The Viridian Cannabis Deal Tracker is an information service that monitors capital raise and M&A activity in the legal cannabis industry. Each week the Tracker analyzes/aggregates all closed deals and allocates each transaction to one of twelve key industry sectors in which the deal occurred (from Cultivation to Brands), the region in which the deal occurred (country or U.S. state), the status of the company announcing the transaction (public vs. private) and the type of deal structure (equity vs. debt).

The Viridian Cannabis Deal Tracker provides the deal data/terms/valuations/structures and market intelligence that cannabis companies, investors, and acquirers utilize to make informed decisions regarding capital and M&A strategy. Since its inception in 2015, the Viridian Cannabis Deal Tracker has tracked and analyzed more than 2,500 capital raises and 1,000 M&A transactions totaling over $45 billion in aggregate value. Find it exclusively on Benzinga Cannabis every week!

INVESTMENT AND M&A ACTIVITY IN THE CANNABIS INDUSTRY

9/28/2020 - 10/2/2020

CAPITAL RAISES

-

Transactional Activity: Week 40 ended October 2, 2020, saw a $71.8 million lower dollar volume with 2 fewer transactions vs. the prior week of this year and a 15.5% lower dollar volume with 3 fewer transactions vs the prior-year period. We tracked 5 capital raise transactions totaling $59.8 million, vs 8 transactions totaling $70.8 million during the same week in 2019. The average tranche size was $12.0 million this week, vs. $8.9 million in the prior-year period.

-

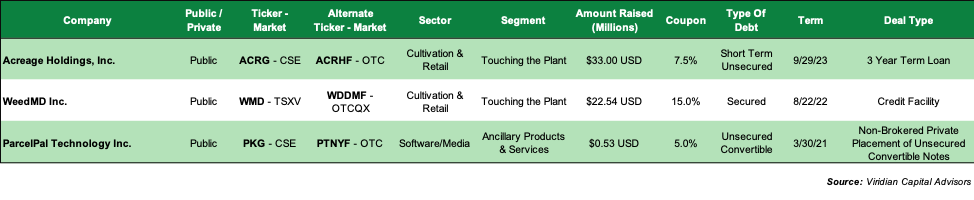

Largest Cap Raise: On September 29, 2020, Acreage Holdings, Inc. ACRG ACRGF raised $33 million in an unsecured 3-year term loan with a coupon of 7.5% from an institutional investor. No additional details were disclosed, however, we believe that some other loan feature is likely to have been involved because we find it difficult to believe that investors would have loaned money to Acreage on an unsecured basis at 7.5%. The Viridian Credit Tracker ranks Acreage #10 out of the 14 U.S. Cultivation & Retail sector companies with market caps over $100 million. The company ranks at the bottom in both profitability and liquidity and #9 on our leverage ranking. Acreage’s last debt raise in June was done at an effective cost of over 50% and, although recent news regarding the distribution of Canopy beverages is undoubtedly credit-positive for Acreage, it’s still quite a stretch to get to 7.5%. So, it seems likely that there are some convertibility/warrants, a significant OID, a large premium due at maturity, or some other investor-friendly features that were not disclosed in the press release.

-

Public vs. Private Cap Raises: 4 of this week’s 5 capital raises were closed by public companies. So far in 2020, public companies have accounted for 80% of all capital raises, vs. 66% for the same period in 2019. In 2020, public companies have accounted for 84% of total dollars raised, vs. 69% for the same period in 2019.

-

Public Company Listings: Of the 4 public company capital raises, all are listed in Canada on (3 on the CSE and 1 on the TSX), and all 3 also trade on other markets (3 on the OTC and 1 on the FSE).

-

Equity vs. Debt Cap Raises: Equity-based capital raises accounted for 2 of this week’s 6 capital raises and accounted for only 6% of the funds raised.

-

2nd Largest Capital Raise: On September 30, 2020, WeedMD WMD WDDMF, a Canadian company engaged in the production and distribution of both medical and adult-use cannabis, closed a C$30 million (US$22.54 million) 15% secured credit facility maturing in August 2022. Interest can be paid in cash or capitalized. The lender, an affiliate of the LiUNA Pension Fund of Central and Eastern Canada (“LPF”), is a related party, with more than 10% ownership of WeedMD’s outstanding shares after WeedMD’s purchase of Starseed Medicinal Inc. Deal terms were approved by a special committee of the company’s board and appear favorable to what might have been obtained from a non-affiliated lender. WeedMD ranks #11 out of the 63 Canadian Cultivation & Retail companies on our Credit Tracker with market caps of under US$100 million; its high relative size and reasonable liquidity partially mitigate its high market leverage and low profitability. Our constructive quantitative rating notwithstanding, we note that the company has missed its consensus EBITDA estimates for each of the last 4 quarters, has a significant decline in the most recent quarter’s sales and EBITDA as it moved away from wholesale sales, and had to obtain amendments to its credit agreement covenants in June.

-

Cap Raises by Sector: The 5 capital raises this week were spread across 2 different industry sectors with three in Software/Media, and two in Cultivation & Retail.

MERGERS & ACQUISITIONS

-

Transactional Activity: Week 40 saw 2 M&A transactions, down from 5 in the prior-year period. Although the number of M&A transactions completed year-to-date is down 77% vs the comparable period of 2019, we continue to expect increased activity in the remainder of the year.

-

Largest M&A Transaction: On October 1, Slang Worldwide SLNG )) SLGWF, a company focused on developing brands and hardware products that include Openvape, Firefly, Magic Buzz, Bakked, and Strain Hunters, closed its acquisition of Oregon based LBA Global Corporation (“LBA”) and its Lunchbox Alchemy (“Lunchbox”) brand portfolio which is one of the top-selling edibles brands in the state. The acquisition adds extraction, manufacturing, and distribution capabilities that Slang expects will add gross profits in what it considers a core market. The transaction consideration consisted of 23.9 million shares of Slang, valued at US$2.22 million on the transaction date.

-

Public vs. Private: Both of this week’s two acquisitions were made by public companies. Year-to-date, 92% of M&A transactions closed in 2020 have been made by public companies (up from 71% in 2019). Public companies, particularly with the recovery in stock prices and fundraising ability, have been the dominant acquirers in the cannabis industry. Private companies remain the dominant targets for acquirers.

-

M&A by Sector: Both of the buyers in this week’s two deals came from the Infused Products & Extracts sector. One target was from the Infused Products & Extracts sector and the other from the Software / Media sector.

WEEKLY SUMMARY

EQUITY RAISES

DEBT RAISES

MERGERS & ACQUISITIONS

YEAR-TO-DATE SUMMARY

CAPITAL RAISES

Capital Raises by Week

Capital Raises by Sector

MERGERS & ACQUISITIONS

M&A Activity by Week

M&A Activity by Sector

Photo by Javier Hasse.

The preceding article is from one of our external contributors. It does not represent the opinion of Benzinga and has not been edited.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Cannabis is evolving – don’t get left behind!

Curious about what’s next for the industry and how to leverage California’s unique market?

Join top executives, policymakers, and investors at the Benzinga Cannabis Market Spotlight in Anaheim, CA, at the House of Blues on November 12. Dive deep into the latest strategies, investment trends, and brand insights that are shaping the future of cannabis!

Get your tickets now to secure your spot and avoid last-minute price hikes.