Tesla Inc’s TSLA shares have had a bumper few weeks after erasing all their coronavirus-spurred losses. But it’s had such a high-voltage jolt to the upside that investors heading into Wednesday’s earnings report may be wondering whether the stock price momentum can continue.

Even excluding what may have been a speculative spike earlier this month that took the electric vehicle (EV) maker’s stock within spitting distance of $1,800, Monday’s close of $1,643 represented a more than 368% gain from its $350.51 nadir in March’s coronavirus selloff (see figure 1 below).

FIGURE 1: TESLA AND TECH. Shares of Tesla (TSLA—candlestick) have been on an incredible run in recent months, even when compared to wild runup in the tech-heavy Nasdaq Composite Index (COMP—purple line). Data source: Nasdaq Chart source: The thinkorswim® platform from TD Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

Accelerating Out Of Slump

Since reporting a surprise profit for the third quarter in a row last time around, a lot has gone right for the company.

Earlier this month TSLA said it delivered approximately 90,650 vehicles in the second quarter. That was well ahead of what analysts had been expecting, pushing shares past all-time highs to allow TSLA to eclipse Toyota Motor Corp TOYOF as the world’s most valuable automaker by market cap.

Goldman Sachs Group Inc GS initiated coverage on TSLA with a buy rating, citing the company’s leadership in the EV market, which has long term growth prospects. GS also noted the company’s early mover advantage, brand recognition, vertical integration, and success with the Model Y. As shares advanced, however, some analysts have begun to dial back a bit.

Tesla shares had gotten a jolt a couple of months ago when SpaceX, a privately held company that shares Elon Musk as CEO, successfully launched human astronauts into space. Although the two companies are separate, the public victory for SpaceX seemed to feed into the aura around Musk as sort of a cult hero to some investors.

But cults of personality can cut both ways. At one point during the second quarter, Musk delivered a head-scratching statement about his company’s stock price being too high. That helped push shares down, but they certainly didn’t stay there.

As the second quarter came to a close, TSLA shares, which had already erased their coronavirus losses, began a remarkable rally. Through the close of Monday’s trading, shares are up more than 50% from their June 30 close.

Are Share Prices Sustainable?

With such an amazing influx of investment, traders and investors might be wondering whether these prices are sustainable, especially in light of what just happened with Netflix Inc NFLX. In NFLX’s case, the company’s stock also hit a record high prior to earnings and guidance that ended up leaving investors deflated.

Netflix’s pullback isn’t all related to its latest earnings report. It also comes as some investors have been rotating out of big tech-related stocks that they had been piling into in search of relatively stable names to invest in amid wider uncertainty about the economic reopening.

Depending on what Wednesday’s numbers show, the runup in TSLA shares may have priced in a high hurdle of expectations. Like NFLX, TSLA isn’t a technology company per se, but one that relies heavily on technological advancement in order to keep its products and platform front and center with investors and consumers.

Downside Risks Grow

Of course, TSLA and NFLX are very different companies, but if the extra boost that tech-related shares have gotten recently means that TSLA stock has gotten ahead of its skis, there could be some risks to the downside.

A consensus price target among analysts has been on the rise, but Tesla’s share price has tended to outpace those targets—by a sizable margin. As of the end of trading Monday, an analyst consensus price target was $707.19 for Tesla’s shares, up more than $100 from 30 days prior, according to MarketBeat. Over the same period the potential downside between TSLA’s actual price and that price target had increased to 56.9% from 39.7%.

And like many other companies out there, there’s also a coronavirus overhang. With millions still unemployed, there may be a risk that people might hold off on purchasing a car until their finances get back in shape.

The Macro Trends

But the TSLA story isn’t just about one quarter; it’s about long-term trends. And those trends have been pointing away from gas-powered vehicles toward those powered by electricity. For example, according to a report last month by the International Energy Agency, EVs registered a 40% year-on-year increase in 2019. And that was on top of a 2018 that had also shattered records.

Another trend that could be pointing TSLA’s way: price parity between electric and internal combustion engines. A report by Bloomberg NEF sees the price per kilowatt-hour ($/kWh) dropping to around $94 by 2024, and to $62/kWh by 2030. To put that into perspective, in 2010, it was $1,160/kWh and in 2018 it was $176/kWh. According to Bloomberg, the advancement in battery pack technology could mean upfront price parity between gas and electric sometime in 2022.

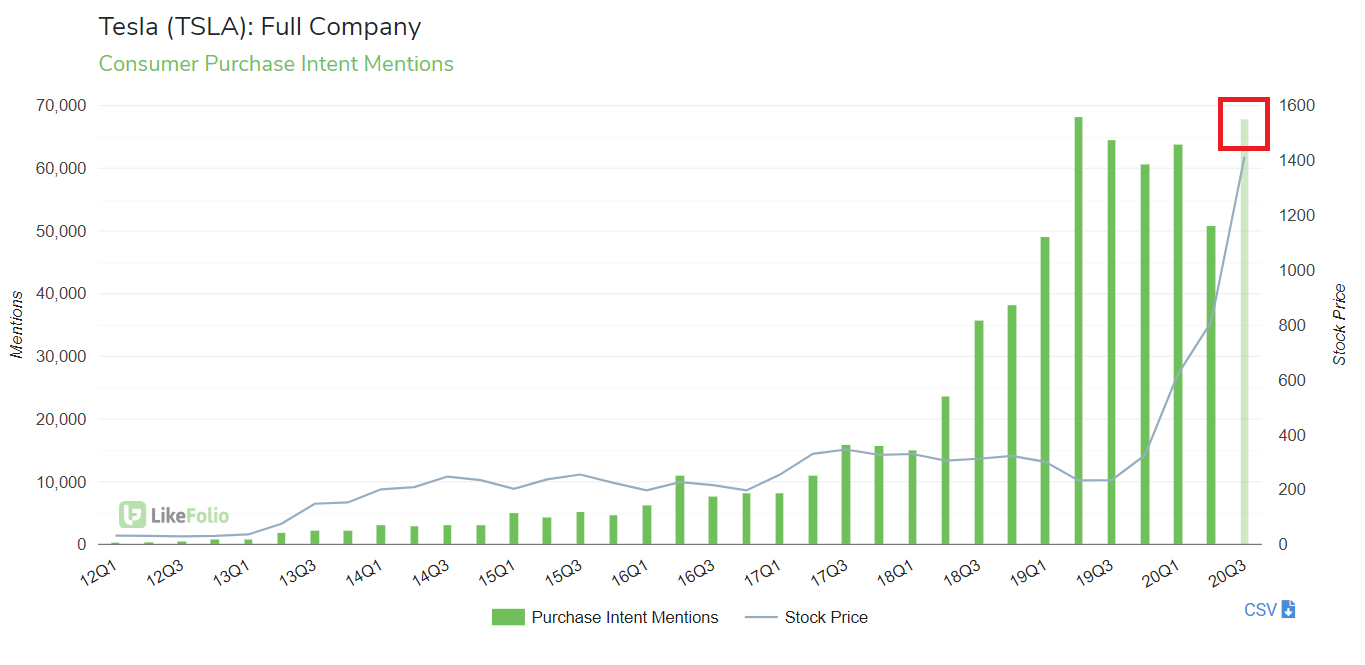

Finally, if sentiment analysis from LikeFolio is a guide, 2020 could be a watershed year, despite the spring coronavirus-led consumer pullback. According to LikeFolio data, Purchase Intent mentions for the current quarter (beginning in July) are pacing +34% quarter-over-quarter and +5% year-over-year, largely driven by strength in TSLA’s Model 3 brand (see figure 2).

FIGURE 2: ELECTRIFIED SENTIMENT. Purchase Intent mentions have risen for TSLA products along with share prices. Data source: LikeFolio. For illustrative purposes only. Past performance does not guarantee future results.

The short answer ahead of Wednesday’s earnings could be that the macro trends favor TSLA and other makers of electric vehicles, but recent share price gains have substantially raised the expectations bar.

TSLA Earnings And Options Activity

TSLA is expected to report an adjusted loss of $0.11 per share, according to third-party consensus analyst estimates, on revenue of $5.23 billion. It should be noted, however, that analyst estimates have varied widely, with a low earnings estimate of -$2.53 per share to a high of $1.45 per share. The options market has priced in an expected share price move of 12.6% in either direction around the earnings release, according to the Market Maker Move™ indicator on the thinkorswim® platform.

Looking at the July 24 option expiration, put activity has been highest at the 1200 and 1500 strikes. But there have been higher concentrations to the upside, particularly in the 2000 and 2500 call strikes. The implied volatility sits at the 55th percentile as of Tuesday morning.

Note: Call options represent the right, but not the obligation, to buy the underlying security at a predetermined price over a set period of time. Put options represent the right, but not the obligation, to sell the underlying security at a predetermined price over a set period of time.

TD Ameritrade® commentary for educational purposes only. Member SIPC. Options involve risks and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options.

Photo by Pixabay, from Pexels.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.