The Viridian Cannabis Deal Tracker is an information service that monitors capital raise and M&A activity in the legal cannabis industry. Each week the Tracker analyzes/aggregates all closed deals and allocates each transaction to one of twelve key industry sectors in which the deal occurred (from Cultivation to Brands), the region in which the deal occurred (country or U.S. state), the status of the company announcing the transaction (public vs. private) and the type of deal structure (equity vs. debt).

The Viridian Cannabis Deal Tracker provides the deal data/terms/valuations/structures and market intelligence that cannabis companies, investors, and acquirers utilize to make informed decisions regarding capital and M&A strategy. Since its inception in 2015, the Viridian Cannabis Deal Tracker has tracked and analyzed more than 2,500 capital raises and 1,000 M&A transactions totaling over $45 billion in aggregate value. Find it exclusively on Benzinga Cannabis every week!

INVESTMENT AND M&A ACTIVITY IN THE CANNABIS INDUSTRY

8/3/2020 - 8/7/2020

CAPITAL RAISES

Transactional Activity: Week 32 ended August 7, 2020, saw a 58% lower dollar volume but over 2 ½ times as many transactions vs. the prior week of this year and a sharply lower dollar volume and number of transactions vs the prior-year period. We recorded 8 capital raise transactions totaling $20.2 million, vs 10 transactions totaling $281.4 million during the same week in 2019. The average tranche size was $2.5 million this week, vs. $ 28.1 million in the prior-year period. Last year’s totals were skewed by the $143 million Sundial Growers IPO.

Largest Cap Raise: On August 6, FSD Pharma Inc. (HUGE : CSE, HUGE : OTC), which is focused on developing FDA-approved synthetic compounds targeting the endocannabinoid system, closed a $10 million registered direct offering of 2.76 million units at $3.62 per unit. Each unit consists of one common share and ½ of a 5-year warrant to purchase a share at an exercise price of $4.26. The $3.02 closing price for the shares on 8/6/20 is consistent with a valuation of the warrants using the Black Scholes option pricing formula and a 45% volatility. Although this is generally higher than the volatility we use to value warrant packages in the cannabis space, it is justifiable given the pre-revenue nature of FSD’s business. FSD trades at approximately 1.1 times market to book, a considerable discount from its peers. Of the 23 Biotech/Pharma companies we track with market capitalizations of between $25 million and $200 million,13 are pre-revenue companies, and they trade at a median valuation of approximately 4 times book. Some justification is found for FSD’s discount by looking at the company’s balance sheet. Approximately 50% of FSD’s assets of $52 million as of 6/30/20 were either cash ($14M) or assets held for sale ($12M), with the bulk of the remainder being intangibles ($21M). Neither cash nor assets held for sale are likely to be accorded a premium valuation. Assets held for sale arose from the company’s March 2020 decision to exit the medical cannabis business and liquidate its Cobourg facility. FSD’s stock has performed relatively poorly, declining 25% in the 3rd quarter to-date compared to an increase of 29% for our 28 stock index.

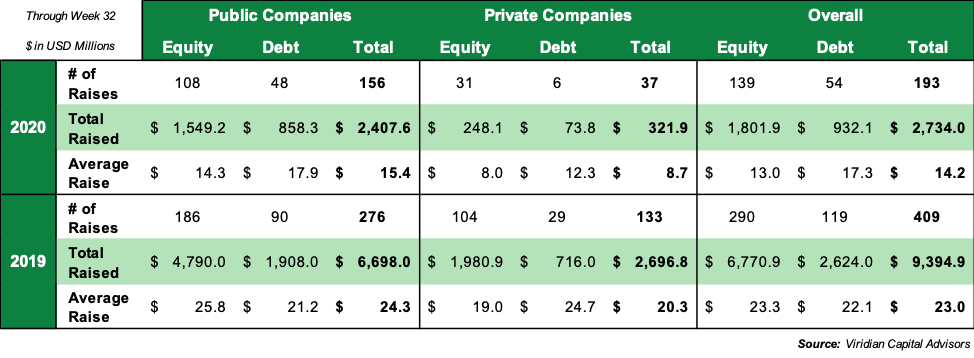

Public vs. Private Cap Raises: All 8 of this week's capital raises were closed by public companies. So far in 2020, public companies have accounted for 81% of all capital raises, vs. 67% for the same period in 2019. In 2020, public companies have accounted for 88% of total dollars raised, vs. 71% for the same period in 2019. Cannabis stock prices continue to perform strongly with our index of 28 cannabis stocks up approximately 11% in the most recent week. Viridian Deal Tracker data shows a clear relationship between cannabis stock prices and both capital raise and M&A activity. The capital markets are gaining confidence in the cannabis industry based on its demonstrated resilience in the face of a weak economy and on renewed hopes for positive legislative developments following the upcoming national election.

Public Company Listings: Of the 8 public company capital raises, all are listed in Canada (5 on the CSE and 3 on the TSX) and 7 of the 8 also trade In the U.S. (6 on the OTC and 1 on the Nasdaq)

Equity vs. Debt Cap Raises: Equity-based capital raises accounted for 7 of the 8 transactions and 75.7% of the proceeds raised. This week’s FSD Pharma Inc. $10 million equity raise represented nearly 50% of the financings for the week.

Largest Debt Raise: The largest debt raise of the week was the August 5, 2020, US$4.9 million issue of 8% senior secured convertible debentures with warrants by Canada House Wellness Group Inc. (CHV : CSE, SARF : OTC), an integrated medical cannabis company which provides patient-specific cannabinoid therapy products and services through its clinics and licensed producer. The issue was placed with a single strategic investor, Archerwill Investments Inc. which will control approximately 27.5% of the company on a fully converted basis. The debentures have a maturity of 5 years and a conversion price of C$0.05 per share, representing a 25% premium to the company’s stock price on the closing date. Archerwill also received 130 million 4-year warrants with a strike price of C$0.06 per share (a 50% premium). The conversion premium and warrant exercise premium are both higher than recent norms reducing the cost of what would otherwise be a very generous package given its combined coverage of 220%. We calculate an effective cost of 14.85% for the issue, lower than we would expect were it not for the placement with a single strategic investor.

Cap Raises by Sector: The 8 capital raises this week were spread across 4 different industry sectors with three in Biotech/Pharma, two in Cultivation & Retail, one in Agriculture Technology, and one in Infused Products & Extracts. Biotech/Pharma equity capital raises are accelerating with 19 issues for $96.3 million in the first half of 2020 compared to only 12 issues for $78.5 million in the same period of 2019 and 23 issues YTD, compared to 21 for the full year of 2019.

MERGERS & ACQUISITIONS

Transactional Activity: Week 32 saw 4 M&A transactions, vs 0 in the prior-year period. Though M&A activity is still far below the levels seen in 2019, we continue to see a pickup in activity. This is likely driven by the continued increases in stock prices of cannabis companies, giving them a more valuable transaction currency.

Largest M&A Transaction: On August 4, MYM Nutraceuticals Inc. CSEOTC closed an $11.65 million acquisition of Highland Grow, a licensed cultivator/processor subsidiary of Biome Grow Inc. CSEOTC. The transaction was significant for MYM: total consideration including Class A special shares, amounts to approximately 49% of total MYM shares. The Highland Grow cultivation and distribution facility in Nova Scotia will expand MYM’s cannabis footprint, allowing it to immediately supply the Canadian market with premium craft cannabis.

Public vs. Private: All of this week’s acquisitions were made by public companies as has been the case in 94% of M&A transactions closed in 2020. Public companies, particularly with the recovery in stock prices and fundraising ability, have been the dominant acquirers in the cannabis industry. All of the acquired companies were private. Private companies remain the dominant targets for acquirers, except for the growing number of sale-leaseback transactions, many of which have been done by large public MSOs.

M&A by Sector: Buyers came from 3 different sectors: Cultivation & Retail, Investment/M&A, and Infused Products & Extracts.

WEEKLY SUMMARY

EQUITY RAISES

DEBT RAISES

MERGERS & ACQUISITIONS

YEAR-TO-DATE SUMMARY

CAPITAL RAISES

Capital Raises by Week

Capital Raises by Sector

MERGERS & ACQUISITIONS

M&A Activity by Week

M&A Activity by Sector

Photo by Javier Hasse.

The preceding article is from one of our external contributors. It does not represent the opinion of Benzinga and has not been edited.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Cannabis is evolving – don’t get left behind!

Curious about what’s next for the industry and how to leverage California’s unique market?

Join top executives, policymakers, and investors at the Benzinga Cannabis Market Spotlight in Anaheim, CA, at the House of Blues on November 12. Dive deep into the latest strategies, investment trends, and brand insights that are shaping the future of cannabis!

Get your tickets now to secure your spot and avoid last-minute price hikes.