Zinger Key Points

- Rosenblatt maintains a Buy rating for Arm Holdings, driven by strong licensing interest and royalty growth.

- Analyst Hans Mosesmann highlights Arm's potential in AI and datacenter markets.

- Pelosi’s latest AI pick skyrocketed 169% in just one month. Click here to discover the next stock our government trade tracker is spotlighting—before it takes off.

Rosenblatt analyst Hans Mosesmann reiterated a Buy rating on Arm Holdings plc ARM with a price target of $180.

The analyst revised his views on Arm in response to recent investor inquiries regarding its performance compared to the industry over the past three months.

Mosesmann factored in concerns about valuation, royalty ASP trajectory, licensing irregularities, exposure to wireless, and AI involvement.

Also Read: Arm Holdings Gears Up for AI Foray with New Chip Division Launching Next Year

In the past few weeks, his checks have shown significant and ongoing interest in licensing the company’s broad portfolio.

He also noted an increase in Arm Total Access (ATA) to 31 from 3 in the fourth quarter of fiscal 2021.

Customers are moving faster, and their in-house expertise is insufficient for rapid deployment into the next generation of silicon, as per Mosesmann. With licensing giving the analyst a strong sense of mid-to-long-term growth for Arm, royalties are the critical driver to watch in 2024 and 2025.

The analyst said the transition from v8 to v9 is having a significant impact, especially on mobile, with a 2x increase in ASP. Additionally, Arm datacenter is gaining momentum with Alphabet Inc GOOG GOOGL Google Axion, Microsoft Corp MSFT Cobalt, Nvidia Corp NVDA GB200, all indicating potential market share gains over the next few years.

In the PC world, Windows on Arm (WoA) is now ready for AI applications with Qualcomm Inc’s QCOM X Elite and X Plus CPUs, Mosesmann said. These CPUs are impressive in a space that has been dominated by the x86 architecture for decades.

The analyst expects royalties to exceed 70% of license sales in the next few years, compared to approximately 55% in the most recent quarter. Regarding AI, Arm is foundational to all of computing going forward, he added.

Mosesmann stated that Nvidia’s GB200 is only possible with the NVLink-connected Arm-based Grace CPU. Intel Corp’s INTC foundry strategy only works with the multigenerational collaboration with Arm.

Along with Nvidia, ARM is his top secular idea.

Mosesmann projected fiscal first quarter 2025 revenue and EPS of $900 million and 34 cents.

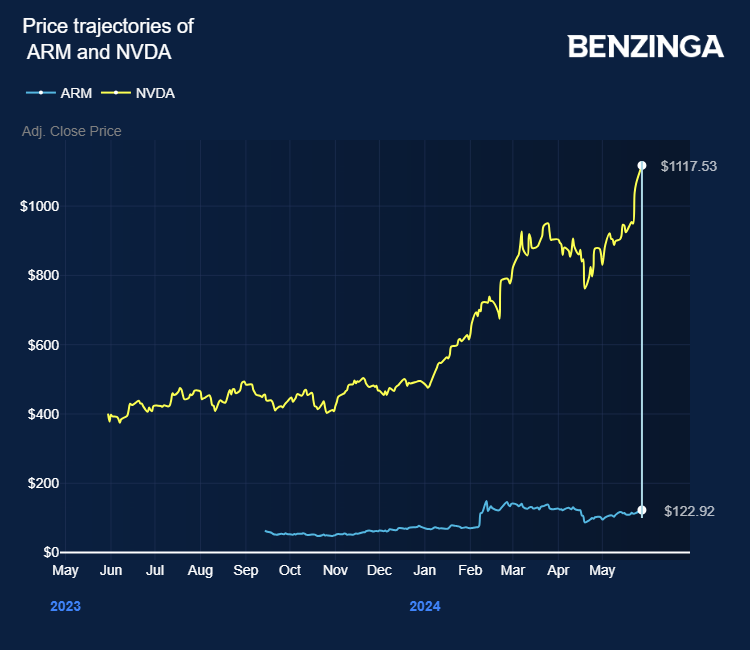

ARM Price Action: Arm shares traded higher by 6.68% at $122.30 at the last check Tuesday.

Now Read: Arm Holdings Poised To Challenge Qualcomm, Intel, AMD In AI, Analysts Predict Growth In Chip Design

Image: Shutterstock

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

date | ticker | name | Price Target | Upside/Downside | Recommendation | Firm |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.