(Wednesday Market Close) The Federal Open Market Committee announced that it would raise the overnight rate by 75 basis points, in line with market expectations. The committee expects to have further hikes in the future as it remains focused on its goal to get inflation back down to 2% annually.

The Federal Reserve still plans to increase its quantitative tightening to $95 billion in September as it tries to clean up its balance sheet.

In its statement, the Fed expressed concerns over changes in recent indicators showing a softening in spending and production. It noted a slowing in demand for homes, cars, and other items. It also acknowledged that inflation remains “elevated” due to the pandemic, higher food and energy prices amid other market pressures.

In the follow up press conference, Fed Chairman Jerome Powell said that the Fed would remain data- dependent when it comes to further rate hikes but wouldn’t offer any definitive guidance on the future hikes it anticipates. He acknowledged that inflation surprises have happened and could still happen, and the committee is willing to be more aggressive if needed.

At the same time, Mr. Powell also said that the Fed’s June dot plot was still relevant with the overnight rate topping out around 3.5% by the end of the year. If this is the case, then the September hike would likely be around 50 basis points and then 25 basis point hikes would likely occur in November and December.

The CME FedWatch Tool is reflecting this sentiment, giving a high probability of a 50-basispoints increase in September and a possible rise of 25 basis points in November and December. However, these probabilities are likely to change as data come in over the next eight weeks.

Mr. Powell said it was too difficult to determine whether or not the U.S. central bank will need to cut rates next year for a recession. He also said that he didn’t think that the recession had to happen and that the Fed’s goal is to not spark a recession.

Further, he said that he didn’t think the economy was currently in a recession no matter what Thursday’s GDP report will look like because of strength in several areas and the strong labor market.

The markets appeared to interpret the Fed statement and Mr. Powell’s comments as dovish. After some initial volatility, the 2-year Treasury yield fell off its intraday highs and closed back below 3%. The 10-year Treasury yield (TNX) fell five basis points to close at 2.734%. The actions between the 2- and 10-year yields further inverted the yield curve according to the 2s10s ratio.

Stocks were already trading higher ahead of the Fed announcement but briefly sold off before rocketing higher once again after Powell’s press conference. By the close, the Nasdaq ($COMP) finished 4.06% higher, the S&P 500® index (SPX) shot up 2.62% and the Dow Jones Industrial Average ($DJI) rose 1.37%.

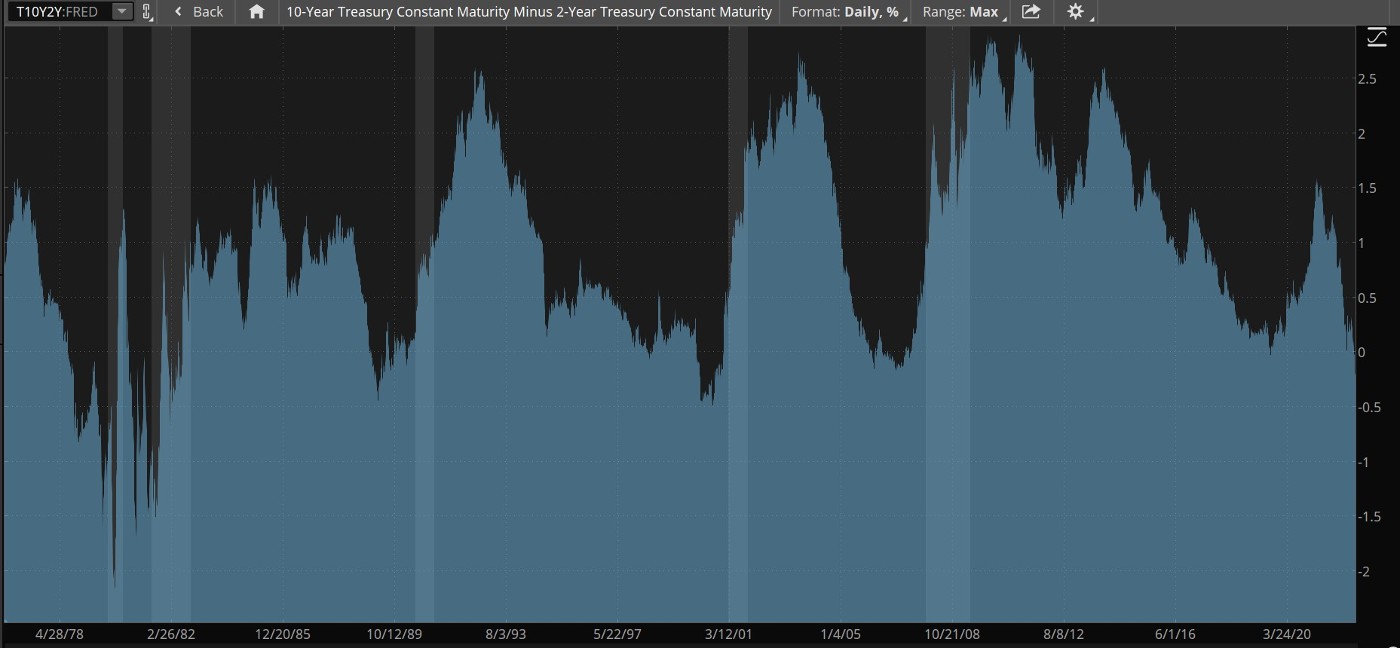

CHART OF THE DAY: GETTING RATIOED. The 10-Year Treasury Constant Maturity Minus 2-Year Treasury Constant Maturity (T10Y2Y:FRED—blue) aka the 2s10s ratio, is inverted when the ratio is below zero. An inverted ratio often precedes a recession (light columns). FRED® is a registered trademark of the Federal Reserve Bank of St. Louis. The Federal Reserve Bank of St. Louis does not sponsor or endorse and is not affiliated with TD Ameritrade. Data Sources: ICE, S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Hitting The Curve

On Tuesday, the spread between the 2s10s ratio inverted to its deepest point since 2006, which was a little more than a year ahead of the Great Recession. The 2s10s ratio is often used as a proxy for the yield curve. An inverted yield curve is considered by many to be a reliable harbinger of a recession.

The yield curve inverts because investors are concerned about the economy and prefer the safety of Treasury bonds despite lower yields and higher maturities. It’s very odd for investors to tie up money for longer period of time for a smaller rate of return unless they feel very strongly that the economy is weak.

Let’s talk through why this trade makes sense. First, Treasuries are considered one of the safest investments.

Second, Treasury payments and the return of principal are backed by the full faith and credit of the U.S. government. No matter what the stock market does, bonds keep making payments.

Third, during a recession, the Fed commonly cuts interest rates, which normally pushes bond prices higher. So, bonds purchased today in anticipation of potential future rate cuts could see enough price appreciation to make up for the lower yields. Longer-term maturities usually experience larger price moves than shorter-term maturities. So, buying 10-year bonds offers greater potential for upward movement.

But there are some risks. The worst-case scenario for Treasury buyers—not counting the U.S. government defaulting—would likely be stagflation. This occurs when the inflation persists even though economic growth is negative or low and unemployment is high. High inflation won’t allow the Fed to lower rates to stimulate the economy, so Treasury investors probably wouldn’t get any price appreciation and would have to settle for collecting the bond payments. They would miss out on the opportunity to get a higher yield with the shorter duration.

Notable Calendar Items

July 28: Gross domestic product (GDP) and earnings from Apple (AAPL), Amazon (AMZN), Mastercard (MA), Intel (INTC), and Caterpillar (CAT)

July 29: PCE Price Index and earnings from Exxon Mobil (XOM), Procter & Gamble (PG), and Chevron (CVX)

Aug 1: ISM Manufacturing PMI and earnings from Activision Blizzard (ATVI), Simon Property (SPG), Devon Energy (DVN), and Aflac (AFL)

Aug 2: JOLTS job openings and earnings Archer Daniels Midland (ADM), Caterpillar (CAT), PayPal (PYPL), Starbucks (SBUX), and Occidental Petroleum (OXY)

Aug 3: ISM Non-Manufacturing PMI and earnings from CVS Health (CVS), Booking (BKNG), Moderna (MRNA), MetLife (MET), and Yum! Brands (YUM)

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Shutterstock

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.