How do you plan to create your retirement “paycheck”? Most likely, you expect to use a combination of Social Security, your retirement accounts, personal savings, and maybe an annuity. But there’s another source that’s often overlooked—dividends.

Stock dividends are an additional potential stream of income that you can use to help maintain your lifestyle in retirement. For example, if you owned 100 shares of a company that pays a $0.45 quarterly dividend, you would have an extra $180 a year at your disposal. This may not seem like much, but think of the possibilities if you owned multiple dividend stocks. Adding these stocks to your portfolio could also help your savings last longer; the more income you get from other sources, the less money you may have to withdraw from your retirement or brokerage accounts.

Let’s take a closer look at why you might consider dividends and how you could incorporate them into your retirement income plan.

The Case for Dividends

Bonds are sometimes the first thing people think of when they think about investing for income. However, dividend stocks offer many of the same potential benefits, plus one bonds generally don’t have—the opportunity for growth. The stocks in your portfolio could possibly grow over time, which means your savings may also continue to grow.

Companies that offer dividends are typically larger, more established businesses. And because the dividends are generally paid out of a company’s earnings or reserves, the payouts aren’t typically impacted by market fluctuations. Your check will likely arrive in your mailbox, bank account, or brokerage account on the designated payable date whether the market is up or down. This consistent stream of income could make it easier for you to budget for expenses and activities.

In addition, your income payments might increase from time to time, which could help you manage inflation, one of the biggest risks retirees face. Companies tend to raise their dividend rates when their projections for sustained growth are strong. Of course, there’s always a chance the reverse could happen or that a company could stop its payments all together. Dividends aren’t guaranteed.

And remember, it doesn’t have to be an either/or situation. Depending on your investment preferences and goals, you might decide to build a portfolio that includes a mix of dividend stocks and bonds.

Choosing Your Stocks

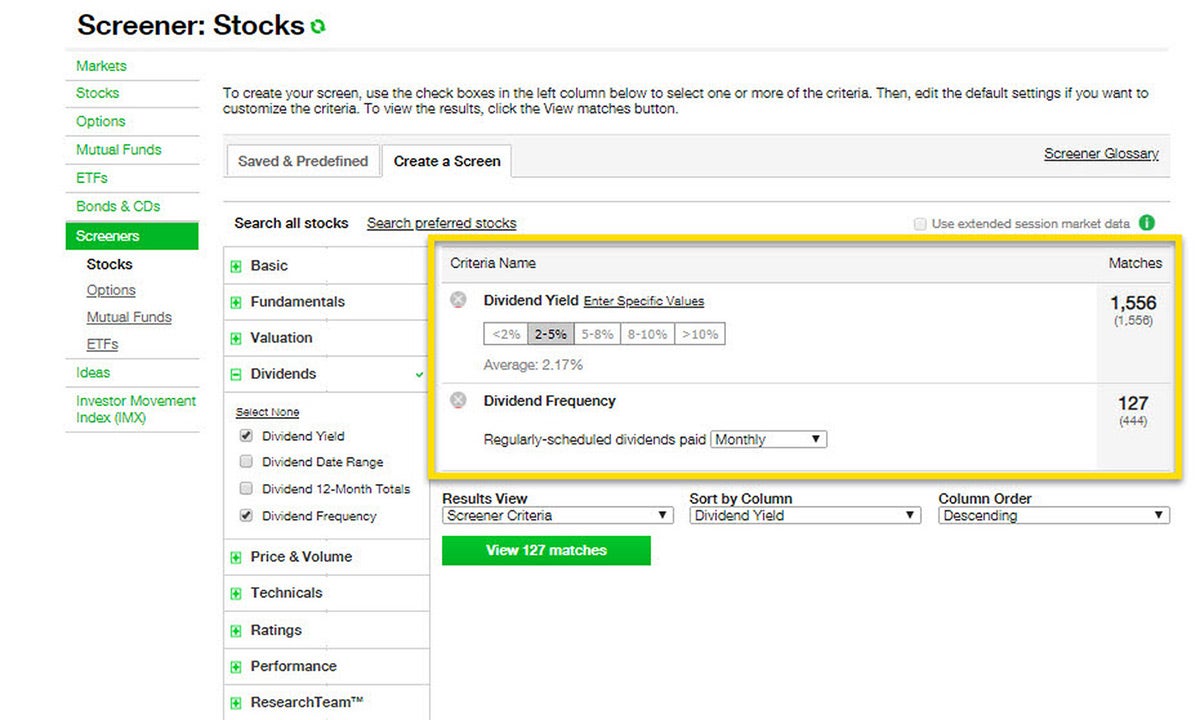

Not every stock pays a dividend. So how do you find the ones that do? One way is to use our stock screener. For example, you could use the screener to identify companies that pay monthly dividends and have a dividend yield of at least 2%. (See figure 1.)

FIGURE 1: STOCK SCREENER. First, identify stocks that pay a dividend. For illustrative purposes only.

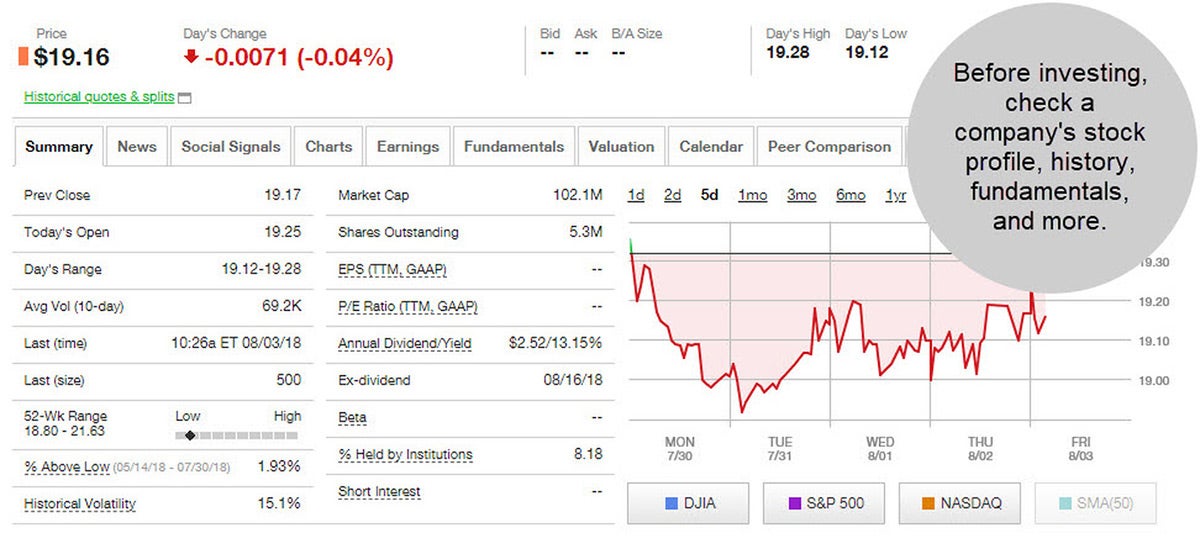

From there, you can review the company profile, performance history, investment fundamentals, and more for each stock that matched your criteria. (See figure 2.) That’s important because even though you’re looking to maximize your dividend income, the size of your check shouldn’t be the sole basis for your investment decision. The stocks you select also need to fit with your goals, time horizon, and risk tolerance. You’ll also want to check the company’s dividend history and cash flow. Keep in mind, though, that past performance doesn’t guarantee future results.

Once you find a stock you like, it’s important to understand the following dates so you know when you might expect your first payment:

- Record date. You have to own the stock by this date in order to receive the scheduled dividend.

- Ex-dividend date. If you buy the stock after this date, you’re not entitled to the payment. You won’t receive any income until the company declares its next dividend.

- Payable date. This is the day the dividend will be mailed or deposited into your bank or brokerage account.

FIGURE 2: CHECK THE DETAILS. The stocks you select need to fit with your goals, time horizon, and risk tolerance. For illustrative purposes only.

FIGURE 2: CHECK THE DETAILS. The stocks you select need to fit with your goals, time horizon, and risk tolerance. For illustrative purposes only.

Putting Dividends to Work For You

There are many ways you can use dividends to help supplement your retirement income. The approach you take may depend in part on whether you’re still working, your income expectations, and your investment style (do-it-for-me versus do-it-yourself).

Reinvest dividends. When you invest in a dividend stock, you have to decide whether to reinvest the dividends or to receive a cash payment. If you don’t have an immediate need for the money, it may make sense to choose the reinvestment option. Each dividend you reinvest purchases more shares of the stock, which may help build your savings and potentially increase the amount of future dividend payments. You can switch to cash whenever you’re ready to start receiving income. Any changes would typically take effect with the next scheduled dividend, assuming you changed your election before the ex-dividend date.

Build a dividend ladder. Companies pay dividends at different frequencies (monthly, quarterly, semiannually, and annually) and different months of the year. If you want to receive dividend income every month, you might consider creating a “dividend ladder” where you invest in stocks that have sequential payments. For example, let’s say you owned 100 shares of the following hypothetical stocks that pay quarterly dividends:

- HIJ: $0.50 dividend; January, April, July, and October

- LMN: $0.35 dividend; February, May, August, and November

- XYZ: $0.65 dividend; March, June, September, and December

Choose a dividend-paying mutual fund or exchange-traded fund (ETF). If you don’t want to spend time comparing individual stocks, you might consider investing in a mutual fund or exchange-traded fund instead. Keep in mind that your dividend check may vary more, since managers regularly buy and sell the stocks in their funds.

One final thought: dividends are generally taxable, so make sure you understand the potential impact on your tax bill before investing.

Today’s retirement can last 30 years or more, so running out of money is a real concern for many people. That’s why it’s important to create a plan that considers all possible sources of retirement income, including dividends.

If you decide to use dividends, remember the payments are not guaranteed and may be discontinued. Plus, the underlying common stock is subject to market and business risks including insolvency.

Information from TDA is not intended to be investment advice or construed as a recommendation or endorsement of any particular investment or investment strategy, and is for illustrative purposes only. Be sure to understand all risks involved with each strategy, including commission costs, before attempting to place any trade.

Image sourced from Pixabay

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.