Technological innovation has a habit of kick-starting disruptive movements across the global economy. And one of the reasons why we believe that decentralized finance, or DeFi, has such vast disruptive potential is that it offers inclusion and innovation.

Participants in economies where the financial system promotes regulated inclusion are fortunate to have relatively easy access to capital markets, savings, borrowing, lending, and other financial functions. However, financial access is a relative luxury and not equal to all, especially in developing economies. Traditional finance, being tied to centralized entities and intermediaries, offer permissioned entryways to financial inclusion. The merger of finance and technology into fintech has opened doors to new participants by simplifying front-end applications. But fintech’s underlying infrastructure still relies on the existing centralized models and functions.

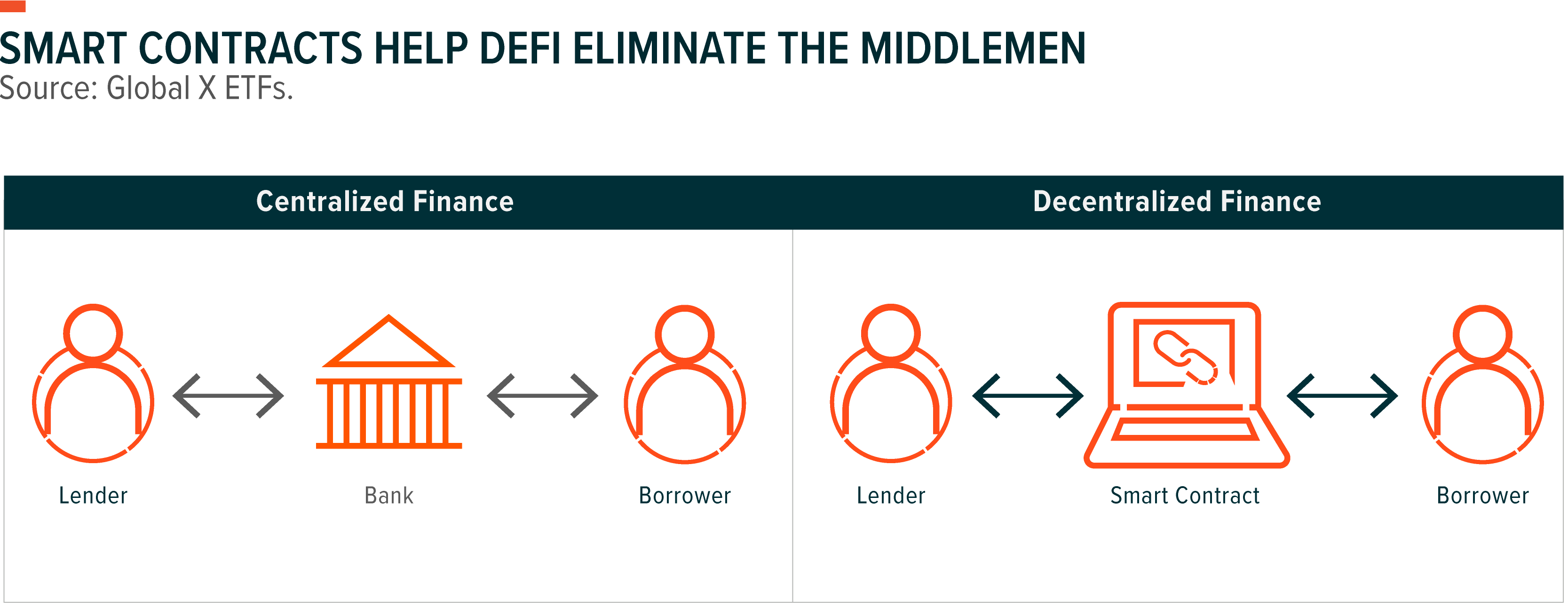

Enter DeFi, which is designed to solve those problems. With the rise of smart contract blockchains that host programmable applications, developers built DeFi decentralized applications (dapps) to provide a permissionless, global financial platform for users, by users. DeFi eliminates the need for intermediaries like financial institutions while transferring the power, cost savings, and operational effectiveness to users. It offers financial inclusion in a transparent, secure, and efficient ecosystem.

What to Know About DeFi and How It Works

- How was DeFi born? Smart contract innovation allowed developers to bring financial utility to dapps within smart contract blockchains.

- What is DeFi? DeFi is a decentralized, open-source, and user-owned financial umbrella. DeFi is an ecosystem of composable applications, free of traditional financial intermediaries, for money markets, loans, asset management, digital liquidity channels, and digital ownership.

- Who can participate in DeFi? DeFi is open to all. A non-Know Your Customer (KYC) cryptographically-derived public key allows users around the world to permissionlessly engage within DeFi dapps. The peer-to-peer nature of distributed ledger technology facilitates global value exchange.

- Where is DeFi today? DeFi user adoption continues to grow as its utility expands, helped by rising developer activity intent on innovating new ways to engage with financial infrastructure.

The Rise of DeFi

The Bitcoin network offered the first glimpse of what decentralized finance could be. Bitcoin allowed users to control and exchange value via a peer-to-peer network rather than by relying on financial intermediaries, which set the initial blueprint for a decentralized financial movement.

In 2013, at just 19, programmer Vitalik Buterin published the Ethereum whitepaper in which he introduced a novel, general-purpose, Turing-complete blockchain network that allows developers to build programable conditions and applications. In essence, Buterin created a programmable system that revolutionized how people think about, create, and deploy utility through blockchain technology. These programable conditions are known as smart contracts, as we discussed in Exploring the Disruptive Potential of Smart Contracts.

The ability to compose smart contract-powered dapps launched a utility and innovation movement. Applications that leveraged dapp technology with money programmability moved the needle for DeFi adoption. These applications were built to improve the financial system by creating a user-owned model that is censorship-resistant and open to all, and because of dapp composability traits, these applications could interact with each other. This created a world of possibilities and a new financial paradigm.

One of the first DeFi dapps was MakerDao, a collateralized debt position (CDP) project. Created around 2015, the project allowed users to over-collateralize their ether (ETH) positions in exchange for DAI, a stablecoin pegged to the U.S. dollar. This development was significant because it foreshadowed DeFi’s development. Other dapps such as Compound and Aave introduced decentralized money market platforms for lending and borrowing against cryptocurrencies, and Uniswap introduced the first successful decentralized asset exchange which relies on liquidity pools of token pairs to determine price rather than on market makers as in a traditional order book.

June 2020, popularly referred to as the start of “DeFi Summer”, was another inflection point for DeFi. Kickstarted by Compound, many projects launched community governance tokens, liquidity mining programs, and yield farming opportunities. The tokenization of projects incentivized and attracted users seeking yield in the form of borrower interest and/or token rewards for providing liquidity, triggering waves of new applications and users. Between June and August 2020, DeFi’s market share within the cryptocurrency landscape, as measured by the total cryptocurrency market cap, jumped from roughly 0.9% to 4.6%.1

DeFi Is a Novel Approach to a New Financial System

DeFi applications are where cryptocurrencies and smart contract programmability intersect. DeFi provides an application layer that replaces traditional human-controlled financial infrastructure with disintermediated, trustless, and permissionless proxies governed by immutable code.

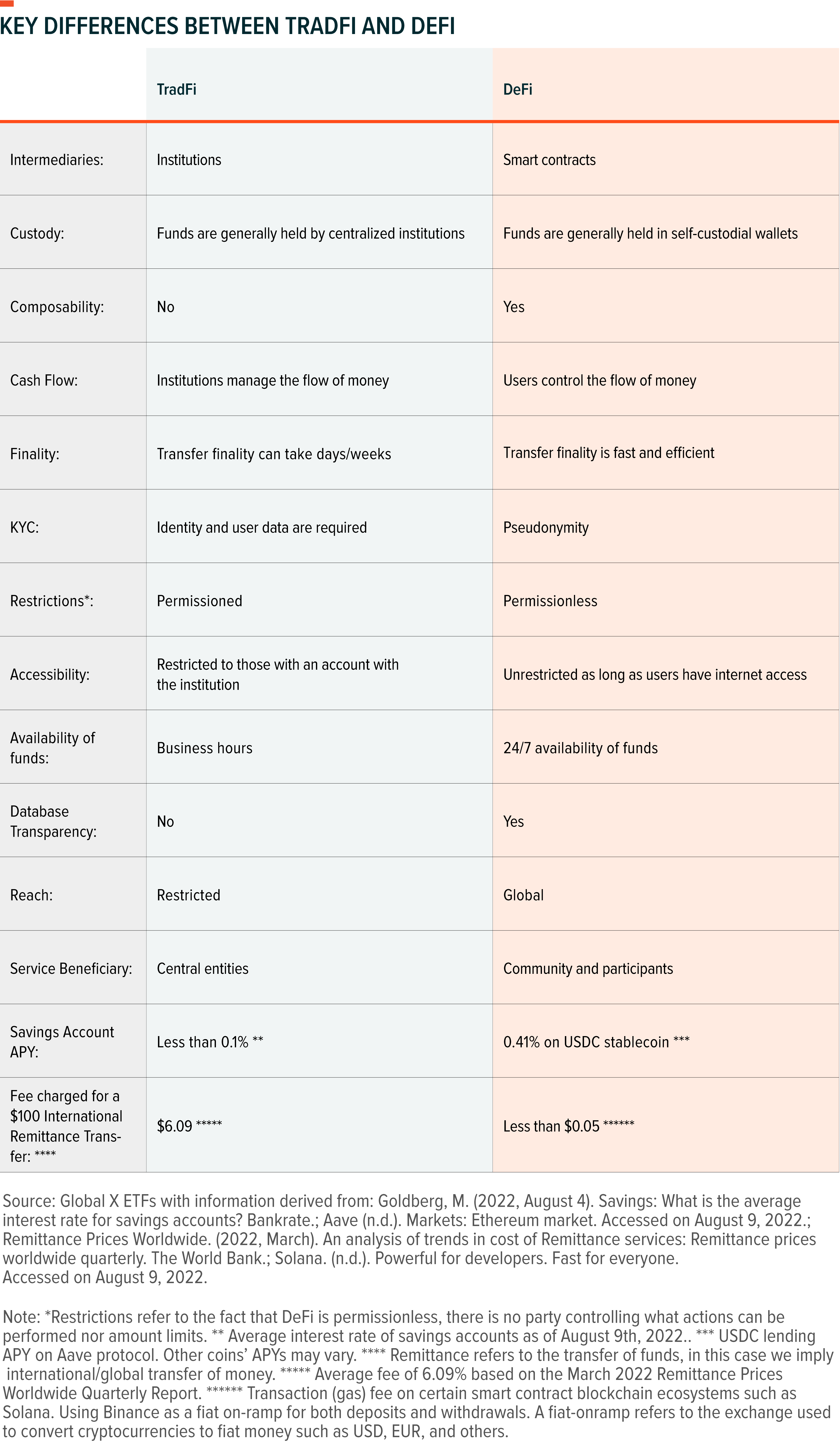

Smart contract dapp programmability powered by the security, scalability, and transparency of a blockchain as the base layer allows DeFi to exist. Ultimately, DeFi seeks to democratize traditional finance (TradFi), as the table below shows.

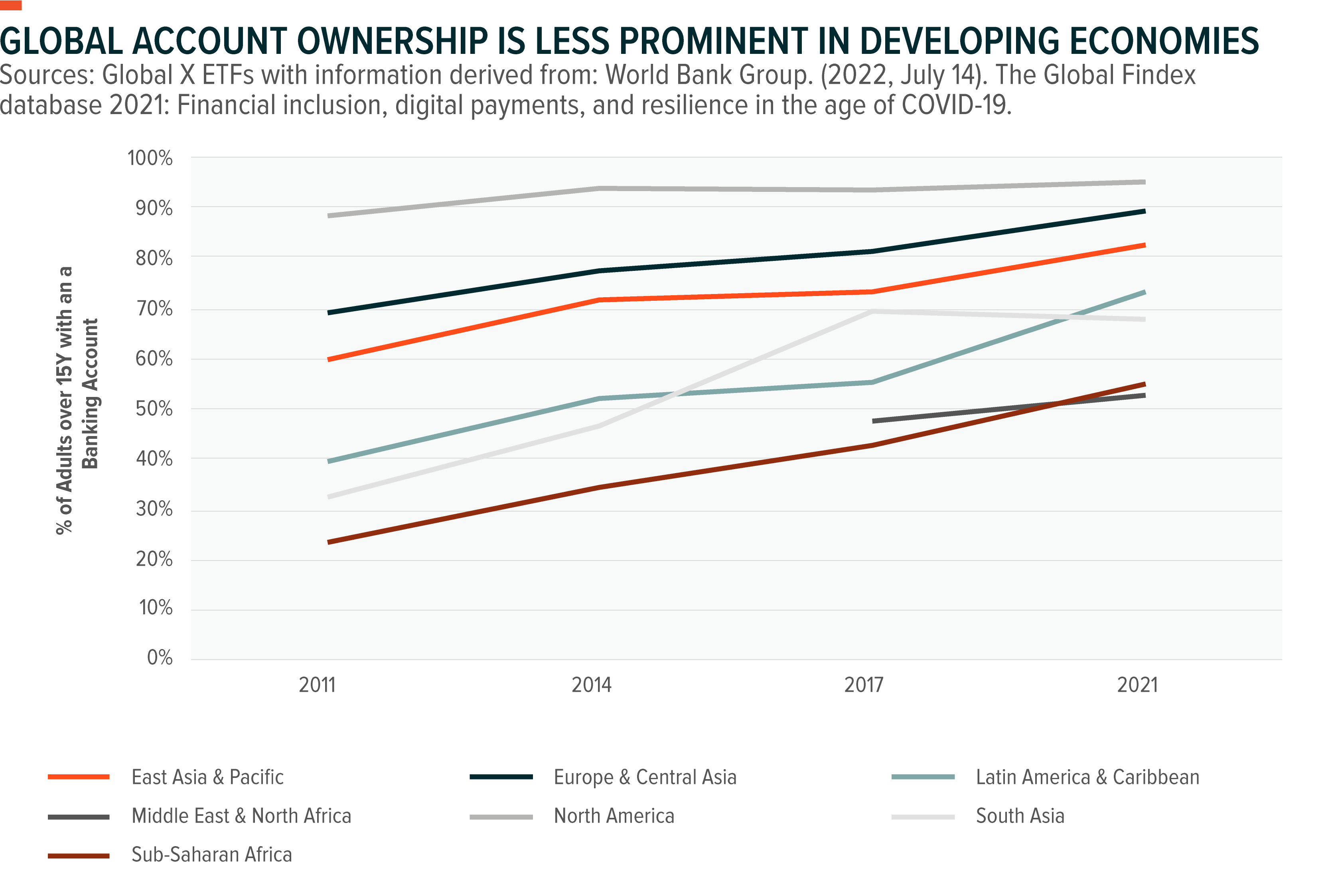

A fundamental measure of financial inclusion is financial account ownership. According to the 2021 Global Findex Database report, 76% of the world’s adult population have a bank account. Measured by age, 79% of adults 25 and older have an account, and 66% of adults between the ages of 15 and 24 have one.2 In our view, these numbers reveal an opportunity, as according to the World Bank, there are roughly 5.8 billion adults over the age of 15 in the world.3 If 24% of the total adult population is unbanked, that means roughly 1.4 billion adults are without access to the financial system and, likely, financial prosperity.

This shortfall in account ownership becomes more acute in underdeveloped and developing economies, where a lack of access to trusted financial institutions, proper technological infrastructures, proper documentation systems for Know Your Customer standards, and financial education is common. Financial services adoption continues to increase in these economies, but DeFi can expedite the onboarding of new participants exponentially due to its censorship-resistant, easy-to-access, and open-to-all financial platform. DeFi’s only requirements are an internet connection and some platform know-how.

DeFi’s reach expands beyond the unbanked and underbanked. We expect DeFi adoption to continue gaining momentum in strong economies as existing participants in the financial system begin to recognize its potential benefits. Among others, DeFi can offer higher lending yields because there is no centralized institution charging for the service. It can provide faster settlement periods on foreign remittances. Users can get instantaneous collateralized loans at variable rates depending on the funding provided without the need for KYC processes, and they can access greater liquidity for tokenized assets through DeFi rails.

According to Chainalysis’ Geography of Cryptocurrency report, DeFi as a percentage of total cryptocurrency activity ranged between 30% and 40% worldwide between July 2020 and June 2021. The most advanced DeFi activity occurred in developed economies. For instance, cryptocurrency transaction volume increased from $14.4 billion to $164 billion in North America; a 1,000% growth driven by DeFi’s growing popularity.4 In developing economies, basic DeFi utility in the form of peer-to-peer value exchange accounts for much of the activity. However, as these economies become digitally native, further DeFi applications are expected to gain adoption, allowing for greater economic prosperity. As cryptocurrencies gain adoption, DeFi can continue to scale.

Anyone can participate in DeFi, on either side of the trade, and reap the benefits of its user-owned nature. Users are incentivized to participate in this decentralized economy because projects can include governance tokens and incentivize liquidity providers through borrower yield without substantial intermediary fees. Additionally, project tokens can allow users to invest in their favorite platforms, participate in the platform’s governance decisions, and benefit from its value growth. In some cases, the fees generated by these dapps are paid out to certain liquidity providers, token holders, or project treasuries. Contrary to popular belief, certain DeFi dapps such as lending and exchange platforms can collect fees and generate revenues. For example, during the seven-day period from July 7th to July 14th, 2022, Uniswap generated an average of $1,245,301 per day in total borrower fees paid to liquidity providers.5 While the space grows, we expect fee allocation to improve as fundamentals and growth metrics shape up.

As with any novel technology, investors can participate in the value growth of the project but also in its volatility and downside risks. DeFi has unique risks that require proper risk management models. DeFi dapps are strings of code attached to a smart contract. If code is written incorrectly or its engineering is flawed, breaches and malfunctions are possible. DeFi users must be aware that the code works as intended, and they must take full responsibility for their actions.

It is important for users to understand the risks associated with on-chain liquidation transparency, on-chain arbitrage by other network participants, a potential malfunction of the dapp’s blockchain host, protocol hacks, associated oracle manipulations, flash loan exploits, maximal extractable value (MEV) farming, and overall market risk. When engaging with DeFi, it is important to do so in projects that have been built by a strong team and audited by a reputable firm. Hallmarks of credible projects include proper governance structures, strong liquidity sources, successful development track records, and healthy economic and token/fee distribution mechanisms.

Digital Wallets: Accessing and Interacting with DeFi

With blockchain technology, any interaction, meaning any type of data transfer, is considered a transaction that must be digitally signed. DeFi is no exception. Interactions with DeFi dapps are much like engaging in a peer-to-peer transaction, down to the transaction fee. In DeFi, the transaction fee is generally known as the gas fee, paid in the blockchain’s native asset. Such fee is paid in exchange for storing a transaction within a validated block.

Interactions generally happen between a user and a smart contract. In this case, the smart contract’s code serves as the intermediary that executes the function coded into the application users engage with.

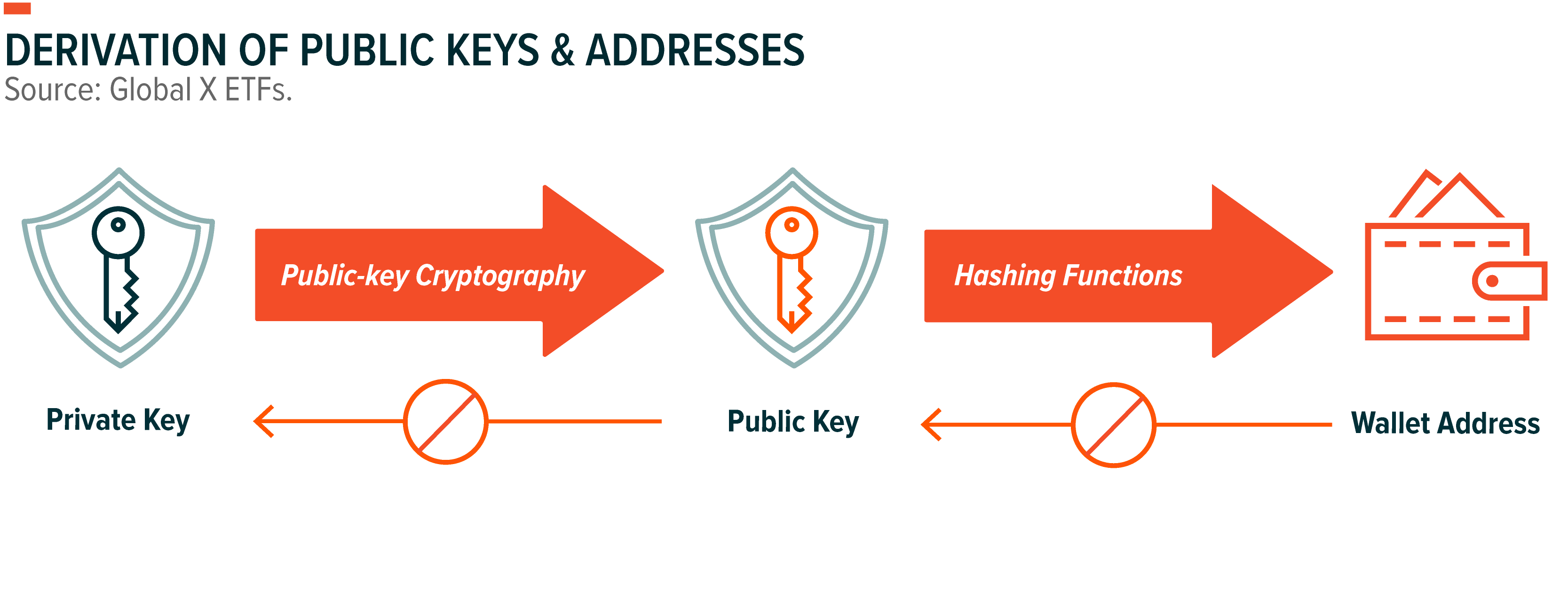

Asset balances reflect transactional activity under a user’s key and are stored within the blockchain’s historical distributed ledger. Users have individual keys that provide access to the rights of ownership of asset balances. Each user has a private key assigned by the blockchain and a cryptographically derived public key. The private key can be thought of as the account password and the public key the account number. Public keys are shareable, private keys are not.

Users connect their keys to DeFi dapps’ front-end applications. If a user engages in a transaction, they must have access to their private keys in order to sign for the approval of balance transfers and/or interactions with these smart contracts. Private keys are generally stored in crypto wallets linked to a public key. Wallets, which vary in type, essentially secure the private key that provides access to the asset rights. They are the gateway to crypto interaction.

Digital signatures are derived from a user’s private key and the proposed transaction information. And because public keys and addresses are derived from a private key, advanced mathematics can verify if the private key that created a digital signature is the same private key used to create a public key. This cryptographic relationship allows digital signatures to provide independent verification of asset ownership on the network.

Wallet responsibility is extremely important given DeFi’s permissionless nature. Whoever has access to the private key, has access to the assets’ rights. However, users have options. For some, self-custody digital wallets provide the desired security and censorship-resistance attributes. For others, centralized entity wallets provide the requisite features and ease of use without key management.

A third wallet option is a fintech and DeFi hybrid. Web 2.0 fintech platforms offer users, customer support, and simple user experience design, which can pair well with DeFi’s decentralized, user-owned DeFi structure. The hybrid approach offers a more traditional user experience, facilitated and secured by the smart contract applications as the infrastructure layer. It may also serve as an effective gateway to onboarding new users into DeFi.

DeFi’s Growth Evident in Its Expanded Areas of Utility

Critical to DeFi’s maturation is that it increasingly attracts strong developer talent, who see a path to build new financial infrastructures. The more dedicated resources in DeFi, the greater its growth, innovation, and value potential. Developer activity illustrates the commitment to a project. Tracking open-source developer activity by the number of GitHub events that projects generate offers us a glimpse of the activity being conducted behind the scenes. During June 2022, leading DeFi platforms including Uniswap, Aave, Maker, and Compound averaged a combined activity of 1,395 on-chain events.6 Compared to 1,140 average events during June 2020, developer activity has risen roughly 18% year over year. This indicates positive traction.

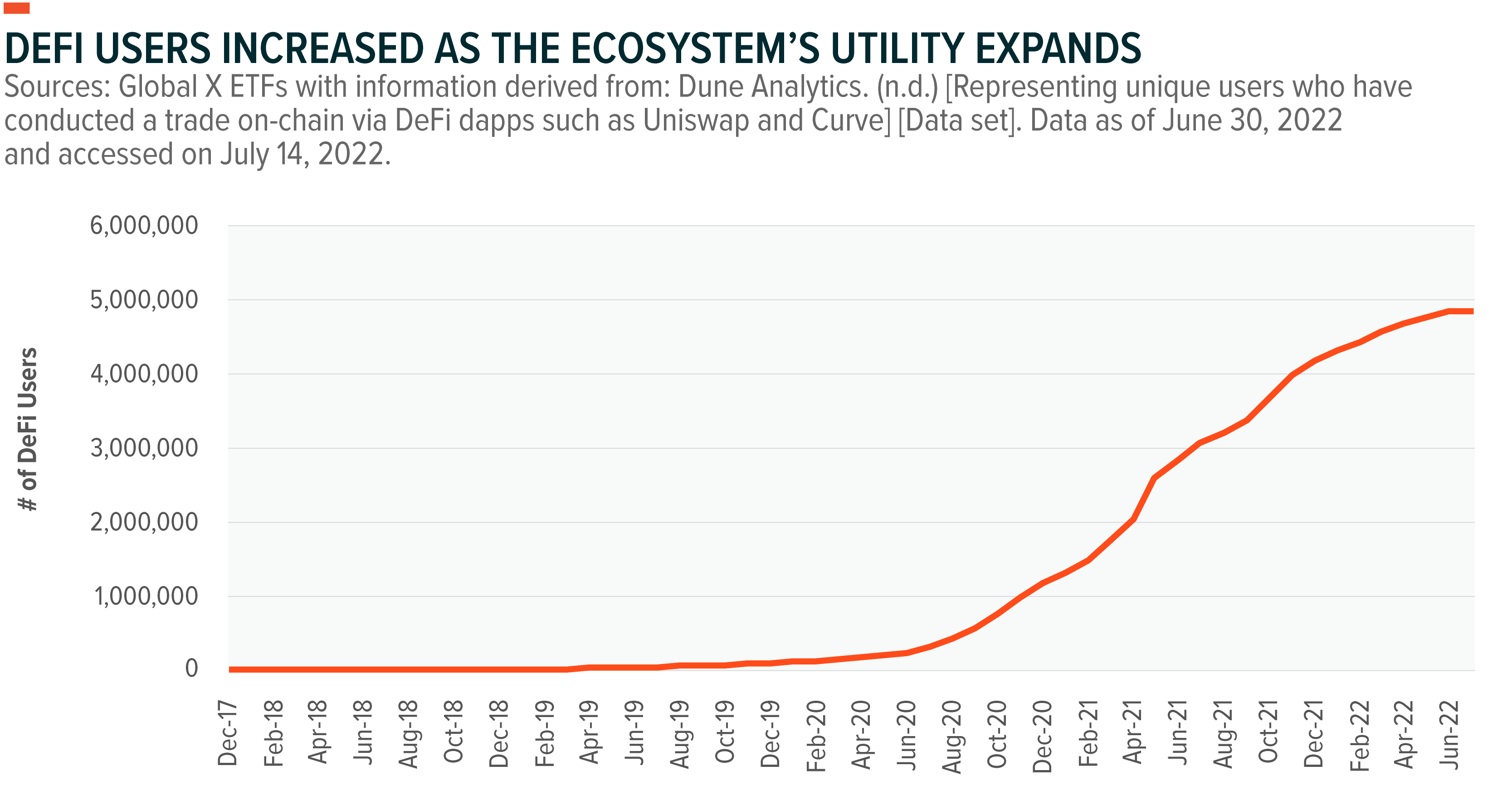

The number of unique addresses engaging with DeFi dapps has increased significantly over time, a validation of DeFi’s utility and a sign of its growth potential, especially considering the composability and network effects associated with these applications. More developers can lead to extended utility, which generally attracts more users and creates a positive feedback loop. As of June 30, 2022, roughly 5 million unique users had conducted an on-chain transaction through DeFi rails, as the chart below shows.

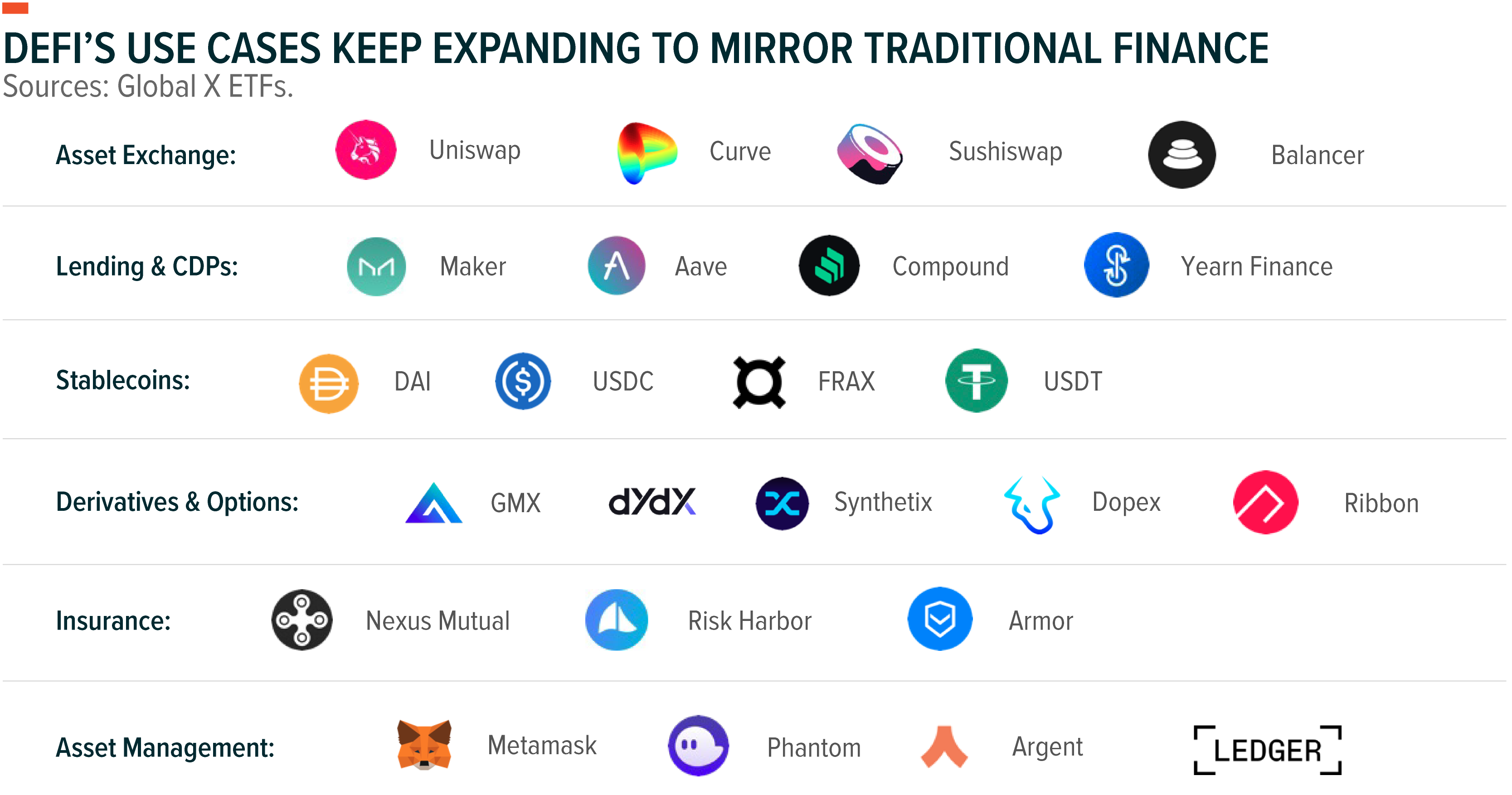

DeFi has developed into a rich ecosystem of dapps. As of today, these dapps offer users alternative platforms to engage in most all of the primary use-cases of the traditional financial services industry, including: saving, borrowing, lending, asset exchange, derivatives, insurance, and asset management. Most DeFi projects and protocols live in public and open-source blockchain infrastructure, and while the ecosystem is not limited to the projects in the chart below, these are the most prominent and valuable to date based on user adoption and economic activity.

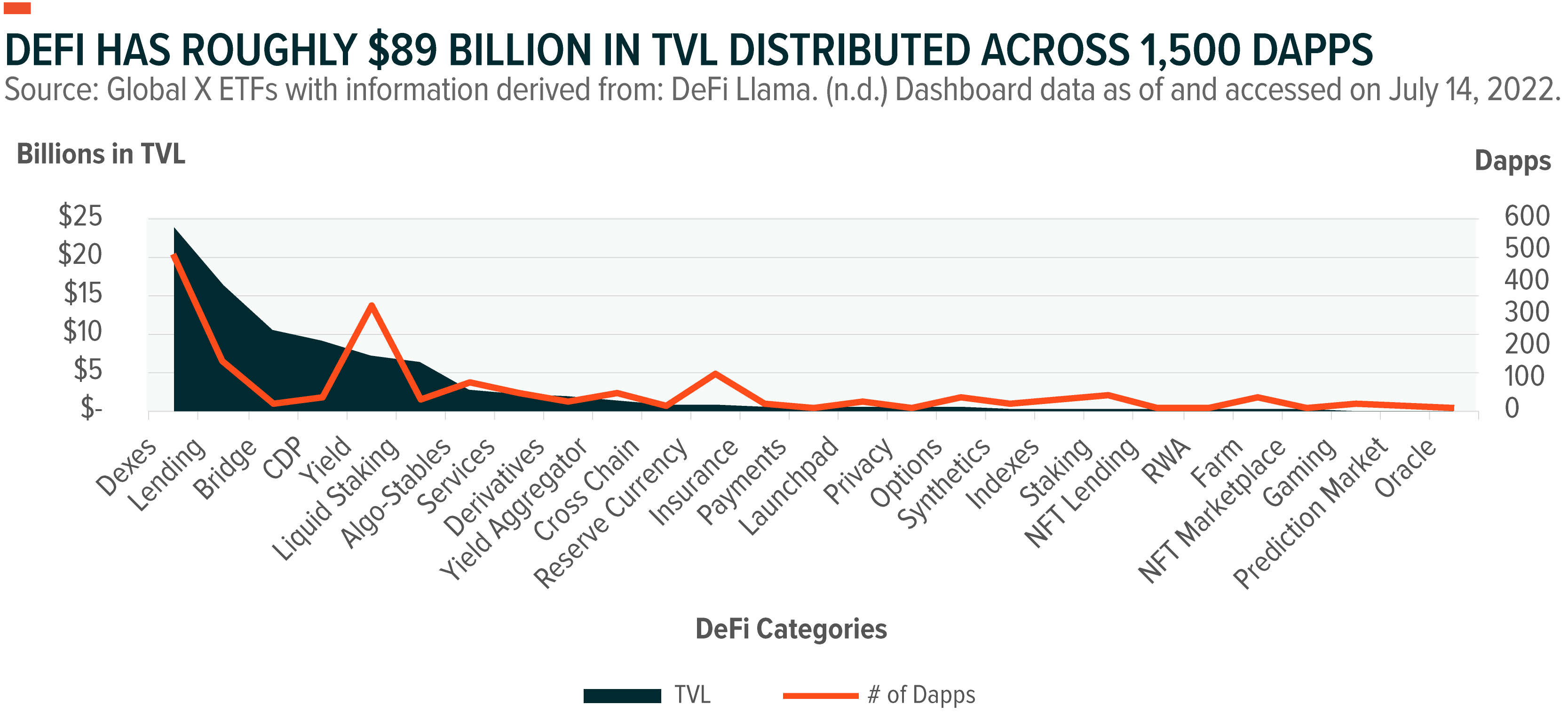

These projects, which have amassed massive amounts of users, can be assessed by the total monetary value locked (TVL) within them. TVL is an important DeFi metric because it provides insight into the monetary value deposited in the smart contract applications and serves as a reliable gauge of sentiment and growth. Locking assets within protocols can indicate growth, utility, and user conviction in the ecosystem depending on the stickiness of the project and the incentives offered to attract users.

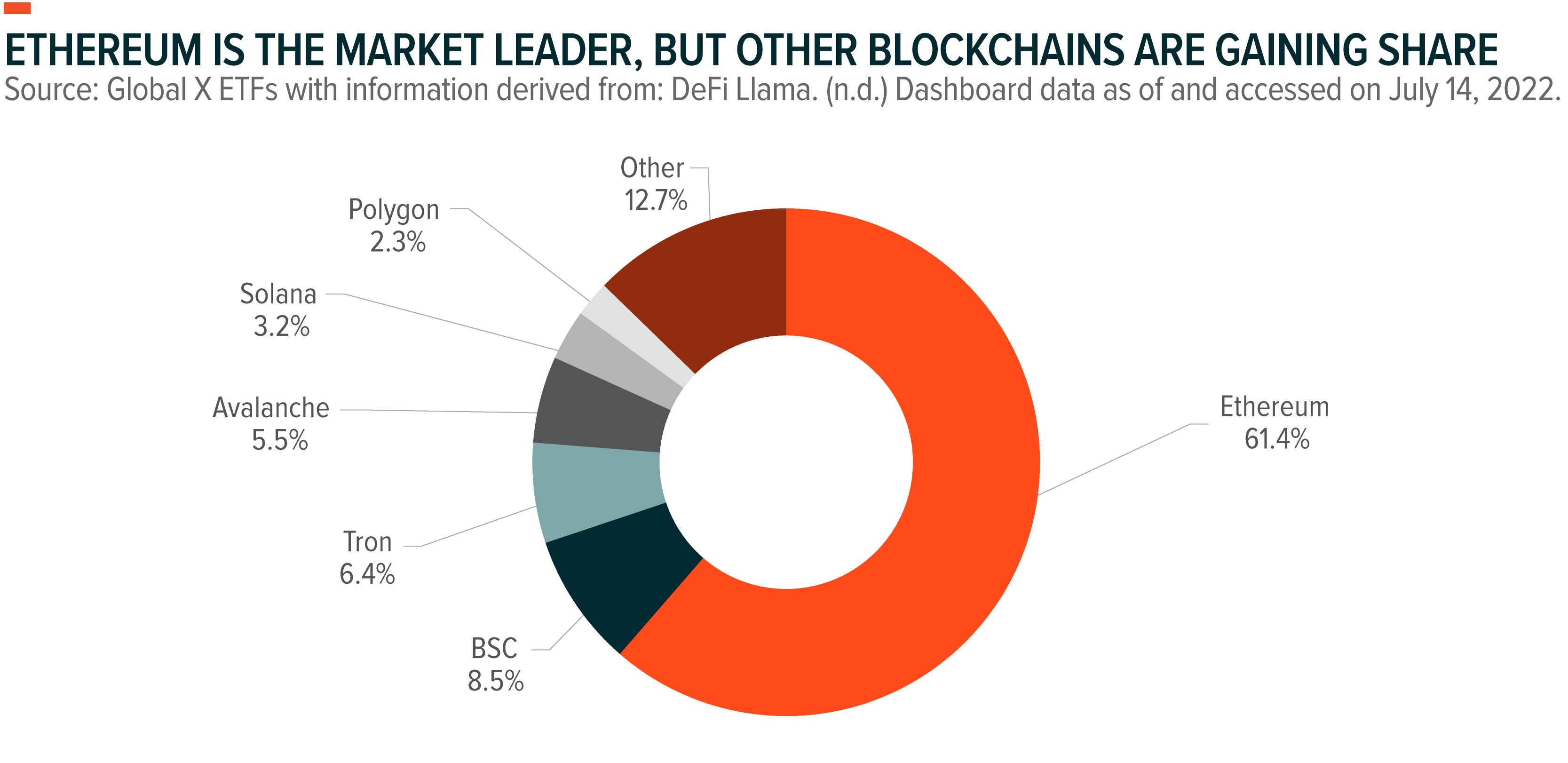

Today, DeFi projects are distributed across the leading smart contract blockchains. Developers leveraged the composability of dapps and general-purpose blockchains to build these ecosystems. As the first smart contract chain to market, Ethereum hosts roughly 60% of DeFi’s TVL. However, platforms like Solana and Avalanche, which offer scalability, high throughput, and low transaction costs, continue to gain market share and attract activity.

To illustrate DeFi’s value, exploring the leading dapps gives investors an idea of the utility behind DeFi. Aave is the leading protocol by TVL across any chain. Anyone can post collateral, borrow, and get liquidated based on the agreed leverage ratios. Aave has $8.75 billion of TVL spread through the Ethereum, Polygon, Avalanche, Arbitrum, Optimism, Fantom, and Harmony networks.7 It has over $3.86 billion in total assets available to borrow and a total borrower debt of roughly $1.5 billion. Interest earned by lenders totaled $282 billion with yields ranging anywhere between 0% to 30% depending on the asset.8

DeFi Paving the Way to Broader Digital Asset Adoption and Innovation

DeFi is in its infancy and we believe the power of DeFi dapps hosted on smart contract blockchains has significant disruptive potential across often slow-to-adapt traditional financial services, including lending and payments, insurance, reinsurance, insurance brokerage, investments, and foreign exchange. Developer activity continues to grow, leading to novel concepts that can revolutionize how the world engages with financial infrastructures. As DeFi extends its reach and users adopt its decentralized, inclusive nature, we expect it to facilitate broader crypto adoption and integration in the global economy.

Related ETFs

BKCH: The Global X Blockchain ETF seeks to invest in companies positioned to benefit from the increased adoption of blockchain technology, including companies in digital asset mining, blockchain & digital asset transactions, blockchain applications, blockchain & digital asset hardware, and blockchain & digital asset integration.

Click the fund name above to view the fund’s current holdings. Holdings are subject to change. Current and future holdings are subject to risk.

Image sourced from Shutterstock

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.