This wasn’t a good week for the “pivot” people and asset gatherers who have been begging the Federal Reserve for lower rates. We got a higher-than-expected CPI and PPI. Making things worse, the short-term monthly numbers have started to accelerate meaning the disinflation story might be dead for now. Retail sales and manufacturing numbers were also a disappointment, but Congressional spending will keep us out of an “official” recession despite a weakening “real” economy as experienced by most Americans. Laks Ganapathi provides a guest “Thing” focused on her concern about the EV business. We explain in more detail the meaning behind the all-time highs in gold and Bitcoin. Finally, we express concern about commercial real estate based on what we’re seeing in the warehousing business.

This week, we’ll address the following topics:

-

The CPI comes in hot. Should we panic about inflation?

-

The PPI comes in hot. Should we panic about inflation?

-

Retail sales come in weak and manufacturing is down. Should we panic about a recession?

-

EV companies already heading for bankruptcy FSR. Guest post by Unicus Research which called this one well in advance.

-

Gold and Bitcoin at/around all-time highs. We do a better job explaining the implication.

-

A decline in warehouse employment is a negative economic signal for commercial real estate.

Nice work this week by DKI Intern, Andrew Brown, who continues to contribute graphs and ideas for the weekly 5 Things. In under two months, he’s become a real contributor which we’re happy (but not surprised) to see.

Ready for a new week of horrifying economic data? Let’s dive in:

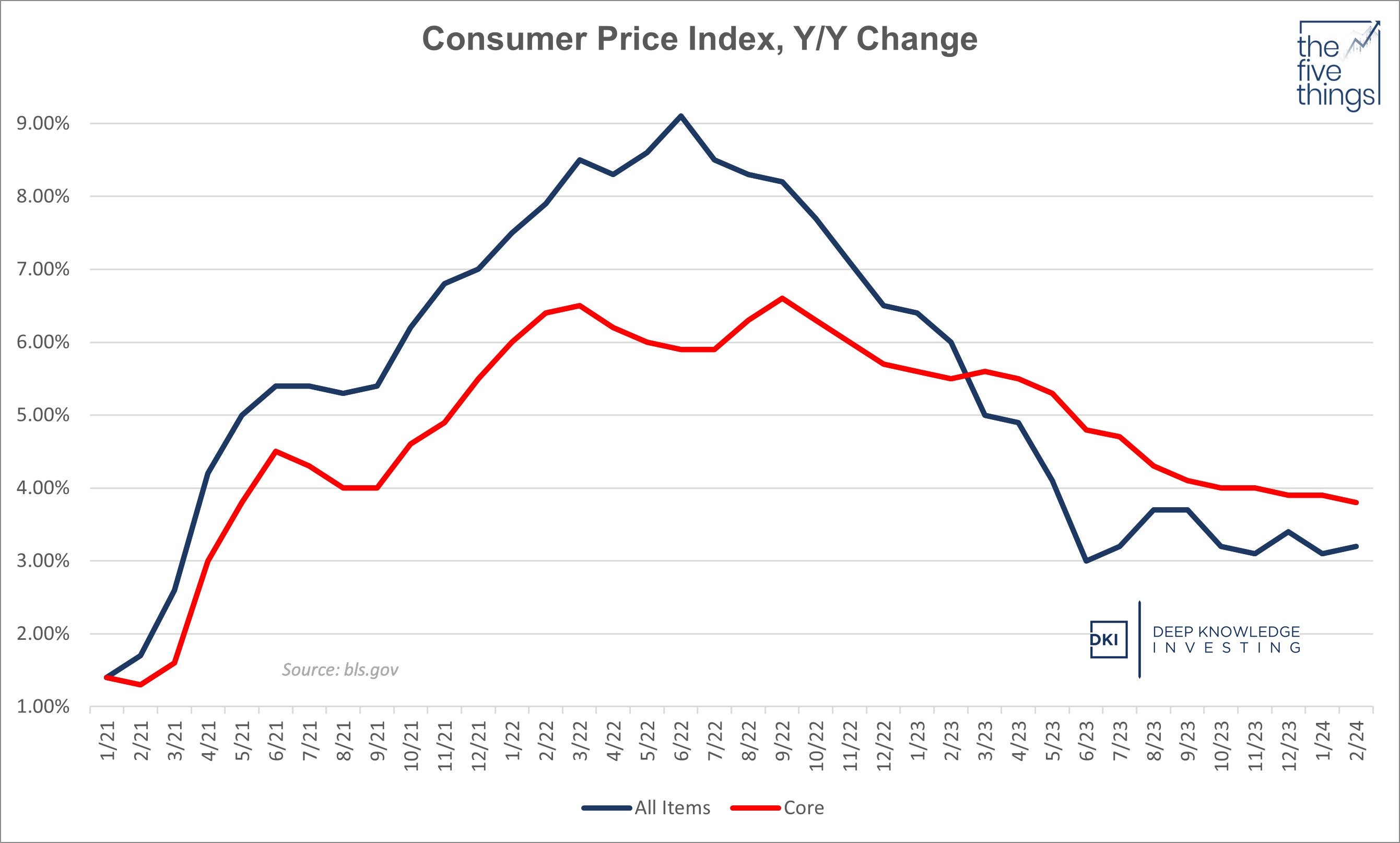

- The CPI Comes in Hot:

This week we got the February CPI (Consumer Price Index) which came in at 3.2% vs last year and 0.4% vs last month. Both of these are 0.1% above last month and above expectations of 3.1% for the year. The Core number, which excludes food and energy, was up 3.8% for the year and up 0.4% vs last month. This was also above expectations and almost double the 2% target largely due to continued high services inflation.

The disinflation story has faded for now.

DKI Takeaway: Last year, people were excited about disinflation and using that as the reason to scream that the Federal Reserve should pivot to lower interest rates. Disinflation is not lower prices; but rather, a slowing in the inflationary increase in prices. It’s a change in the rate of change. For those of you without fond memories of your high school calculus class, it means we still have inflation. A quick look at the chart above makes it clear that the Fed is having trouble making further progress. The obvious conclusion: “higher for longer”.

-

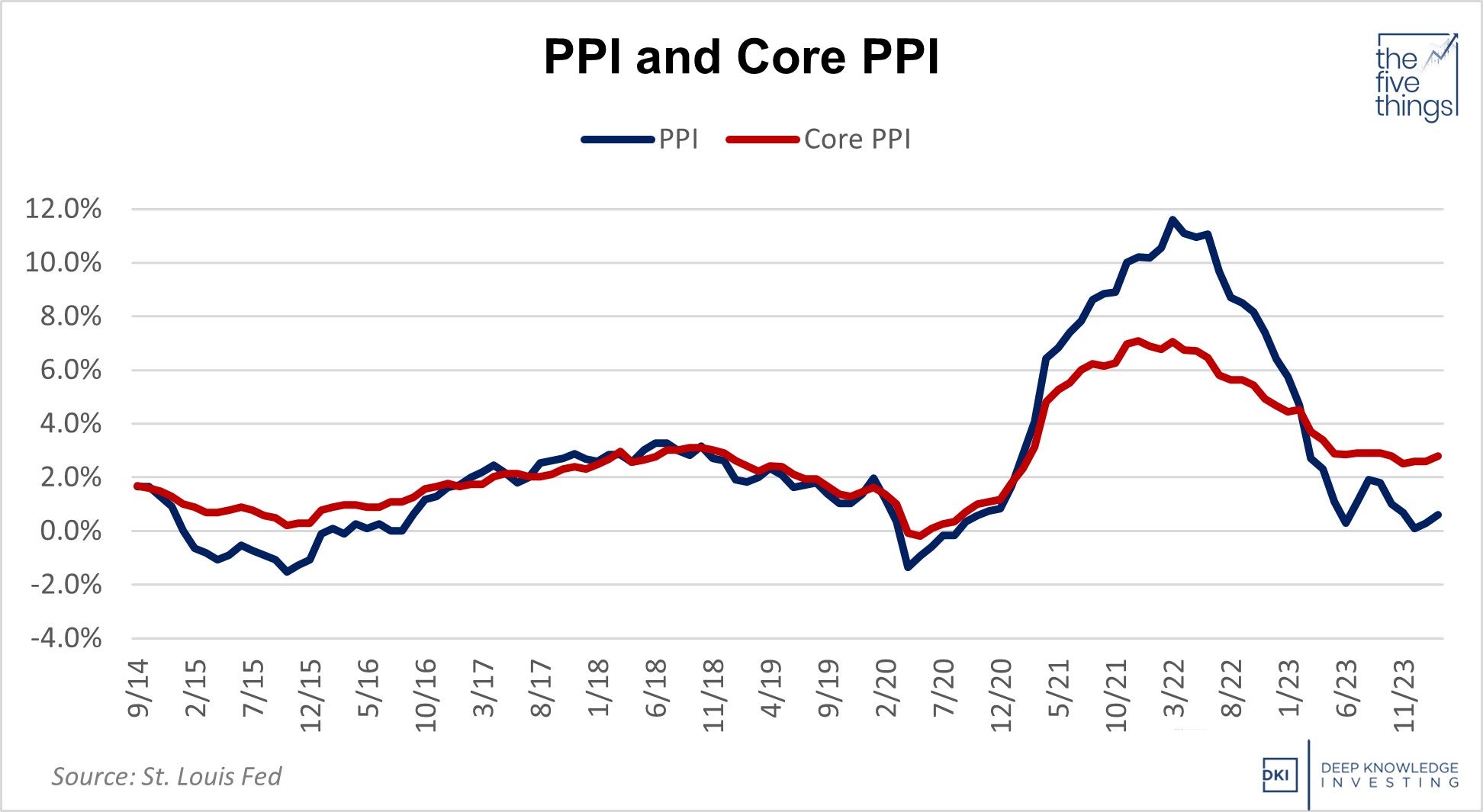

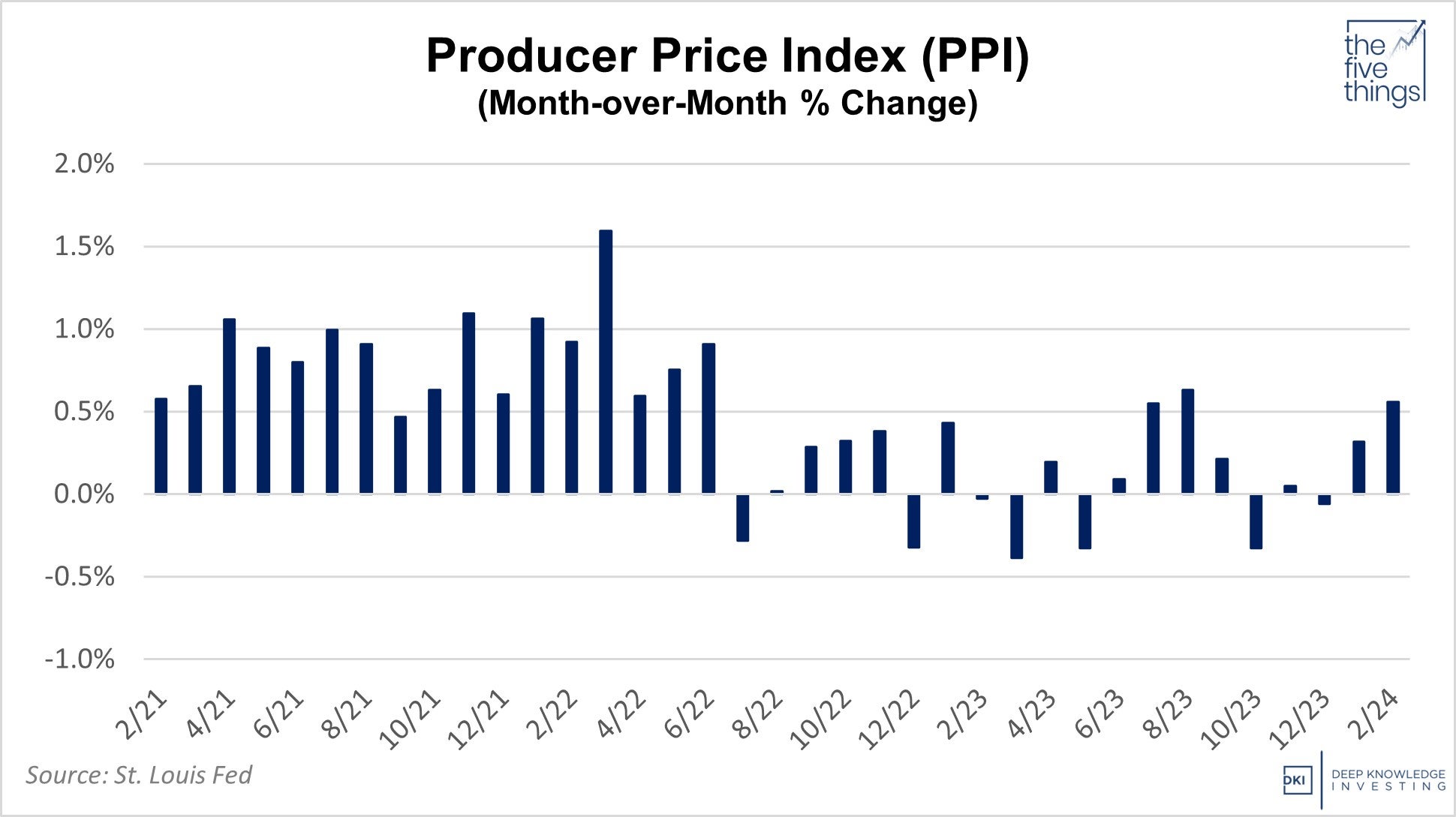

The PPI Comes in Hot:

The February producer price index (PPI) came in at 1.6% vs last year which is a pretty good number. The problem is the monthly increase was 0.6% which was double the expected 0.3% rise. A 0.6% increase might not seem like much, but it annualizes to 7.4%. If this continues, we’re about to see an acceleration of producer price inflation. As usual, the Core PPI remains above the all-items version of the index.

Like the CPI, the disinflation story is stalling.

That’s a big acceleration at the end.

DKI Takeaway: The reason the PPI matters is it is intended to be a forward-looking measure of inflation. As producers and manufacturers experience increases in the prices of their raw materials and labor costs, we can expect those increases to find their way into consumer prices a few quarters in the future. Because the PPI has been lower than the CPI, many people expected we’d see a reduction in consumer inflation in the coming months. The recent re-acceleration of producer prices will cause that narrative to shift. The conclusion for now: “higher for longer” (but you probably guessed that one already).

-

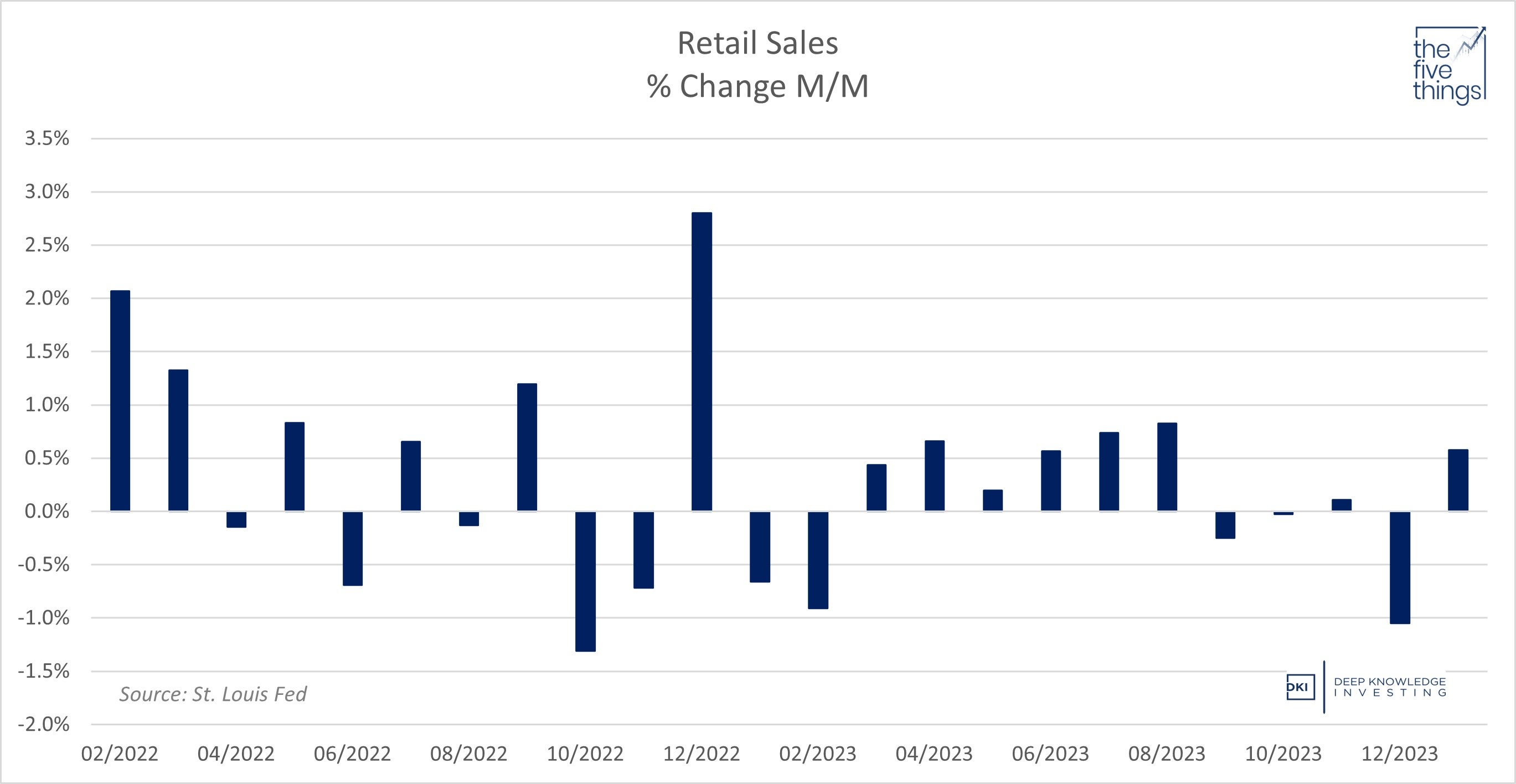

Retail Sales Up but Below Expectations. Manufacturing Down:

Retail sales had been negative in three of the past four months which is remarkable given the persistent high inflation we’ve had. This month, we saw a 0.6% sales increase vs last month which was well-above the prior month’s drop, but also below expectations. After months of weakness, sales of goods have started to strengthen again. Of greater concern, much of the gains in retail sales came from increases in gas prices. Tied to months of weak consumer data, the Empire State Manufacturing Survey fell 19 points to negative 21. That’s a big slowdown.

Much of the increase at the end is due to higher gas prices.

DKI Takeaway: We’re seeing increases in the rate of monthly inflation, higher consumer spending due to higher prices, and a slowdown in some of the manufacturing indexes. This is causing some people to become concerned about stagflation (an economic slowdown combined with inflation). Given that huge Congressional overspending adds to nominal GDP, I think we’re unlikely to see an official recession anytime soon. However, it’s also unlikely the Fed cuts interest rates on data that looks like what we saw this week. The market is already starting to push back expectations for the June rate cut.

-

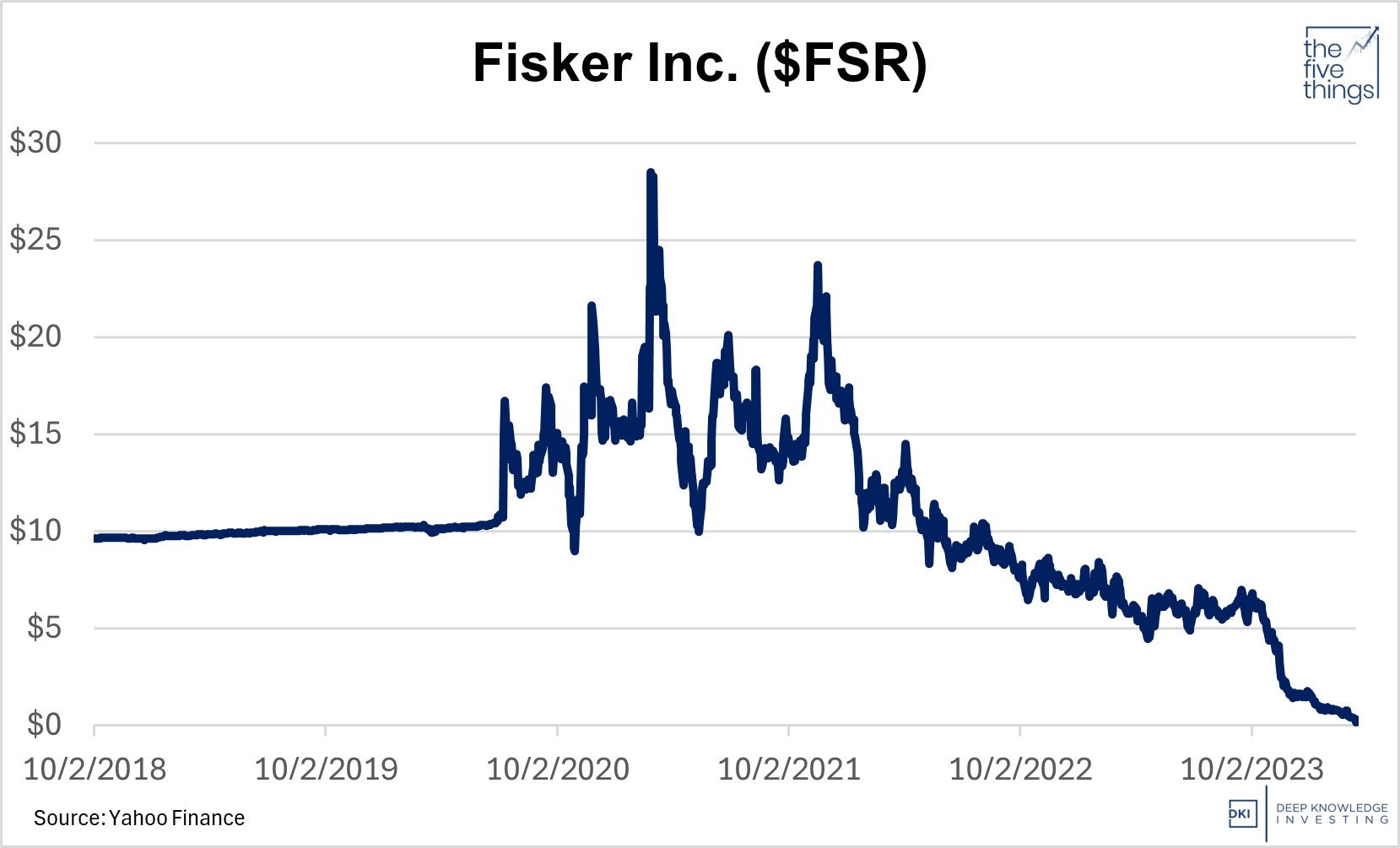

Fisker ($FSR) Heading for Zero. What about the EV Sector?:

Unicus Research notes that EV maker, Fisker is heading towards its second bankruptcy. The company is an early rival to Tesla TSLA and Henrik Fisker helped design the Model S. In October, 2020, $FSR merged with a SPAC and went public. The company has had reliability issues with software, power loss, braking problems, and self-opening hoods. The National Highway Traffic Safety Administration is investigating. Consumers have filed lawsuits regarding lack of warranty support and the stock is heading towards zero.

This one doesn’t require commentary.

DKI Takeaway: Uncius was early and right about problems in the EV sector. The manufacturers are burning billions of dollars to make the world “green”. The cars suffer from scalability and reliability problems, negative cash flow, and lack of infrastructure. Of the 43 EV companies that went public between 2020 and 2022, five have already filed for bankruptcy or been acquired. At least 18 of them are at risk of running out of cash this year. Government subsidies come without due diligence and consumers are being pressured and incentivized to buy these vehicles. Unicus notes that EVs are expensive, environmentally unfriendly, come with liability and safety issues for the users, are not sustainable, and current sales are based on marketing pressure and gimmicks. Plus, what happens to consumers who buy EVs only to find out that no ongoing concern has an obligation to provide crucial software updates?

-

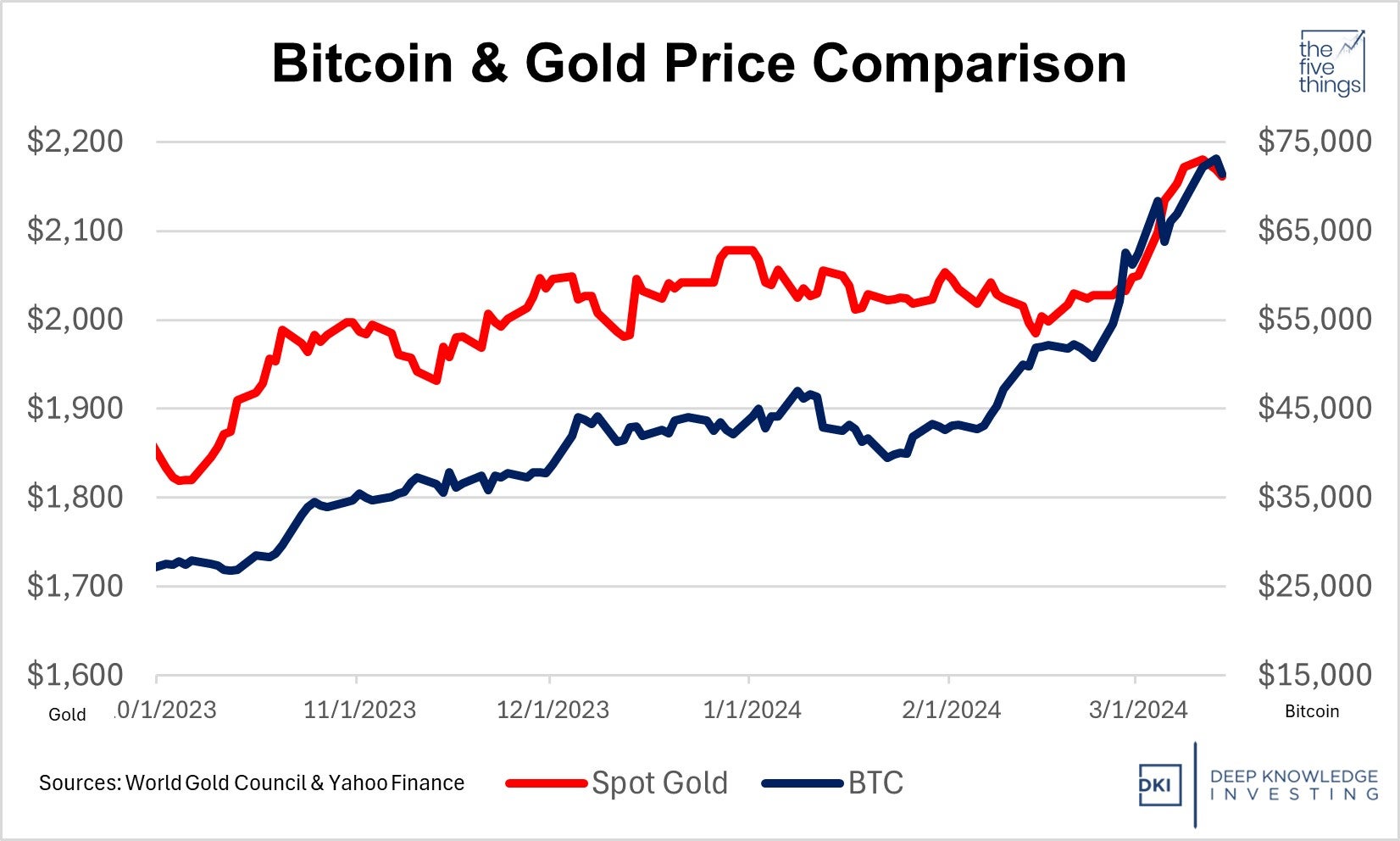

Gold and Bitcoin Around All-Time Highs – What’s it Mean:

Within the last week, both gold and Bitcoin BTC/USD have hit all-time highs. We noted this last week, and got some questions about the topic. Bitcoin has been trading as a proxy for global liquidity and has been a high-beta risk-on asset. That means it tends to go up with the market and with increases in liquidity. Gold has been one of the best risk-off assets for thousands of years. That means when people are worried about their local fiat currency or geopolitical uncertainty, they turn to gold.

Bitcoin is up much more as a percentage, but these are both big runs.

DKI Takeaway: I think we’re seeing two things happening here. Bitcoin is rising partly due to the declining purchasing power of fiat currency, partly due to additional demand related to the new ETFs, and partly in advance of next month’s halving which will further limit flows from mining. Gold is rising partly due to the declining purchasing power of debased fiat, partly due to geopolitical uncertainty, partly due to the desire of much of the world to find an alternative to the dollar, and partly as a response to stock market indexes that are hitting all-time highs on no breadth. Like last year, almost all of this year’s stock market gains have come in only a few stocks. As governments overspend and finance that spending with currency creation, I think both of these assets will see increases in their price in dollars.

-

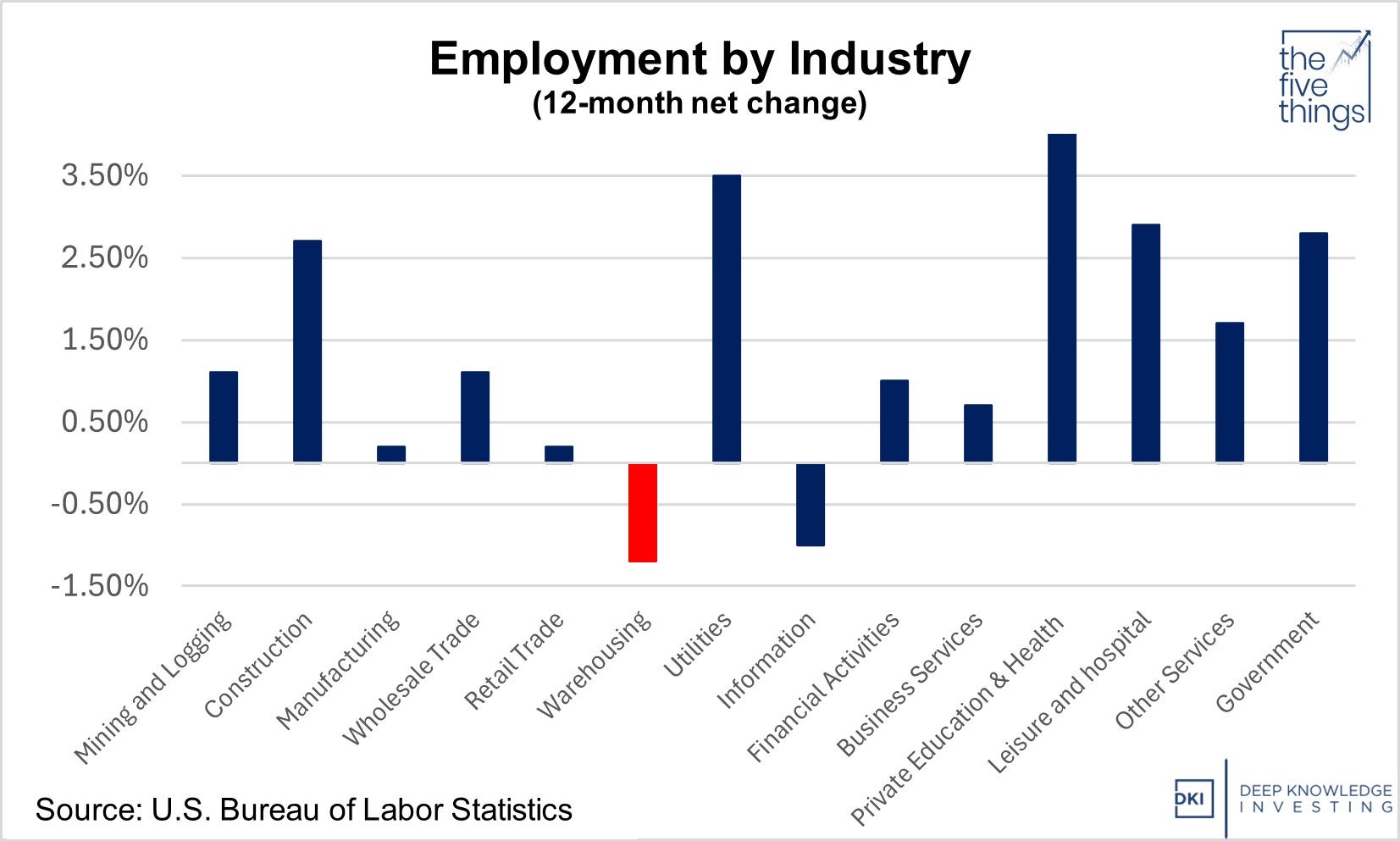

Warehouses Indicating a Problem with Commercial Real Estate:

Online shopping has been taking share from physical retail for the last two decades. Pandemic lockdowns caused this trend to accelerate creating new demand for warehouses to speed distribution to your home. However, while employment across most sectors of the economy has grown, the warehousing sector has seen a decline in employment. Some of that is due to automation, but there are macro issues as well. National vacancy rates for industrial real estate are 5%. In major metropolitan areas, that’s as high as 8%.

I’m pretty sure you can find the big outlier here.

DKI Takeaway: DKI Intern, Andrew Brown, located a business with a new 500,000 sq. ft. distribution warehouse that was completed 6 months ago and is currently unoccupied. This is despite strong growth in North Carolina. We note that the government continues to claim robust economic growth which is largely based on government spending. Under the surface, we have questions regarding the strength of the real economy. Inflation is still too high in our grocery stores, office space remains unoccupied as return-to-work is still unpopular, and we’re starting to see evidence of a waning need for distribution warehouses. None of this is a positive for property developers and regional banks.

Information contained in this report, and in each of its reports, is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied. DKI makes no representation as to the completeness, timeliness, accuracy or soundness of the information and opinions contained therein or regarding any results that may be obtained from their use. The information and opinions contained in this report and in each of our reports and all other DKI Services shall not obligate DKI to provide updated or similar information in the future, except to the extent it is required by law to do so.

The information we provide in this and in each of our reports, is publicly available. This report and each of our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion in this and in each of our reports are precisely that. Our opinions are subject to change, which DKI may not convey. DKI, affiliates of DKI or its principal or others associated with DKI may have, taken or sold, or may in the future take or sell positions in securities of companies about which we write, without disclosing any such transactions.

None of the information we provide or the opinions we express, including those in this report, or in any of our reports, are advice of any kind, including, without limitation, advice that investment in a company’s securities is prudent or suitable for any investor. In making any investment decision, each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable, based on this or any of its reports, or on any information or opinions DKI expresses or provides for any losses or damages of any kind or nature including, without limitation, costs, liabilities, trading losses, expenses (including, without limitation, attorneys’ fees), direct, indirect, punitive, incidental, special or consequential damages.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.