A rise in global trade tensions and growing uncertainty surrounding US economic policies under President Donald Trump have spurred investors to seek safe-haven investments.

Investors have turned to the Swiss franc for safety, given Switzerland's economic stability and moat against geopolitical risk. They have also turned to German Bunds to protect their investments.

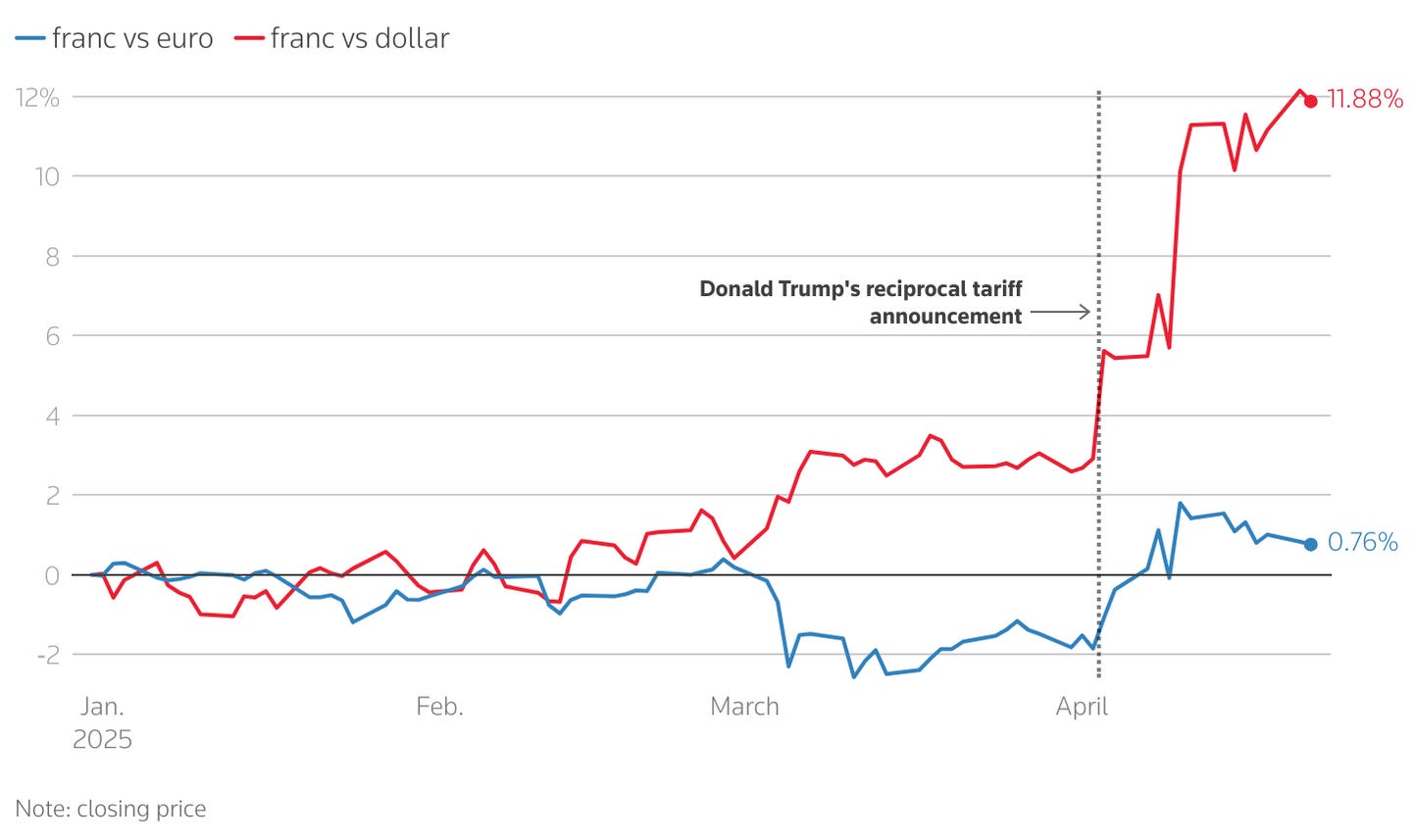

In 2025, the franc became the top currency performer among G10 currencies, outperforming even the Japanese yen. As of mid-April, the USD/CHF pair had exceeded the levels last seen since the Swiss National Bank (SNB) abandoned its 1.20 franc per euro floor in 2015. Hovering just above 0.80, this is the lowest US dollar traded against the franc in almost 14 years.

The surge in the Swiss franc reflects capital outflows from the US into Swiss assets following Trump's aggressive tariff policies. Between April 3 and April 6, Trump's trade restrictions wiped out over $10 trillion in global equity value.

"Investors are looking outside of the US for a safe, rule-of-law and we-can-rely-on-it government, with a well-run economy," April LaRusse, Head of Investment Specialists at Insight Investment, said.

LaRusse pointed at the ICE BofA MOVE Index, a measure of Treasury market volatility, which recently hit a one-year high, reinforcing the sentiment about turbulent expectations for the US Treasuries.

Trump Tariffs Spark Refuge in German Bunds

In previous cycles, the US bond market offered a cushion against equity sell-offs. This year has witnessed both asset classes tumble in tandem due to capital flight from the dollar.

However, Switzerland's $1 trillion economy is too small to absorb all the foreign interest, despite its debt capital market being as big as its GDP and increasing.

Thus, foreign capital also sought refuge in the German Bund. They currently yield around 2.50%, significantly higher than the Swiss 10-year bonds, which yield around 0.42%.

Bunds have rallied despite being jarred by Germany's aggressive fiscal expansion. The 10-year US-German yield spread widened by 30 basis points, reaching a 207 basis point difference on April 11. This development showcased the Bunds' strength as a perceived haven.

The German bond market accounts for around €4.2 trillion ($4.77 trillion), significantly smaller than the $28.6 trillion in the US. It also has around one-tenth in volume, limiting its ability to absorb large capital inflows.

As Steven Major, HSBC's Global Head of Fixed Income, said: “Bunds offer better value as a safe haven with yields still elevated after the recent shift in fiscal policy…But they simply can't match the depth and liquidity of US Treasuries.”

Foreign Investors Undeterred by German Recession

Not even the risk of a German recession has deterred foreign interest. The German Composite Purchasing Managers' Index fell to 50.1 in March, narrowly remaining above the 50 threshold, which divides expansion and contraction.

Germany cut its economic forecast from 0.3% growth to zero for 2025, predicting a year of stagnation after a two-year recession. Earlier this week, the International Monetary Fund also projected that Germany would stagnate this year.

Speaking to Bloomberg Television on Wednesday, April 23, Bundesbank President Joachim Nagel noted that Europe is in a "stagnating situation." He added that a jump in public spending should help the economy, taking an optimistic stance that such a plan is possible without an inflationary effect.

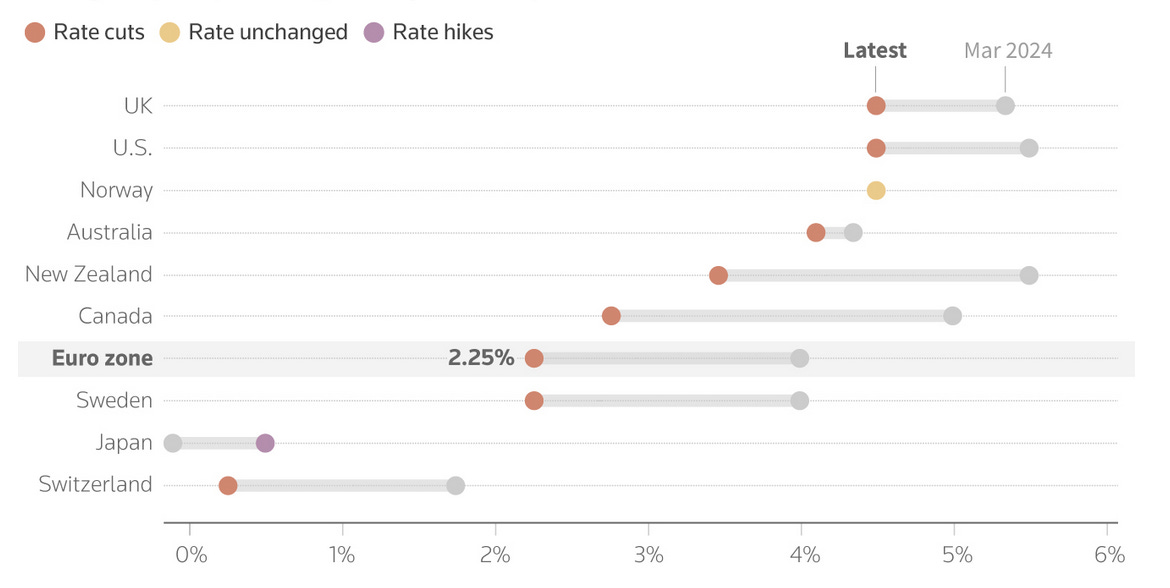

The European Central Bank cut rates three times this year, bringing the benchmark interest rate from 3.15% to 2.40%.

Swiss Central Bank Faces Rates Dilemma

While the Eurozone believes it can handle its higher public spending without an inflationary effect, after last month's rate cut, the SNB faces a dilemma. A strong franc exerts downward pressure on import prices and could reignite deflationary trends that Switzerland spent years trying to escape.

“For us as a small, open economy, the negative interest rate instrument is important,” governing board member Petra Tschudin said in February. “It allows us to manage the interest rate differential even in a low interest rate environment.”

After an eight-year stint, SNB ended its negative interest rate policy in 2022. However, speculation persists that the central bank could be forced to reconsider.

Switzerland experienced a far more stable monetary environment, with interest rates peaking at 1.75% before five rate cuts, including a 50 bps cut on December 12, 2024.

Goldman Sachs Predicts SNB Cuts to Negative Rates

Goldman Sachs considers SNB the only major central bank to resume sub-zero rates. The US investment bank projected a 25-basis-point cut to -0.25% by June. In contrast, most market participants see the SNB merely lowering the policy rate to zero.

This development would be troubling for Swiss bankers and savers. Negative interest rates compel banks to pass on costs to their clients, as the interest differential that generates revenue becomes negligible. Credit markets get distorted and risk appetite surges due to cheap capital.

UBS economist Maxime Botteron noted that limited franc sales by the SNB could already be underway, but he did not expect systematic interventions.

“Interventions are more flexible than interest rate cuts – the SNB can go into the market, sell some francs to ease the appreciation, and then stop,” he said.

With inflation remaining low and the risk of deflation returning—especially if the franc continues appreciating—the SNB's decision could be urgent.

Disclaimer:

Any opinions expressed in this article are not to be considered investment advice and are solely those of the authors. European Capital Insights is not responsible for any financial decisions made based on the contents of this article. Readers may use this article for information and educational purposes only.

This article is from an unpaid external contributor. It does not represent Benzinga’s reporting and has not been edited for content or accuracy.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.