This week, Jerome Powell spoke to Congress and was more dovish than he’s been in years. He’s gone from channeling former Fed Chairman, Volker, who crushed inflation with interest rates approaching 20% to sounding like Volker’s predecessor, Arthur Burns, who reduced interest rates before getting inflation under control. We saw weaker than expected job reports, and I think the real situation is weaker than the data indicates. There were new all-time-highs for both Bitcoin and gold leading some to notice there’s a bull market in both risk-on and risk-off. What should you do? Gas and oil prices are rising partly due to continued production cuts from Saudi Arabia and Russia. Finally, we have a bonus 6th thing as we watch to see if the investor bailout of New York Community Bank ($NYCB) works. Cue Janet Yellen reassuring us all the banking sector is “sound”.

This week, we’ll address the following topics:

-

Jerome Powell spoke to Congress, and seems to have changed his approach. Has he gone insane?

-

Lots of jobs reports. Can we trust the data?

-

As Bitcoin hits an all-time high, the Bitcoin bears revise their selective memory AGAIN. I provide my view.

-

Gold hits an all-time high. What does this mean? Risk-on and risk-off at the same time? Time to panic?

-

Saudis keep production cuts. Brent crude back over $80. Gas prices rising.

-

New York Community Bank NYCB needs a huge capital infusion. Janet Yellen wrong again.

Before we move on, a round of applause for DKI Intern, Andrew Brown. This week, Andrew prepared the graphs for this edition of the 5 Things, pitched two excellent “Things”, and did some of the writing. At DKI, we take seriously our commitment to helping our interns prepare to be contributors. Every week, Andrew is producing more content and more value. We’re proud of the quick progress he’s making, and hope you’ll appreciate his contribution to this week’s edition.

Ready for a new week of breaking the glass in case of emergency? Let’s dive in:

-

Jerome Powell Says the Craziest Things:

Federal Reserve Chairman, Jerome Powell, has spent more time in front of television cameras than any prior Fed Chair I can remember. He’s generally calm and in control in front of an audience, and this week, he addressed Congress. Powell reiterated his expectation that the next change in the fed funds rate would be a reduction, and that he expected this to happen later this year. That’s consistent with DKI’s view, and with his prior comments. However, he did say one thing that caught me by surprise.

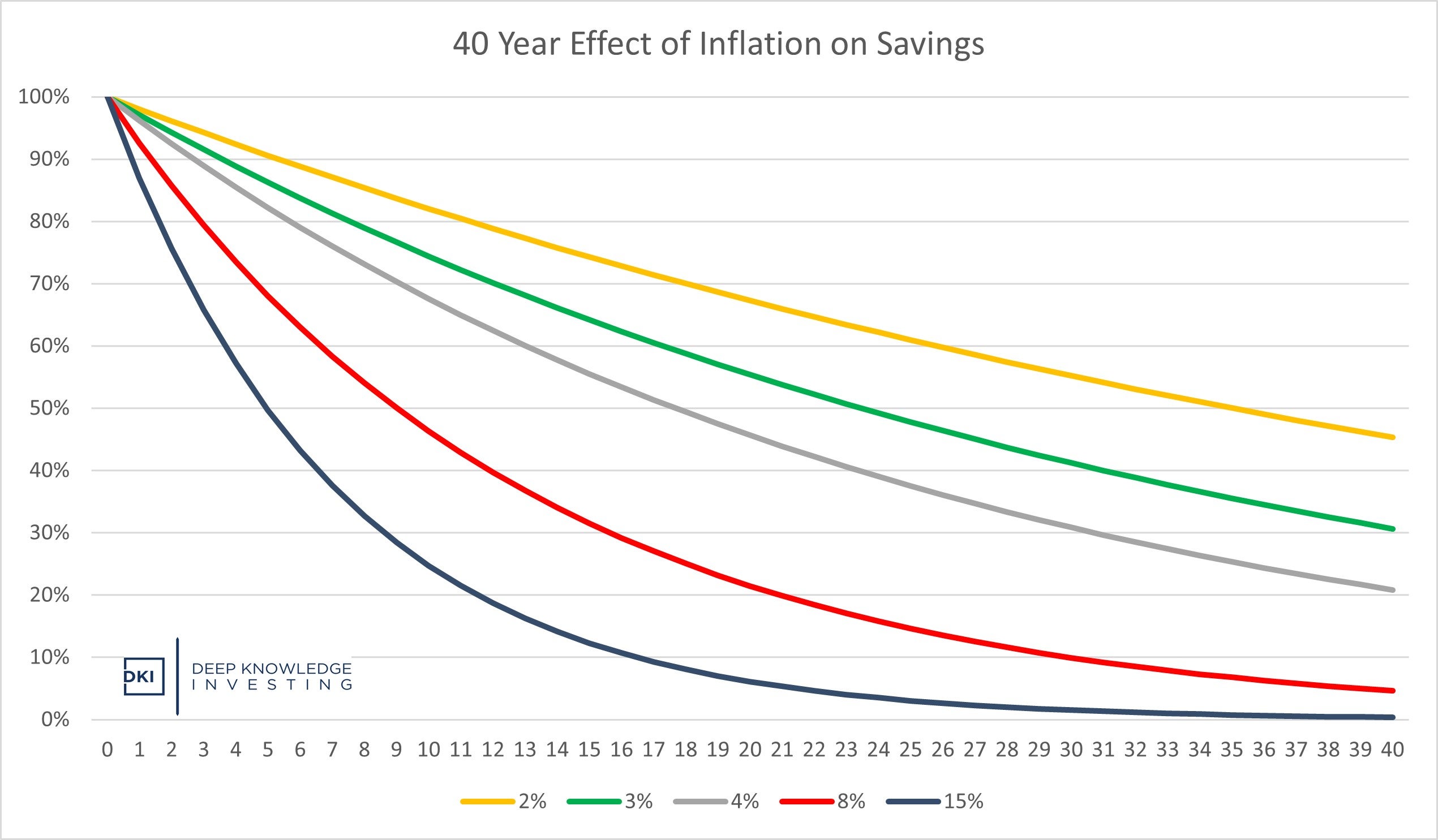

Compounded over decades, there’s a big difference between 2% and 3%.

DKI Takeaway: Powell said that he’d consider rate cuts when the Fed has “gained greater confidence that inflation is moving sustainably” towards the 2% target. Said another way, Powell is indicating a willingness to lower rates BEFORE inflation hits 2%. That’s the same mistake former Fed Chair, Arthur Burns, made in the 1970 with disastrous results. The reason this matters is over a 40-year working career, a 2% inflation rate steals 55% of the value of your savings. A 3% inflation rate means you lose 69% to government-sponsored theft. Given massive Congressional overspending, Powell should stick to his “higher for longer” mantra. That’s going to be an unpopular opinion among many of you while others are more concerned about constantly rising prices.

-

Can We Trust the New Jobs Reports?:

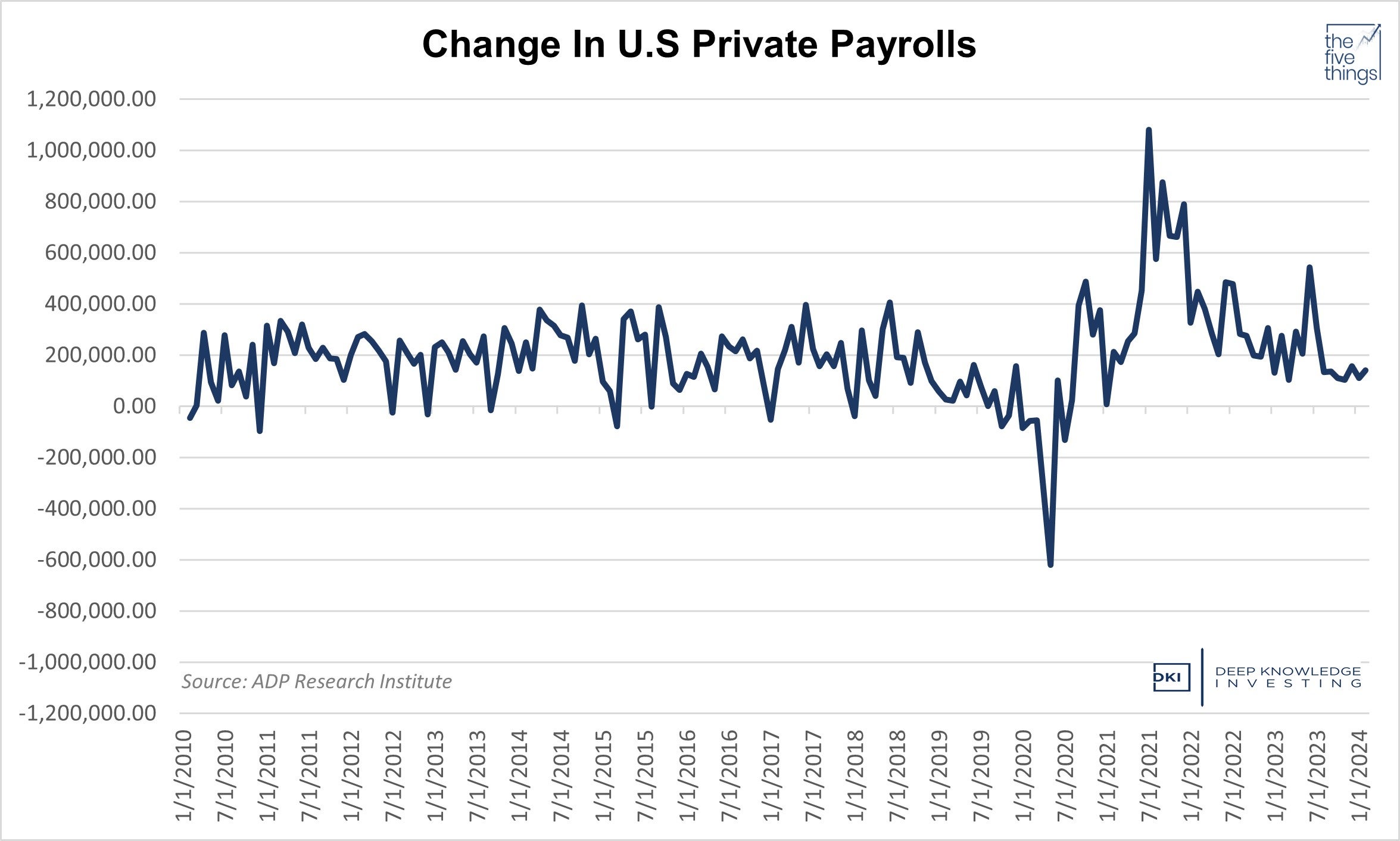

Lots of employment data out this week. The ADP payroll number was up by 140k which was below the 150k estimate, but above last month’s 111k. This report showed a healthy 5.1% increase in wages. The JOLTS report showed job openings of 8.9MM which was below the 9.3MM estimate. Friday’s job growth number of 275k beat the 198k estimate while unemployment rose from 3.7% to 3.9%. Is this bad, or worse?

Slightly below expectations, but still a decent number.

Almost 9MM jobs appears good – if those jobs are real.

DKI Takeaway: I think reality is worse than the data shows. The reports showing new jobs added don’t account for the fact that most of this activity is people taking multiple part-time jobs. That’s not awful, but isn’t an indicator for a healthy economy. One reason the number of job openings was below expectations is fewer people quit their jobs due to a weakening labor market. Companies don’t need to try to replace those workers. Most of the new jobs are in government and health care (which is more than 50% government payors) so the government is creating its own results. Downward revisions of previous reports continue and are so large that most of us don’t trust the initial reports anymore. Finally, many of the jobs listed don’t really exist and companies aren’t trying to fill them. The one positive is if employment and unemployment are both rising, it means that higher wages are bringing in more workers from the sidelines which is good for everyone. Still, the weaker employment situation is a positive for those looking for the Fed pivot to lower rates. Maybe we should have called this version of the 5 Things the “lower and sooner” edition.

-

Bitcoin Bears Revise Their Selective Memory Again:

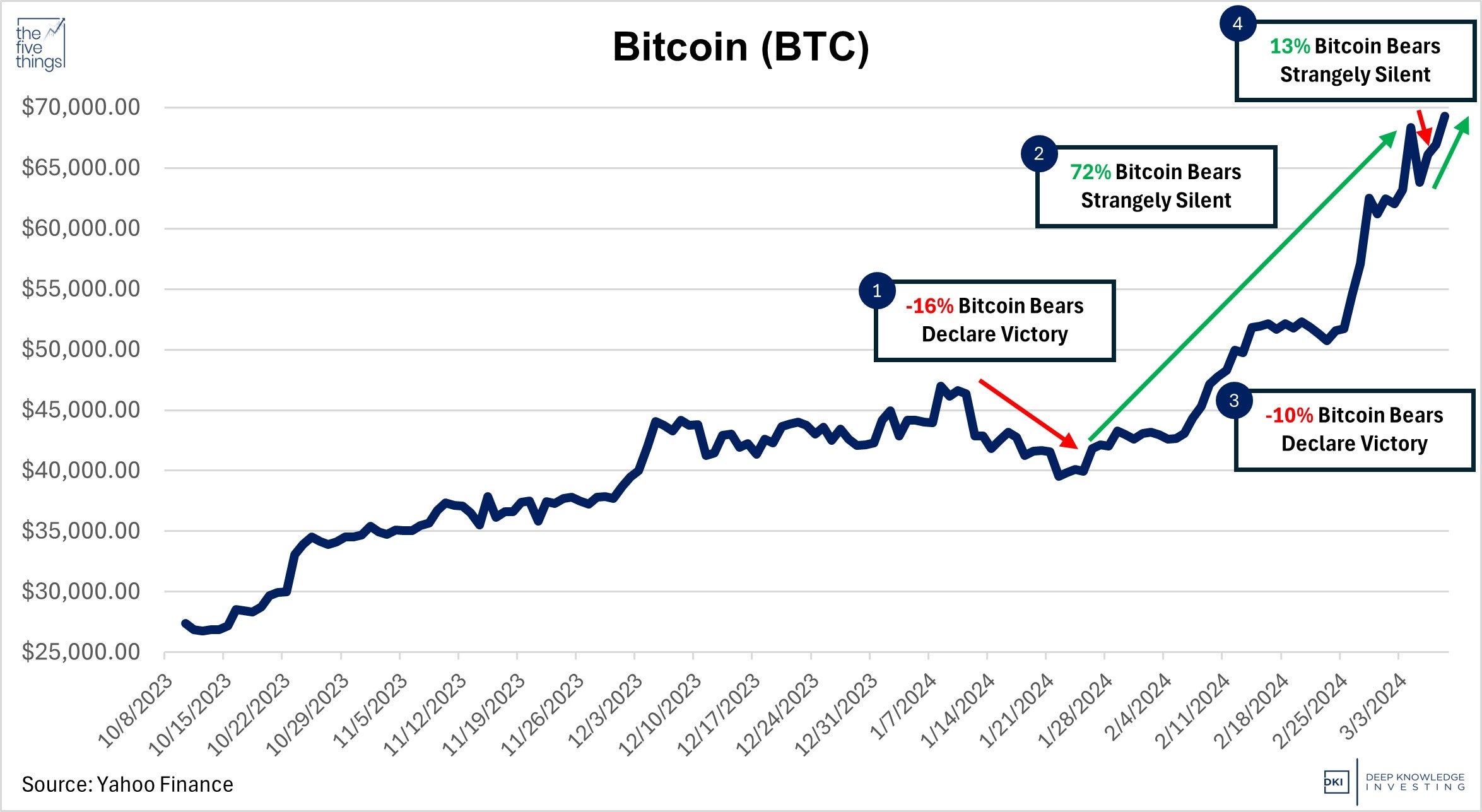

Always a volatile asset, the dollar price of Bitcoin has been fluctuating even more wildly than usual. Last week, we pointed out that the bears loudly declared victory when Bitcoin BTC/USD fell about 10% (16% peak to trough including some short-term intra-day trading), but were strangely silent when it ran up more than 70% in the following weeks. This week, we saw a 10% drawdown bring out the bears crowing on Twitter/X that the apex cryptocurrency is a worthless scam only to quiet down again when Bitcoin recovered those short-term losses and traded just below the all-time record as I write this. Remember, if short-term results make you “right”, then a bigger short-term move in the other direction means you’re “wrong”. People with integrity use one standard to evaluate their decisions. Want my view?

Pretty sure I could predict the dollar price of Bitcoin based on who’s talking on Twitter/X.

DKI Takeaway: I think it’s silly to have a short-term price target on Bitcoin. It’s fine if you do, but then that’s the standard you use to determine if you’re right or wrong. I don’t know what the dollar price of Bitcoin will be in a year, but I do know that the purchasing power of the dollar will decline as Congress continues to run up massive debt approaching $3 trillion a year (for now). That means I’m taking a very long-term view. If Bitcoin falls back to $15k again, I’m not going to panic and would probably buy more just like we did the last time the price fell that much. If and when Bitcoin crosses $100k, I won’t be criticizing the people who didn’t buy any nor will I think it’s too late to get involved then. Bitcoin is a good asset to have a calm long-term view. I know the antics and caustic comments from the “Bitcoin maxis” annoy a lot of people, but in this case, their “keep calm and stack sats” approach is the one that I believe is correct.

-

Gold Hits an All-Time High:

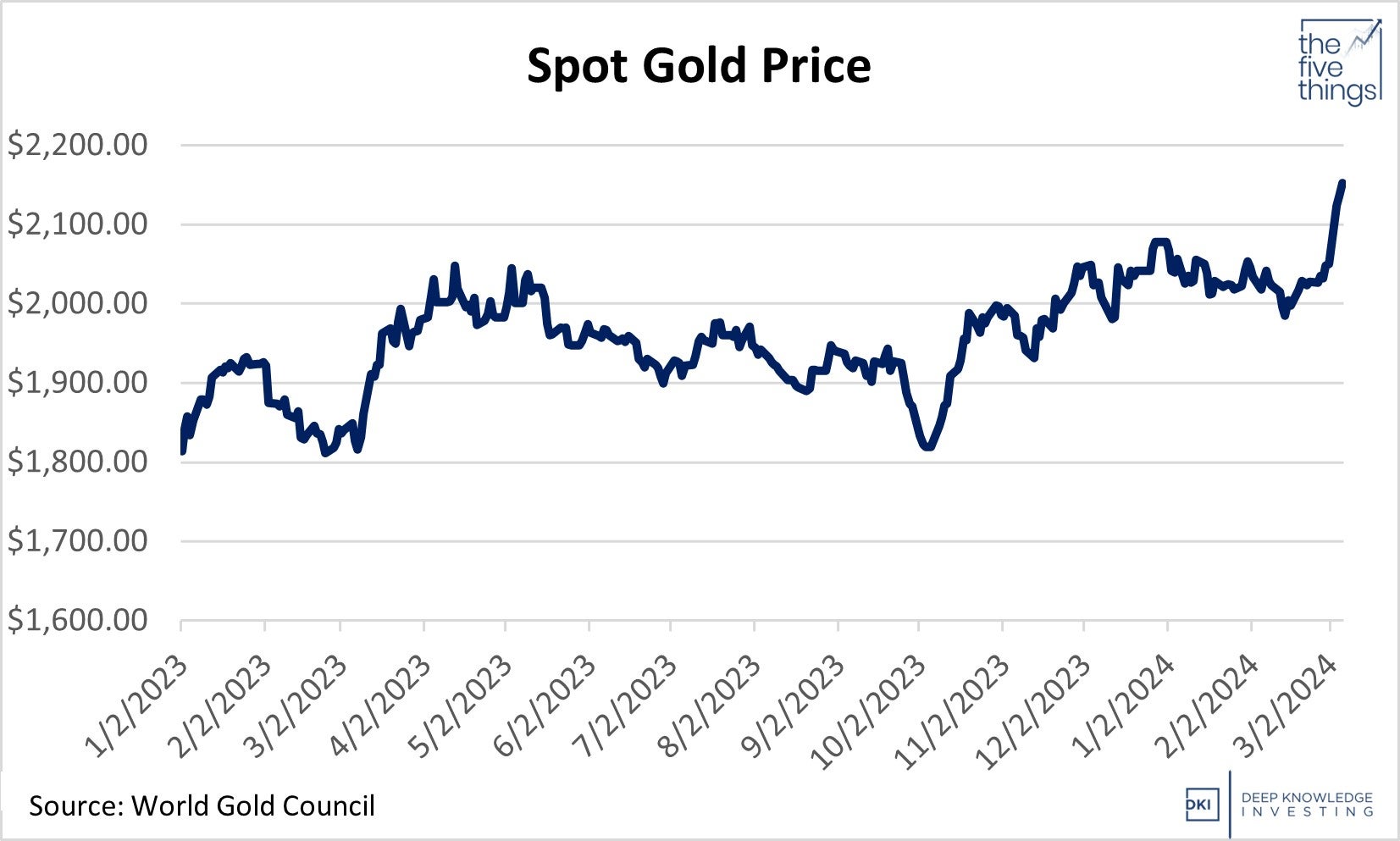

With the higher inflation of the past few years, gold has been a good investment. The chart got more interesting over the past couple of weeks as the metal just hit an all-time high. With higher world-wide inflation as central banks all debase their currencies, gold is the longest-running store of value. Conflict in Ukraine and Israel, attacks in shipping lanes, a credible Chinese threat to take over Taiwan, and a difficult election in the US are all contributing to global uncertainty. Gold is correctly viewed as a safe haven.

Up about 20% in the last year.

DKI Takeaway: Recently, Bitcoin has been a proxy for global liquidity and “risk-on” investing. Gold is the “gold standard” for hedging against inflation, global geopolitical chaos, and government mismanagement. It’s a “risk-off” option. With both hitting all-time highs, that should tell you people are looking for relief from the current market mania of stock indexes hitting all-time highs based on the returns of just 3-4 companies. DKI owns both of these assets as a response to government overspending and the erosion of the dollar’s purchasing power.

-

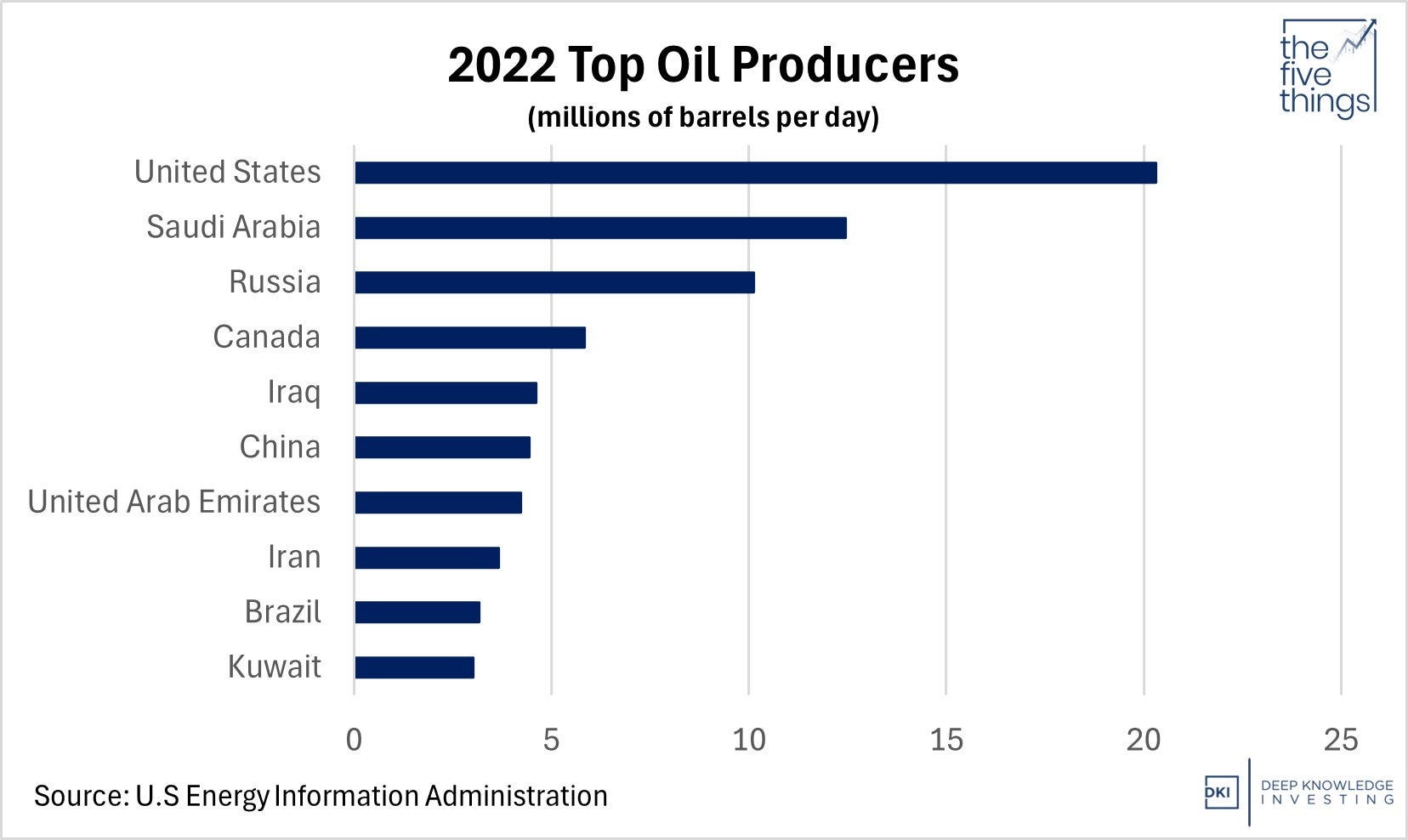

Global Dynamics Influencing Oil Prices:

Saudi Arabia has reaffirmed its commitment to reduce oil supply by 1 million barrels per day. The Saudis have also initiated a rise in oil prices for Asia, their primary market. Russia has followed by reducing supply by 471,000 barrels per day. Meanwhile, Federal Reserve Chair Jerome Powell, testifying before Congress, maintains the expectation of rate decreases later this year. The combination of anticipated rate cuts and Saudi production reductions has led to a modest rise in oil prices with Brent crude back over $80 a barrel.

The Saudis and Russians could produce more, but want higher prices. The US could produce more, but wants less oil usage.

DKI Takeaway: The Saudis and Russians cut oil supply last year and have extended those cuts in an effort to push prices higher. While many still assume Saudia Arabia is the world’s largest oil producer, new technology has put the US in the top spot. In DKI’s conversation with Tracy Shuchart (@chigrl) last month, she said she believes that oil production levels and prices will remain in a range for the rest of the year with no big breakouts to either the upside or downside. Lower interest rates in the future could spur demand for more oil, and DKI maintains the view that we’ll have oil prices that trend “higher for longer” in the coming years.

-

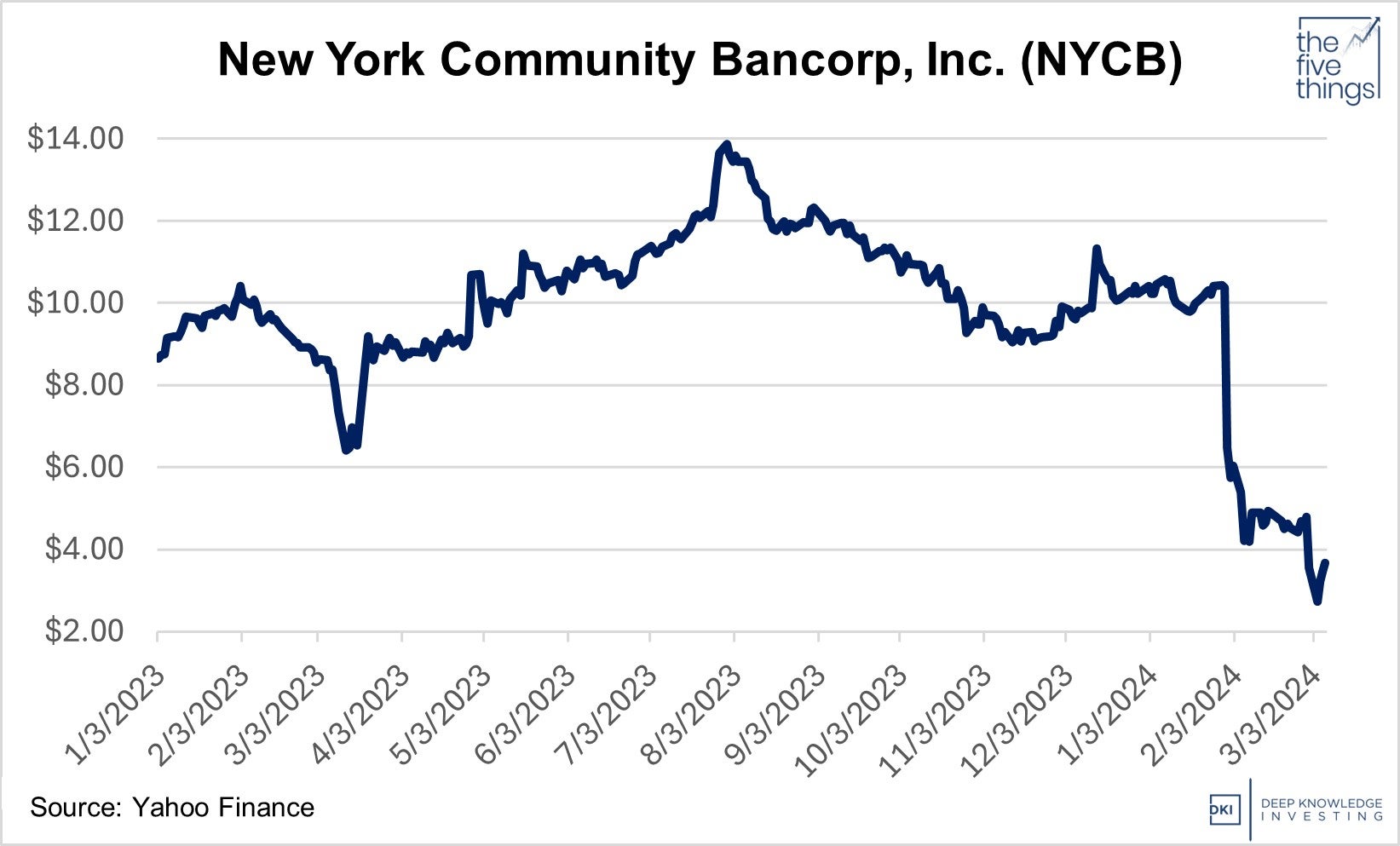

The Banking System Remains Sound:

New York Community Bank is the 35th largest bank in the country. Between bad loans on commercial properties, New York’s destructive rent control laws, and a recent Court decision that is driving away property developers, the market figured out that the bank has an asset-quality problem, and the stock traded below $3. The danger in this situation is depositors spooked by these concerns can withdraw their money instantly causing $NYCB to have to sell bonds. This is the chain of events that caused multiple bank failures last year. A group of investors led by former Treasury Secretary, Steve Mnuchin, invested $1 billion to keep the bank from failing.

Even a billion in extra capital didn’t do much for the stock.

DKI Takeaway: Treasury Secretary, Janet Yellen, never tires of reassuring investors that “the US banking system remains sound”. She keeps saying that despite the fact that multiple banks failed last year, the government bailed out depositors of those failures, and the Federal Reserve continues to provide extraordinary liquidity to banks. Yellen’s constant claim that “all is well” has caused investors to think her words don’t mean what she thinks they mean. Some banking analysts are concerned that when the Fed withdraws the exceptional liquidity, we’ll see more failures. I think this concern is reasonable.

Information contained in this report, and in each of its reports, is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied. DKI makes no representation as to the completeness, timeliness, accuracy or soundness of the information and opinions contained therein or regarding any results that may be obtained from their use. The information and opinions contained in this report and in each of our reports and all other DKI Services shall not obligate DKI to provide updated or similar information in the future, except to the extent it is required by law to do so.

The information we provide in this and in each of our reports, is publicly available. This report and each of our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion in this and in each of our reports are precisely that. Our opinions are subject to change, which DKI may not convey. DKI, affiliates of DKI or its principal or others associated with DKI may have, taken or sold, or may in the future take or sell positions in securities of companies about which we write, without disclosing any such transactions.

None of the information we provide or the opinions we express, including those in this report, or in any of our reports, are advice of any kind, including, without limitation, advice that investment in a company’s securities is prudent or suitable for any investor. In making any investment decision, each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable, based on this or any of its reports, or on any information or opinions DKI expresses or provides for any losses or damages of any kind or nature including, without limitation, costs, liabilities, trading losses, expenses (including, without limitation, attorneys’ fees), direct, indirect, punitive, incidental, special or consequential damages.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.