Let's get after it with the vigor and passion of French protesters who took over the Paris Stock Exchange last week.

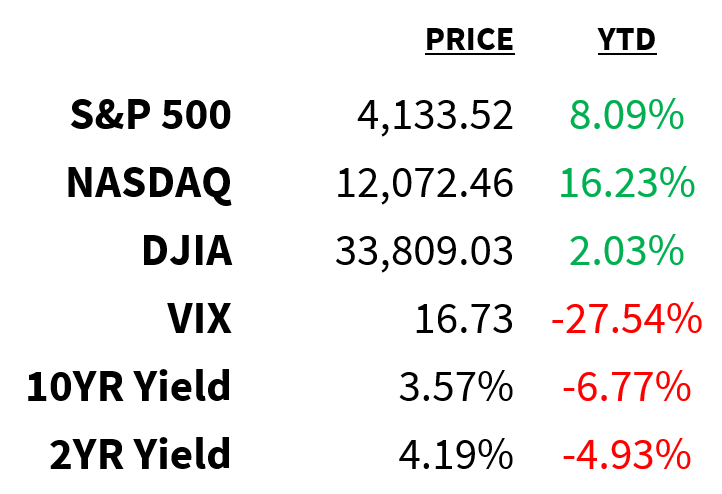

Market

Prices as of 4 pm EST, 4/21/23

Macro

The US House of Representatives will be voting on a spending and debt bill this week.

-

The proposal—put forth last week by GOP Speaker Kevin McCarthy—includes $4.5 trillion in spending cuts as well as a $1.5 trillion increase in the $31.4 debt limit.

-

It’s a familiar game of chicken but stress is showing in markets where the cost of insuring US debt for one year (via credit default swaps) is at its highest on record.

Meanwhile, 87% of respondents in a Bloomberg survey of professional investors expect a Fed funds rate of 3% or lower.

-

The same investors also expect the US dollar’s weakness to continue.

-

In addition to problems at home, many see a rise in the yen or yuan as the main source for the greenback’s decline.

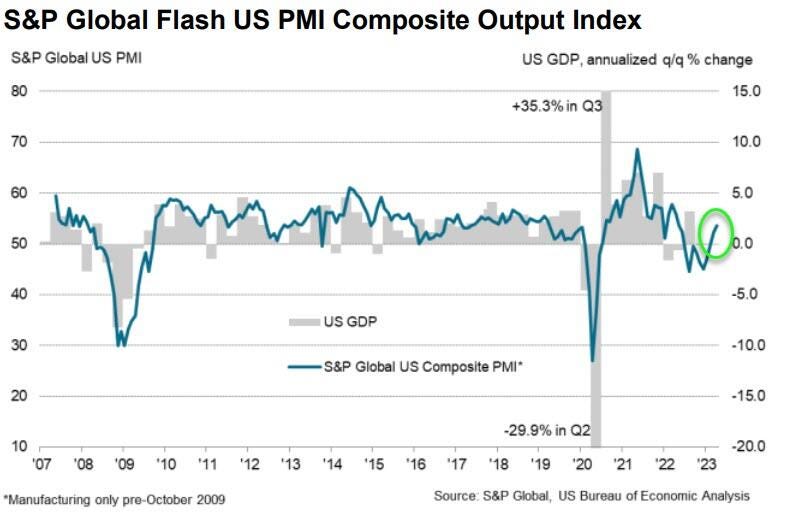

S&P Global’s April Flash US Composite PMI rose to 53.5—the highest reading since May 2022—for its third straight expansionary reading.

-

Services activity growth reached its highest level in a year, increasing well above market expectations to 53.7.

-

Manufacturing PMI beat expectations more modestly, pointing to the first expansion in factory activity in 6 months.

S&P Global

Stocks

The tech sector is off to its best start to a year relative to the S&P 500 since 2009.

-

The strong YTD performance reflects investor optimism that the Fed will soon reverse its aggressive monetary policy stance…but are they too optimistic?

-

Justification for current tech stocks valuations (~25x earnings) would require at least 300bps in rate cuts (or more than 5x what markets are pricing in).

-

The earnings outlook isn’t helping either: analysts predict the sector’s profits will tumble 15% in Q1.

Individual investors in Q1 bought equities and ETFs at a rate third only to the first quarters of 2021 and 2022.

-

Total purchases of single stocks and ETFs totaled $77.7 billion over the first 3 months of the year.

-

Buying peaked in February, however, and has slowed since the collapse of Silicon Valley Bank.

-

Investors are also increasingly preferring ETFs over single stocks, suggesting a lower appetite for risk.

-

According to Vanda Research, the average retail investor’s portfolio is still down ~27% from November 2021.

Hedge funds have never been more bearish on US Treasuries.

-

Leveraged investor net shorts on 10-year Treasury futures have climbed to a record high after increasing for 5 consecutive weeks.

-

Their positioning suggests they don’t anticipate a near-term recession despite higher rates.

Bloomberg

Energy

Weak US economic data and softening gasoline demand pushed down weekly oil prices for the first time in roughly a month last week.

-

Nearly all the gains stemming from OPEC+’s surprise cut earlier this month have been wiped out as the outlook for global demand wanes.

-

Analysts are uncertain crude prices can bounce back without an expansion in refiner margins, which have fallen ~50% from their mid-2022 highs.

Earnings

So far, 18% of the S&P 500 has reported.

-

76% have beaten EPS estimates (above the 5-year average but below the 10-year average)

-

63% have beaten revenue estimates (below the 5-year average and equal to the 10-year average)

-

Blended earnings and revenue growth rates are at -6.2% and 2.1%, respectively.

What we’re watching today:

-

Coca-Cola KO

-

Canadian National Railway CNI

-

Cadence Design CDNS

-

Ameriprise AMP

-

Alexandria Real Estate ARE

-

Brown & Brown BRO

-

Packaging of America PKG

-

Cadence Bank CADE

-

First Republic Bank FRC

Top Headlines

-

Presidential election: More than half of Americans do not want to see a Biden-Trump rematch in 2024.

-

Earnings risk: Vocal Morgan Stanley bear Mike Wilson thinks investors are too optimistic about earnings.

-

Insider optimism: On an individual and company basis, insider buying in March was the highest since May 2022.

-

Outflows: Credit Suisse saw $68.6 billion in outflows during the first quarter.

-

European first: Luxury giant LVMH became the first European company to eclipse $500 billion in market value.

-

Chapter 11: Bed Bath & Beyond has filed for bankruptcy protection and plans to liquidate (unless it finds a last-minute buyer).

-

Ride-sharing: Lyft will cut ~1,200 jobs to lower costs and remain competitive with Uber.

-

Semis: The semiconductor industry’s sharpest slowdown in more than a decade is lasting longer than expected.

Week Ahead

-

Monday: Chicago Fed National Activity Index, Dallas Fed manufacturing

-

Tuesday: Redbook, Case-Shiller Home Price Index, CB Consumer Confidence, new home sales, Richmond Fed manufacturing/services, Dallas Fed services

-

Wednesday: Durable goods, retail & wholesale inventories

-

Thursday: Q1 GDP, initial jobless claims, pending home sales

-

Friday: Personal income & spending, PCE Price Index, Chicago PMI, Michigan Consumer Sentiment

-

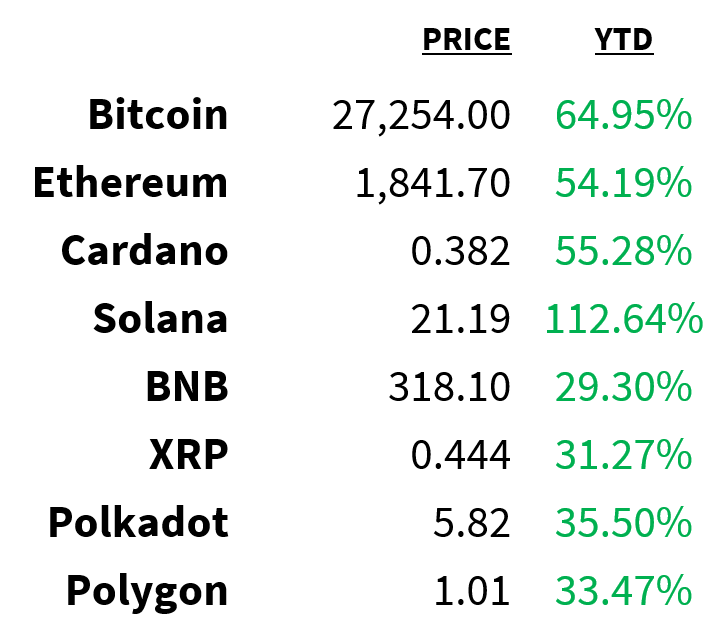

Crypto

Prices as of 4 pm EST, 4/21/23

-

CBDC adoption: Government staff in Changshu, China will be paid in the central bank’s digital currency from June onwards.

-

Gold-backed CBDC: Zimbabwe will introduce a gold-backed digital currency as legal tender.

-

Asset flows: Six straight weeks of inflows into digital asset investment products ended after investors pulled out $30 million last week.

-

Liquidations: Bitcoin’s ~9% drop last week resulted in $650.9 million in long liquidations.

-

Blue chip NFTs: Floor prices for both CryptoPunks and Bored Apes fell well below $100,000 last week for the first time in months.

Deals

-

Software: Shares of Software AG jumped nearly 50% after a takeover offer from private equity firm Silver Lake.

-

Shoring up: PacWest Bancorp is considering the sale of its lender finance division to free up capital and reduce its balance sheet.

-

Fashion: A week after unloading Bonobos, Walmart will sell its plus-size fashion brand Eloquii to FullBeauty Brands.

-

M&A fees: Partner pay at US law firms took a hit in 2022 after a drought in dealmaking.

-

Global IPOs: The global market for new offerings is showing signs of strength after $25 billion worth of IPOs were priced in March.

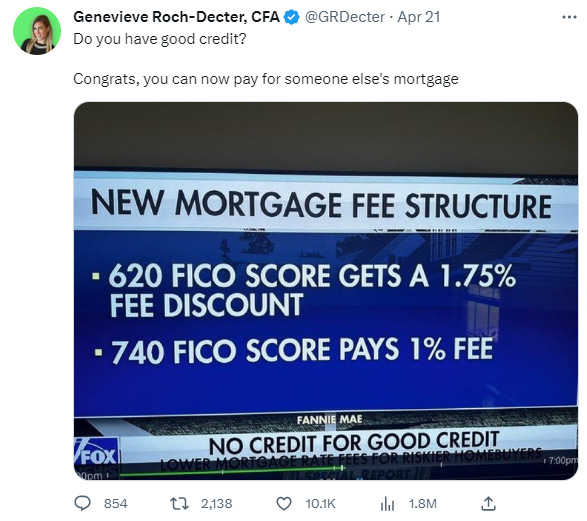

Meme Of The Day

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.