Zinger Key Points

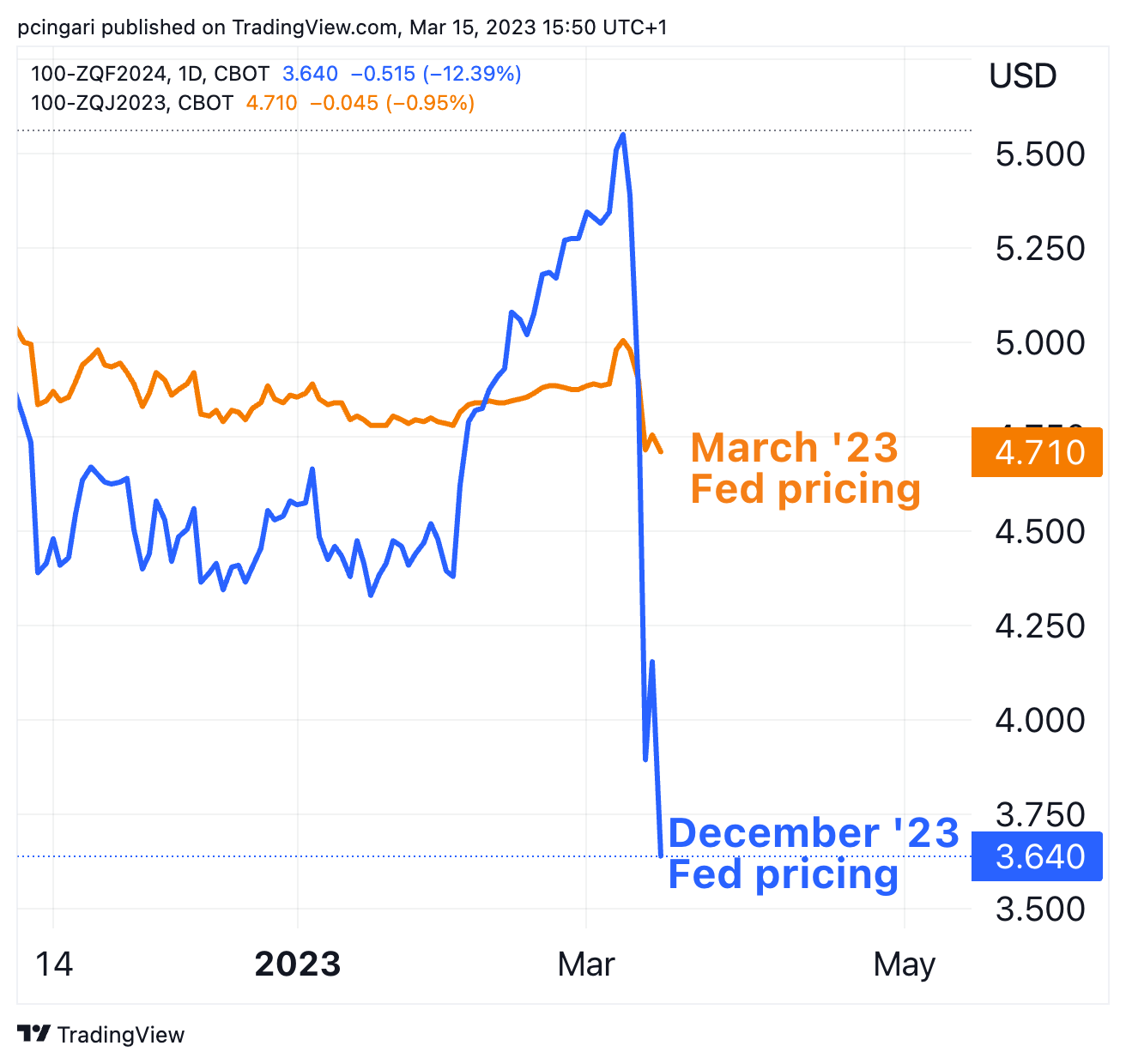

- Traders trimmed their rate expectations throughout the year, and now expect Fed funds to be at 3.6% in December 2023.

- The figure reflects a nearly full percentage point cut from present levels.

- Get real-time earnings alerts before the market moves and access expert analysis that uncovers hidden opportunities in the post-earnings chaos.

Recent economic indicators in the United States point to an increased risk of a recession, encouraging many traders to anticipate a more rapid Federal Reserve policy shift.

In February, retail sales declined 0.4% month-over-month, below market expectations of a 0.3% drop and down from a 3.2% increase in January.

The largest monthly drops were seen in sales at furniture stores, down by 2.5%, and food services and drinking places, a 2.2% drop.

The producer price inflation (PPI) fell 0.1% month-over-month in February 2023 against market estimates of a 0.3% increase. The PPI index was 4.6% higher on an annual basis, down from 5.7% the previous month and falling short of the market expectation of 5.4%.

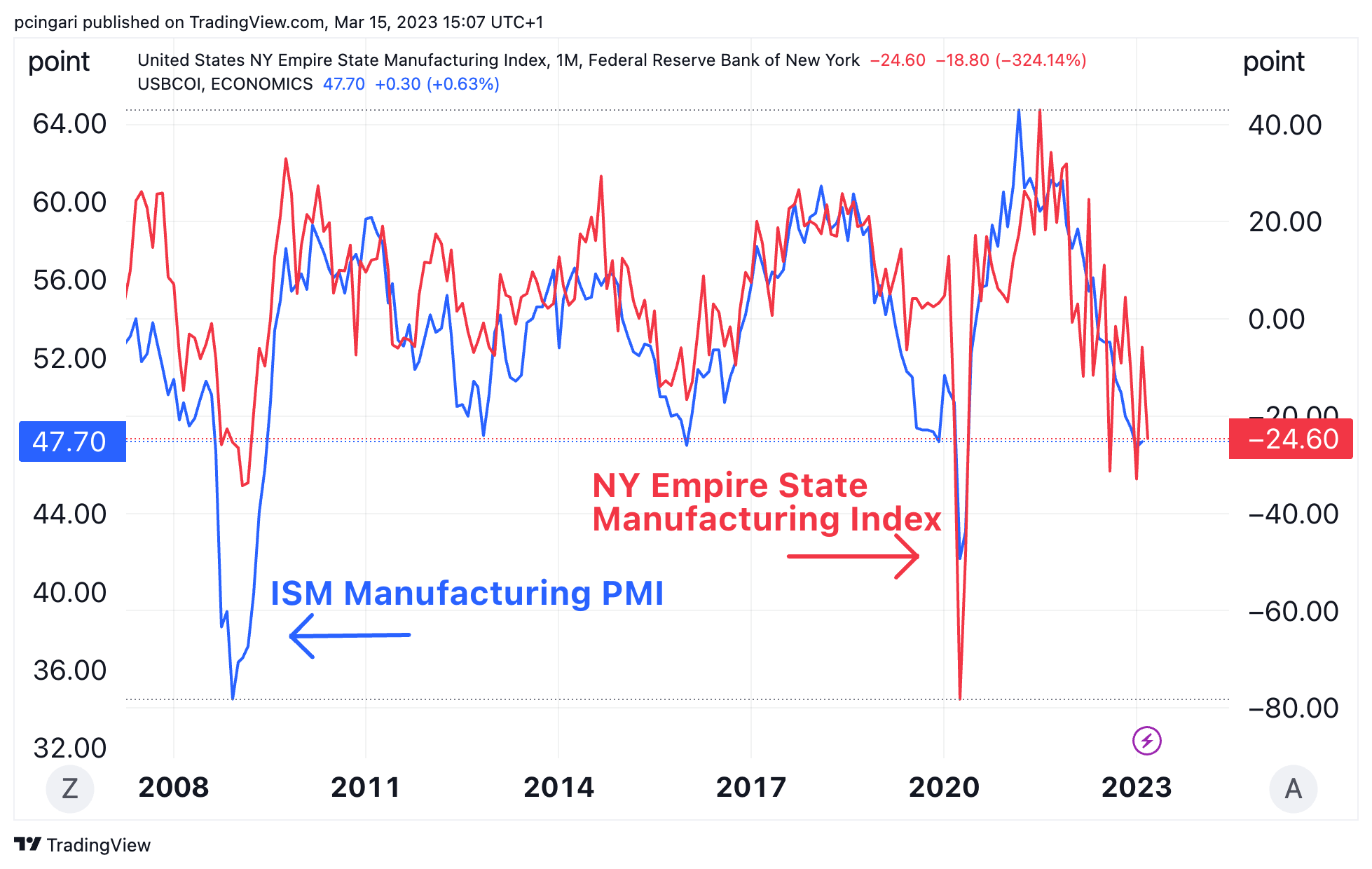

In terms of manufacturing activity, the NY Empire State Manufacturing Index plummeted to negative 24.6 in March 2023, down from negative 5.8 in February and considerably below market expectations of negative 8. This measure has traditionally been a good predictor of the broader US ISM Manufacturing index.

Chart: TradingView.

Fed Rate Hike Expectations Tumble: Weaker-than-anticipated retail sales and producer inflation dampened the market odds for Fed rate hikes.

Money markets are assigning a 60% probability that rates will remain unchanged at the upcoming Fed meeting on March 22 compared to a 40% chance that they will be raised by 25 basis points. Markets were pricing in a 50-basis-point raise with a roughly 80% possibility only a week ago.

Traders trimmed their rate expectations throughout the year, and now expect Fed funds to be at 3.6% in December 2023, reflecting a nearly full percentage point cut from present levels.

Chart: TradingView

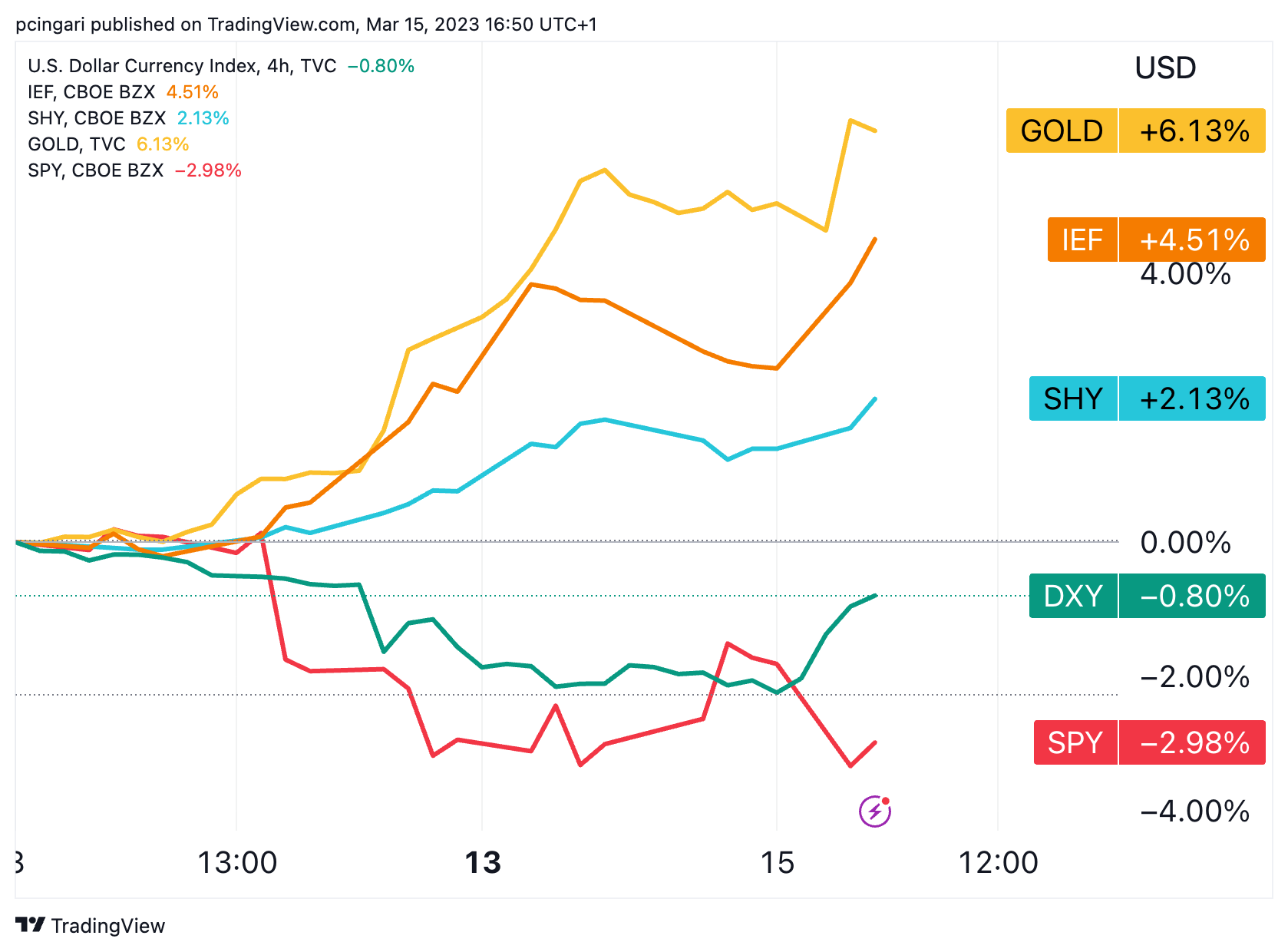

Treasuries, USD, Gold Rally: U.S. Treasury yields have fallen throughout the yield curve. Yields on two-year Treasury notes fell roughly 45 basis points to 3.8%, hitting the lowest level since mid-September 2022.

The 10-year Treasury yield fell 28 basis points to 3.42%, approaching February's lows.

The iShares 1-3 Year Treasury Bond ETF SHY is up 0.8% Wednesday, rising as much as 2.4% since March’s lows. The iShares 7-10 Year Treasury Bond ETF IEF gained 2% on the day and is now up 5.6% since its March lows.

The dollar surged, aided by a risk-off sentiment in European assets, as a result of turmoil in the banking sector. Credit Suisse Group AG CS dropped 16% after its largest shareholder, the Saudi National Bank, refused to inject further capital into the troubled bank.

The EUR/USD fell 1.6% to 1.0550, while the broader US Dollar Index (DXY) rose 1% to 104.8 levels.

The sell-off in US equity indexes resumed Wednesday. The S&P 500 index, which is tracked by the SPDR S&P 500 ETF Trust SPY, fell 1.8% to 3,850 points, while the Dow Jones lost 1.9% to 31,550 points, hitting its lowest level since the end of October 2022. The tech-heavy Nasdaq 100 fell 1.3% to 12,031 points.

Gold continued to tick higher, gaining 1% to $1,922/oz and acting as a safe-haven and recession-hedge asset.

Chart: TradingView

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.