Between April 1995 and August 1998, the yen (JPY) fell by nearly 50% versus the U.S. dollar (USD). It then reversed course, gradually at first, and then suddenly. In a 48-hour period between October 6- 8 in 1998, JPY gained 17% versus USD.

The proximate cause of JPYUSD’s spike higher was the unwinding of the U.S. hedge fund Long-Term Capital Management (LTCM). LTCM had been borrowing yen at near-zero rates in order to fund leveraged positions in the higher yielding fixed-income instruments of other currencies. When a consortium of banks unwound the failed hedge fund’s positions, the yen soared (Figure 1).

Figure 1: The yen soared in 1998 with the LTCM meltdown: could it happen again?

From early 2021 to October this year, JPY lost nearly one-third of its value versus USD, but in the past month the yen has been rebounding. Could a 1998-style upward move happen in the yen again? While we are not aware of any LTCM-like foreign borrowing in the yen this time, there are other risk factors that could lead to a sudden rise in the yen. Should such a rise occur, it could have profound implications for investors in global bond markets as well as for foreign and domestic investors in Japanese equities.

Scan the above QR code for more expert analysis of market events and trends driving opportunities today!

Perhaps the biggest risk factor is the Bank of Japan’s (BOJ) ongoing yield-curve control, which has capped 10Y Japanese Government Bond (JGB) yields at 0.25%. The BOJ designed the policy to help return inflation towards 2% -- a level that the central bank has not consistently achieved absent hikes in Japan’s value-added tax (VAT) since the early 1990s. Now, however, the policy seems to be working, perhaps too well. In October 2022, headline inflation hit 3.7%, and core inflation, excluding food and energy, was 2.5% , raising the risks that the BOJ might opt to end its yield-curve control policy (Figure 2). Moreover, the recent rise in inflation has happened in the context of an extraordinarily strong employment market with 1.34 job openings per applicant. Finally, the BOJ has surely witnessed the rapidity with which inflation surged in the U.S. and in Europe and might be tempted to end yield-curve control sooner rather than later to help prevent a surge in inflation.

Figure 2: Japan’s inflation has risen above target and far above the 0.25% cap on 10Y JGB yields

Should the BOJ opt to end the 0.25% cap on 10Y JGBs, the decision could ricochet through the global bond market. Part of the reason why the yen has been so weak is that with domestic yields capped, Japanese investors have often sought better returns on fixed-income instruments abroad. As such, depressed yields on Japanese government bonds may have prevented yields on foreign bonds from rising further than they might have otherwise (Figure 3). Additionally, the BOJ’s yield-curve control has helped to expand its balance sheet to be more than four times that of the U.S. Federal Reserve relative to their respective GDPs. The much more rapid expansion in the BOJ’s balance sheet is likely a factor in the yen’s weakness over the course of the past few years, and any end to the BOJ’s yield curve-control policy could be a serious boost for the Japanese currency (Figure 4).

Figure 3: The 0.25% cap on JGB yields may be preventing a further rise in yields elsewhere

Figure 4: The BOJ’s QE program has been 2x that of the ECB and 4x that of the Fed

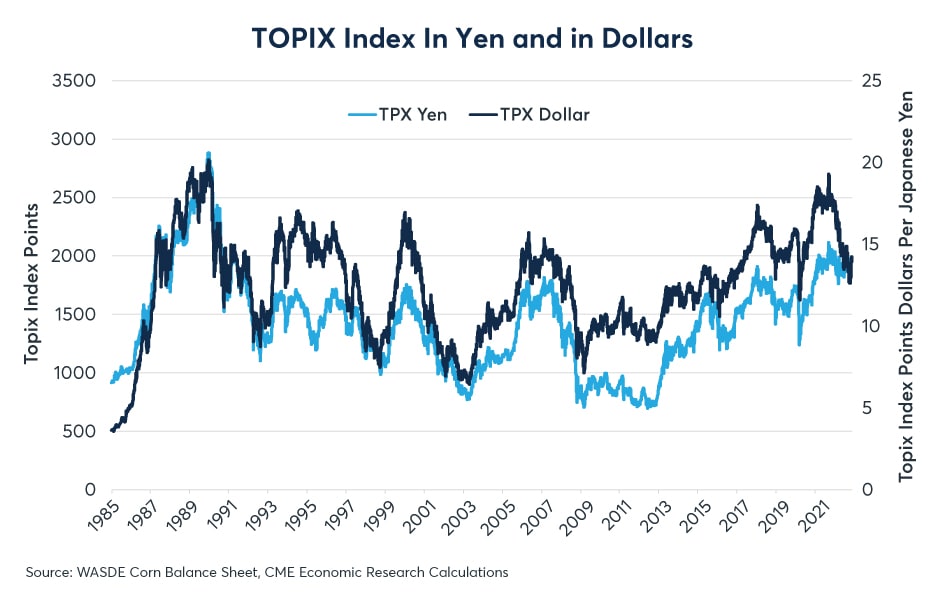

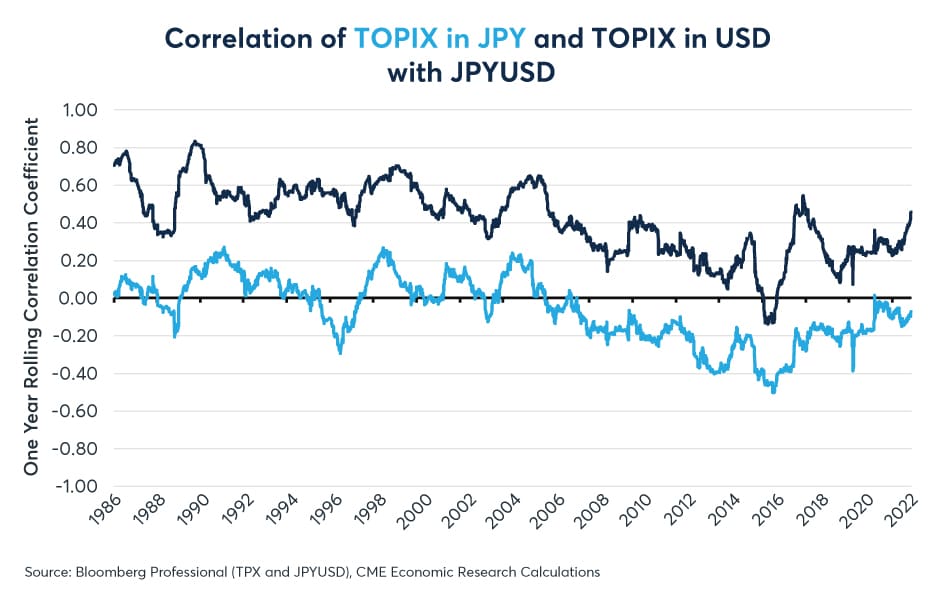

A potential end to yield-curve control has implications for equity investors as well, especially in the Japanese equity market. For domestic investors, who view their equity investments in yen terms, a sudden rise in the yen could be negative for equity returns. Over the past decade, TOPIX, or the Tokyo Stock Price Index, has generally had a negative correlation with JPYUSD, meaning that Japanese stocks tend to fall on days when the currency rose and vice versa. If the Japanese yen were to rise on the news of an end to yield-curve control, it could send Japanese stocks lower, at least when seen from a yen-perspective. By contrast, a sudden rise in the yen versus the dollar could boost returns to U.S. dollar investors who do not hedge their currency exposure. TOPIX seen from a USD perspective correlates positively over time with yen movements (Figures 5 and 6).

Figure 5: TOPIX hedged into dollars has underperformed as the yen has weakened

Figure 6: A sharp rise in the yen would likely lead to an outperformance of TOPIX hedged into USD

Featured image credit: Shutterstock

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.