value), the YTM equals the coupon rate.

How Are Bonds Priced?

The Costco offering constitutes primary offering of notes. Just like stocks, there is a secondary market for bonds, where already issued bonds are bought and sold. Bond pricing in the secondary market is dictated by the classical economic theory of demand and supply. Additionally, years to maturity and credit rating of the bonds also determine their prices. Bonds can trade at par value (with face value), at a discount or at a premium depending on the factors that influence the pricing.

The Confounding Inverse Relation

Bond price also depends on the prevailing interest rates. Let us assume Bond A is priced at $1,000 and the coupon rate on the bond is 10 percent. Bond prices are benchmarked against the U.S. treasury security taken as proxy for the prevailing interest rate.

If the interest rate (rate on the short-term treasury security) is also 10 percent. A bond investor may not have much to choose between both, although he may be swayed slightly by the safety offered by the government security. Both would fetch a yearly return of $100.

However, if the economic fundamental deteriorate, causing interest rates to drop, to say 8 percent; the government security will fetch $80, while the bond would continue to return $100, making it a better investment option. With the bond bringing in more returns for the same investment dollars, demand for the bond will increase, sending its price higher.

The bond will now trade at a premium to its face value and the price of the bond rises until its return equals to the diminished return from the government security.

If the reverse happens, ie if interest rate rises to 11 percent, the bond price would fall until the returns equal to the prevailing interest rate or the returns from the government security (which is now 110). No investor worth his salt would be willing to cough up $1,000 to earn $100 on a bond, when an investment of the same magnitude in a government security can fetch you $110.

If the bond has to be a viable investment option, its price has to fall to push up its yield to equal the interest rate.

Thus bond prices and its yield are inversely proportional to interest rate.

On An Extended Bull Run

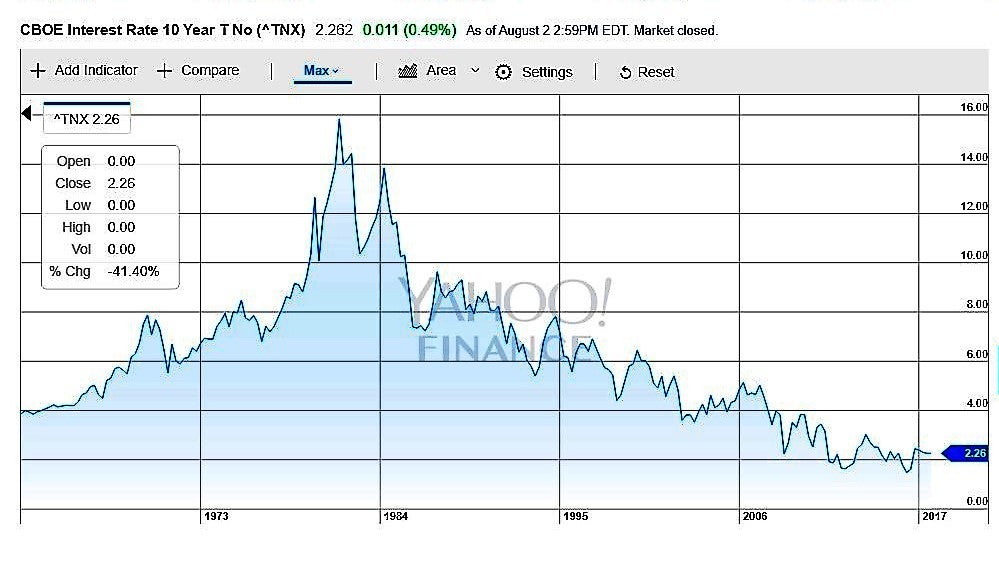

Currently, the bond market is on a bull run, as the yield on the benchmark 10-year is depressed. The yield on the 10-year Treasury bond was at 2.26 percent Wednesday, down from 5.5 percent before the Great Recession of 2007–08. The yield has been on a decline since peaking at 15.84 percent in July 1981.

Source: Yahoo Finance

Source: Yahoo Finance

Lower interest rates, though good for borrowers, deprive income for those invested in fixed income securities. On the contrary, higher interest rates would be bad for existing bond holders, as prices of bonds would drop, causing substantial losses.

"Still, bond market experts point to a simple, undisputed fact: Yields on Treasuries and other highly rated bonds are so low they cannot go much lower," according to an article carried by Knowledge Wharton.

"Historically, they have been much higher, and the law of averages says they should rise again."

Bubble Burst?

Recently, former Fed Chairman Alan Greenspan, who is credited with the coining of the term irrational exuberance, mused about a probable bond market bubble burst. Along with the predicament, Greenspan also sees the stock market being dragged lower.

_______

Image Credit: By Dan Smith - Own work, CC BY-SA 2.5, via Wikimedia Commons

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.