The oil industry just got another major tailwind…

Two weeks ago, Energy Secretary Jennifer Granholm said the U.S. aims to start purchasing oil from domestic producers later this year.

It’s not a huge surprise. Just last week, I wrote about our country’s need to refill the Strategic Petroleum Reserve (SPR)—the U.S.’s emergency oil supply—which is nearly half empty.

These future purchases will create a floor under oil prices… and add another tailwind for oil stocks over the coming months.

Today, I’ll share several opportunities to profit from the energy sector’s improving outlook. But first, let’s take a closer look at why oil prices are set to keep rising…

The Bullish Picture For Oil

You’ve probably heard a lot about the massive growth in green energy in recent years.

The trend makes sense. Renewable energy sources like wind and solar will play an important role in the fight against climate change.

But anyone who thinks green energy will kill the oil & gas industry is crazy.

The simple fact is that the world still relies on fossil fuels for most of its energy needs. Oil and gas account for about 2/3 of the total U.S. energy consumption and about 4/5 of global energy demand.

Based on the most recent proposals, governments worldwide could eventually commit to hitting net-zero emissions by 2050. Even in this arguably “best case scenario” for green energy proponents, the plan still assumes that fossil fuels will account for 1/5 of global energy production. And even then, fossil fuels will still be used for several products and applications—from plastics to facilities using carbon-capture technologies.

In fact, the green energy push actually increases the value of existing oil reserves, as energy companies are becoming hesitant to explore and develop new oil fields.

Put simply, less oilfield development means less future oil production. And this dwindling supply situation improves the long-term outlook for oil prices. It’s Economics 101.

And, as I mentioned above, our need to refill the Strategic Petroleum Reserve (SPR) creates a major near-term boost for oil prices… and oil producers. The purchases will help put a floor under oil prices, which are already showing signs of strength. After dipping sharply last month, the price of oil quickly recovered and is now trading back near its 2023 highs… despite the widespread fears of a looming recession.

Put simply, the oil industry isn’t about to disappear… It’s set to flourish in the coming years.

And this translates into a huge opportunity for investors.

Below, I’ve highlighted three ways for investors to capitalize on the sector’s resilience…

1. Occidental Petroleum OXY

It’s almost impossible to go wrong following Warren Buffett’s investments…

And when it comes to energy, the Oracle of Omaha has an obvious favorite: Occidental Petroleum.

At the end of 2022, Buffett’s Berkshire Hathaway was the largest owner of eight mega-companies—American Express, Bank of America, Chevron, Coca-Cola, HP Inc., Moody’s, Paramount Global, and Occidental Petroleum.

It’s worth noting that OXY is the only energy company on that list.

Last summer, Buffett got the Federal Energy Regulatory Commission’s (FERC) permission to buy up to half of Occidental’s stock. Today, he’s sitting on more than 221 million shares—or 23.5% of the company.

The reason Buffett loves OXY is simple: The company has massive reserves in the Permian Basin—the largest oilfield in the U.S. Back in 2019, OXY outbid Chevron to buy independent producer Anadarko… thereby expanding OXY’s footprint in the Permian—bringing its stake to a sector-leading 2.8 million acres.

Buffett has been scooping up shares ever since.

In fact, Occidental is now the largest player in the Delaware Basin (part of the larger Permian)… and it has 3.8 billion barrels of oil equivalents in reserves.

Plus, OXY is one of the lowest-cost producers in the Permian… which makes it a profit machine as long as oil prices are above $40. And the company has no problem sharing its profits with shareholders. In February, OXY hiked its dividend by a whopping 38%.

2. Pioneer Natural Resources PXD

Pioneer is one of the biggest players in the Permian… and the largest player in the Permian’s best field, the Midland Basin.

The Midland Basin is shallower than the nearby Delaware Basin and holds higher-grade crude. That means more successful drilling… and higher-quality output.

Operating in such a well-researched, highly-developed oil region is also less costly since much of the infrastructure is already in place. And lower production costs mean higher profits… especially as energy prices rise.

In short, Pioneer’s assets are the best of the best—which translates to higher margins and growing profits.

And thanks to its incredible assets, Pioneer is a prime acquisition target as Big Oil launches a landgrab in the oil patch. But I don’t think PXD shareholders will need a buyout in order to score a profit. PXD’s flexible dividend policy is currently generating a 12%-plus annual yield—one of the highest in the entire stock market. And the longer PXD stays independent, the higher the ultimate reward for its shareholders—in terms of dividend payouts and share-price appreciation.

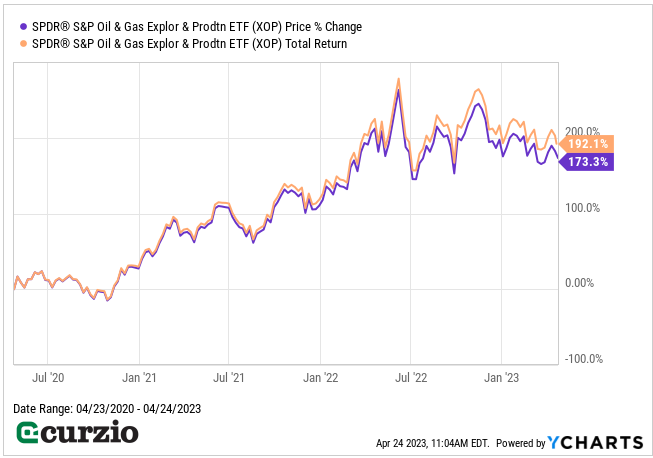

3. SPDR S&P Oil and Gas Exploration & Production ETF XOP

If you’d rather own a basket of leading oil companies, consider buying an exchange-traded fund (ETF)—like the iShares S&P Oil and Gas Exploration & Production.

This ETF gives investors exposure to the exploration and production segment of the market.

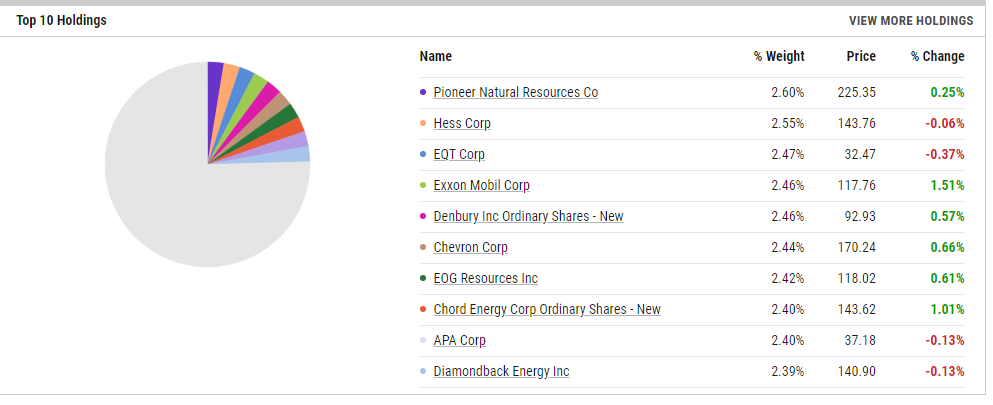

What makes this ETF different from the competition is its equal-weight focus.

In other words, it starts with the same-sized stake in each of its holdings… Like with any portfolio, the stronger the stock, the more of it you end up owning (until the next rebalancing). As of today, the ETF owns a larger position in PXD than it does in ExxonMobil (XOM) or Chevron (CVX), as you can see below.

Thanks to how it’s constructed, XOP is a better choice if your portfolio already has a lot of exposure to Big Oil… but is underweighted in smaller-cap oil companies (the cheapest group of the sector). Plus, you don’t have to research individual stocks.

Altogether, XOP has about 75% invested in exploration & production… 7% in integrated oil & gas… and 18% in refining & marketing.

In short, this ETF gives you instant exposure to companies big and small across the entire energy sector.

And because the ETF is smaller-cap focused, the stocks there are still very cheap… trading, on average, at less than seven times (7x) forecasted earnings (vs. 10.6x for PXD or 11.5x for OXY).

The bottom line: Demand for oil & gas isn’t about to wane any time soon, so if you don’t have energy exposure, now’s the time to get it…

Each of the picks above are great choices to play the improving outlook for the oil sector.

This content is for informational purposes only and is not intended to be investing advice.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.