Zinger Key Points

- Housing affordability is increasingly an issue as market inventory falls due to lock-ins.

- This reduction in supply has increased house prices by 5.7%,

- Learn the top momentum trading strategies for today’s whipsaw market, live with Chris Capre on Sunday, May 4 at 1 PM ET. Reserve your free spot now.

Mortgage lock-in is an often overlooked area of the U.S. housing market. It hampers the ability of homeowners to sell their properties, adding to the shortage in supply of available homes, pushing house prices ever higher.

Here’s the problem. Most of the 50 million active mortgages in the U.S. have fixed rates. Those taken out prior to 2022 when the Federal Reserve began raising interest rates will have fixed mortgage rates at far below the prevailing market rate, which creates a disincentive to sell.

Families who, for whatever reason, need to upscale, instead of re-mortgaging at current high rates, are staying put and extending or making improvements to their existing homes.

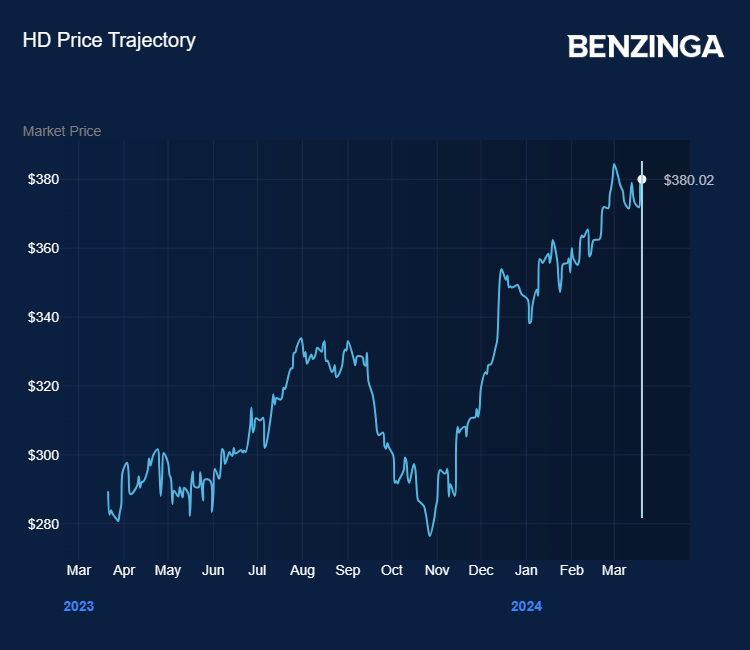

This has helped boost sales at home development retailers such as Home Depot Inc HD and Lowe’s Companies Inc LOW — both up around 30% in the past year — but has added to the problem of falling sales of existing homes.

This, in turn, is creating a housing market that is low on inventory, pushing the onus on to builders, such as D.R. Horton Inc DHI and Lennar Corporation LEN, to provide more new homes — and within demographics that help support housing market mobility.

Also Read: Housing Starts Rebound, Lift Homebuilder Stocks: Sign Of Economic Resilience

Worsening Affordability

The Federal Housing Finance Agency, in a report this week, said that for every percentage point that market mortgage rates exceed the origination interest rate, the probability of sale is decreased by 18.1%.

Currently, according to Freddie Mac, the average rate on a 30-year mortgage stands at 6.74%, down from the October 2023 peak of 7.79%.

This mortgage rate lock-in led to a 57% reduction in total home sales with fixed-rate mortgages in the fourth quarter of 2023, and prevented 1.33 million sales between the second quarter of 2022 and the end of 2023.

This reduction in supply, the agency said, increased house prices by 5.7%, offsetting the direct impact of elevated rates, which decreased prices by 3.3%.

“These findings underscore how mortgage rate lock-in restricts mobility, results in people not living in homes they would prefer, inflates prices, and worsens affordability,” said Ross Batzer, lead analyst on the report.

While the Federal Reserve is expected to begin its monetary easing cycle later this year, possibly cutting rates at its May meeting, the lag in mortgage rate decreases means that mortgage lock-in could persist for some years to come, the report says.

To address this problem, the authors suggest a number of solutions including tax credits for sellers of starter homes, or mortgage portability — where a homeowner retains financing terms when moving to another home.

Federal planners might, in the future, have to take a closer look at the potential homebuyer demographic and require homebuilders to provide more starter homes for young families.

Now Read: Settlement Shake-Up: National Association Of Realtors’ $418M Agreement Reshapes Real Estate Dynamics

Image created using artificial intelligence with Midjourney.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.