Co-Authored by Michael Sassano and Callum Kellas

The cannabis illicit market existed in all countries long before the legal markets arrived late on the scene. They have the biggest global distribution networks, with direct-to-your-door service and choices. For legal producers, the illicit market is and will always be the largest competitor to the legal market.

The dynamics of cannabis consumption in the European Union and beyond portray an interplay between cultural acceptance, legal restriction, consumer appetite and geography.

The best data for the vast majority of European consumers today, sadly for now, comes from crime statistics, the European Monitoring Centre for Drugs and Drug Addiction (EMCDDA) and the Office for National Statistics, as well as anecdotal evidence.

The Consumer Profile Of Adult Consumers In The EU

When considering annual consumption, the rate surpasses 10% in five countries within the sample. The adult consumers in Spain and France are the two most notable for their contrasting barely existent legal access frameworks.

Examining the profile of monthly consumers closer, we see broadly about 30% of monthly consumers intake cannabis almost daily, and a further 30% use it weekly. In short, around 3% of the European population consumes cannabis at a volume comparable to a legal patient.

Czechia is a striking outlier, with frequent consumption considerably more prevalent than other EU countries given its comparatively permissive regulatory and social culture.

Evidently, the Portuguese have the least habitual use. While being the trailblazers in decriminalization, the most topical comparison would be in Germany, where this week Chancellor Olaf Scholz stated that their specific aim was to reduce use. No prizes for guessing how the German markets will react in the coming months with simplified medical access and soon an established source of legal supply in the rollout of social clubs.

The Sleeping Giants Of Legal Cannabis Consumption

When you look at the percentage of adults who consume cannabis every month, it’s the same three names that jump out at you in that big green block: Spain, France, and Italy emerging as significant markets for potential legal reform and access.

This consumption pattern underscores the deeply ingrained nature of cannabis within certain European cultures and the potential for legal markets to adapt and compete with the illicit trade.

Trends within EMCDDA-reported average illicit market prices per gram over the past 20 years in the EU illustrate that geographical circumstances and early deregulation are key drivers in price inflation.

-

Sweden, Greece, Malta, and island nations are penalized for geographical inaccessibility. Maltese prices dropped sharply upon decriminalisation

-

Netherlands locals access affordable, locally grown flower in coffee shops

-

Spain benefits from well-connected routes with Africa and Latin America

-

Portugal prices are reigned in by progressive early legislation

-

Germany medical access over the past 5 years has reversed a fast rate of inflation

In 2021, the average illicit market price in the EU — which stood at €10.45 before the inflation of the last two years — reflects the impact of supply chains and the potential for localized legal production to influence market dynamics.

Point Of Inflection

More recently, one has to rely on anecdotal straw-poll pricing that points to continued illicit market inflation.

With a small sample size and a wide range of products and quality, it’s difficult to conclude too precisely. However, we can draw the same general assertions as we did with official data:

-

The two markets are in direct competition with one another

-

The more developed and permissive the regulations, the lower the price

-

Often, the highest reported pricing comes from the illicit market

-

Comparison To Medical Pricing Trends

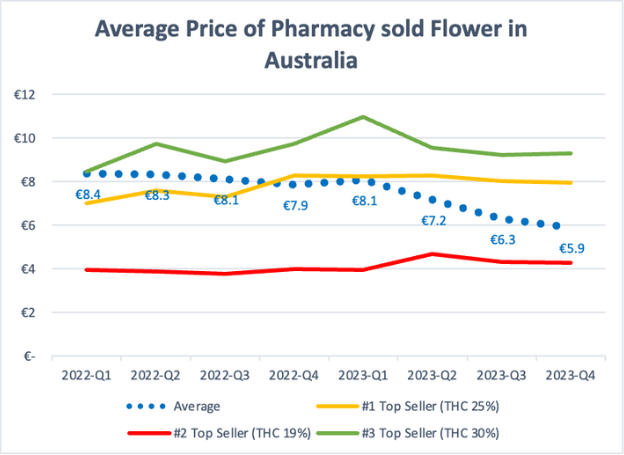

Australian prices derived from POS data up to 2023 illustrate the opposite effect in a significant downward price per gram. This was at a time when legacy GACP flower was still permissible but the emergence of compassionately priced patient access schemes has made a significant price impact since their launch in late 2022. The breadth of the market is shown by the top selling 3 brands, where evidently some consumers value premium products well above the global average.

A similar pricing trend occurred in the United Kingdom, where the average price of 65 strains listed for sale on 4/20 on MedBud UK was €8.5 per gram. Of course, significant clinical fees supplement the medication cost, but the downward trend is evident compared to those prices reported in MedBud just one year ago when the 44 flowers averaged €10.1.

One year ago, an economizing patient could acquire 20% THC at €8 per gram. Today this budget would stretch to one of dozens of flowers up to 25% THC, representing a meaningful step forward in value and quality for patients.

When we remove the 3 most extreme outliers in each case as above, a far stronger relationship between potency and price emerges, indicative of an increasingly mature and competitive market.

The New World Producer Revolution: Localization And Supply Chain Shift

Data on the volume of seizures of cannabis, compared to other regional countries, gives an insight to the supply chain of the illicit market. Given Spain’s proximity to Morocco, it’s especially striking in the cannabis resin (hash) category.

Whereas geography and culture previously governed market dynamics, the producers of tomorrow will be determined by deregulation.

As with wine production, heritage producers like Morocco and Thailand will have their place alongside deregulated, entrepreneurial nations in the cannabis world of tomorrow.

Tip Of The Iceberg

The contrast between the number of illicit consumers and those procuring cannabis legally through medical channels is stark. Take the U.K., for example, where an average appetite for habitual cannabis consumption accompanies a meager degree of medical access: Monthly illicit consumers outnumber legal medical patients by approximately 80 times, highlighting the significant disparity in accessibility brought about by the existing regulatory model.

There are myriad reasons why some of the most educated and passionate cannabis consumers get what they need illegally. While standardization, efficacy and quality are paramount, our job is to understand, compete and even emulate some facets of illegal trade. Any cannabis producer is missing the point if they don’t define the value proposition that every consumer weighs up. Whether it’s cannabis, beer or pastel de nata, my high school business textbook tells me the fundamentals are price, quality, choice and convenience.

The medical price per gram is reaching an inflection point with the illicit market. While the added costs of accessing in-clinic settings with healthcare professionals privately is the difference between today’s legal producers gaining a transformative competitive advantage over the illicit market.The timing of this shift will depend on this generation’s political agenda shifting further from reefer madness mindset to demonstrably more effective strategies for tackling the illicit trade.

Prices will continue to converge as the legal supply chain catches up with its infrastructure. As access opens up, the boxes ticked in each consumer's head begin to accumulate:

|

Price |

QUALITY |

CHOICE |

CONVENIENCE |

|

|

EUROPE |

Pending |

Pending |

N |

N |

|

AUSTRALIA |

Y |

Pending |

Pending |

Y |

|

CANADA |

Pending |

Y |

Y |

Y |

|

USA |

Pending |

Y |

Y |

Y |

2024 will be etched in history for global medical cannabis as a small step for international consumer access through deregulation in Germany and the famous U.S. HHS/FDA 252-page report deeming cannabis safe and useful for “at least 15” indications.

Now, the door is open wider than ever for any other predominant cannabis-consuming nations to embrace the data and growth in investment and infrastructure for developing countries that will unlock markets even larger than in the U.S. The ones that can marry supply capabilities with deregulation and genuine care for the consumer will be the big winners in the brave new world of cannabis.

This article is from an external unpaid contributor. It does not represent Benzinga’s reporting and has not been edited for content or accuracy.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Cannabis is evolving—don’t get left behind!

Curious about what’s next for the industry and how to stay ahead in today’s competitive market?

Join top executives, investors, and industry leaders at the Benzinga Cannabis Capital Conference in Chicago on June 9-10. Dive deep into market-shaping strategies, investment trends, and brand-building insights that will define the future of cannabis.

Secure your spot now before prices go up—this is where the biggest deals and connections happen!