Zinger Key Points

- A feature of past episodes of market turmoil was feverish demand for protection that does not carry static exposure to direction.

- Instead, the payouts are asymmetric.

- Find out which stock just claimed the top spot in the new Benzinga Rankings. Updated daily— discover the market’s highest-rated stocks now.

Friday marked the roll off of $460 billion in derivatives across single stocks and $855 billion of S&P 500-linked contracts, according to a Bloomberg report.

What It Means: Heading into this event, market participants sought protection and were well-hedged. During this latest episode of equity market weakness, unlike in the past, participants were not feverishly demanding protection and, at the same time, volatility has been well-supplied.

The latter remark is a reflection of volatility suppressing activities, according to comments online by SqueezeMetrics, a provider of options market analyses.

Investors de-grossed and, by that token, “you don’t have to protect what you don’t own.”

Similarly, analytics service SpotGamma said investors are potentially monetizing (i.e., selling to close) existing hedges and writing put options against static short equity exposure, lending to the suppressive forces outlined above.

“Due to this supply and demand dynamic, we’ve observed divergence in the volatility realized, versus that which is implied by options activity,” SpotGamma said in a note sent to Benzinga.

Graphic: Via Robson Chow, founder at Tradewell, a tool that empowers traders to build and test trading ideas. Shown are times when the realized volatility is in excess of that implied.

A Nonlinear Reaction: A feature of past episodes of market turmoil was feverish demand for protection that does not carry static exposure to direction (i.e. delta).

Instead, the payouts are asymmetric (i.e. convex) and this is a reflection of those options’ dynamic deltas with respect to changes in underlying price (gamma) and volatility (volga).

Accordingly, liquidity providers’ response to this demand is reflexive and may tend toward the exacerbation of underlying movement as they sell into weakness to hedge puts they’re short.

The Ambrus Group, a volatility arbitrage fund who Benzinga has spoken with in the past, recently published a paper on these dynamics and more. Check it out here.

Structural Flows In Action: Many traders were caught off guard after the Federal Open Market Committee (FOMC) event earlier this month.

Heading into that event, markets were oversold and participants were demanding protection.

“Barring a worst-case scenario, if markets do not perform to the downside (i.e., do not trade lower), those highly priced (often very short-dated) bets on direction will quickly decay, and hedging flows with respect to time (charm) and volatility (vanna) may bolster sharp rallies,” Physik Invest recently reported.

After participants’ fears with respect to a more hawkish FOMC announcement were assuaged, options bets were sold and priced down. The decreased probability of them paying out played into the covering of static delta liquidity providers held short.

Graphic: Via SpotGamma. “SPX prices X-axis. Option delta Y-axis. When the factors of implied volatility and time change, hedging ratios change. For instance, if SPX is at $4,700.00 and IV jumps 15% (all else equal), the dealer may sell an additional 0.2 deltas to hedge their exposure to the addition of a positive 0.2 delta. The graphic is for illustrational purposes, only.”

Kai Volatility’s Cem Karsan, who Benzinga interviewed last year, explained this was purely “structural buyback” and the removal of the liquidity providers’ short inventory took from the market a support mechanism.

This left the door open to fundamental weaknesses, or “the incremental effects on liquidity (QE/QT).”

Graphic: Via CrossBorder Capital. “Latest weekly Fed liquidity injections and the S&P 500. Bigger the bull, the harder they fall? Fed trying to crash [the] economy to kill inflation [and] Wall Street is the victim.”

Why Is This Relevant? Pursuant to the remarks that volatility is well supplied, SpotGamma tells Benzinga there’s not as much stored energy to catalyze a rally, as in past episodes when implied volatility was wound up.

“For divergences in volatility realized and implied to resolve, it would likely take forced selling,” and it’s difficult to see how that happens barring a change in the fundamental environment.

Karsan, in a December 2021 commentary, argued for this potential of “exacerbated” downtrends that have a hard time reversing.

“This is due to a lack of downside ‘catharsis’ and a dearth of supportive, concentrated Vanna/Charm flows that are helpful in achieving the necessary support for an impending rally.”

These positive flows, driven by liquidity providers’ buyback of hedges to offset options delta-decay, in the years prior, would bolster markets near options expirations (OPEX) and, particularly, in the case of charm, were often front-run.

Graphic: In August of 2021, Pat Hennessy of IPS Strategic Capital, broke down returns for the S&P 500, categorized by the week relative to OPEX.

That’s not the case, today, as Karsan accurately foresaw happening last year.

What To Expect: Heading into Friday’s session, Bloomberg quoted the 4,000 S&P 500 strike as having 93,000 contracts set to roll off.

Per SpotGamma insights released in the days prior, this OPEX would likely coincide with the removal of a lot of in-the-money put delta.

That means “market makers will be free to buy back stocks to cover the short exposures that are no longer needed,” and that could open a window during which markets have less pressure to rally against.

“Any ultimate rally off of OPEX, we’d consider to be short covering, and subject to swift reversals.”

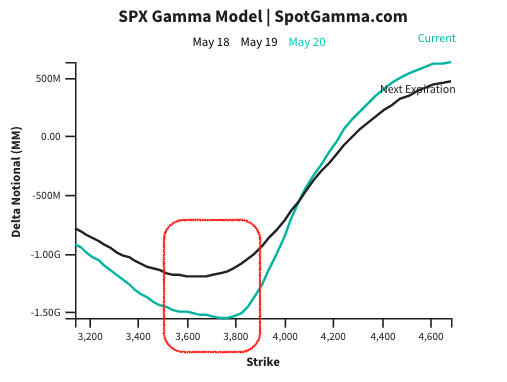

Graphic: Via SpotGamma. With continued weakness, the pressure liquidity providers must add on the underlying market in light of their hedging activities, flatten out. This may be attributed to options hedges these liquidity providers have on themselves, SpotGamma explains.

Have questions or clarifications? Please email renato@benzinga.com.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.