The Home Depot Inc. HD looks well-poised for long-term growth on its ongoing investments to strengthen its business despite the recent softness in demand trends across the home improvement industry. Home Depot is witnessing significant benefits from the execution of its strategic initiatives and commitment to investing in the business to deliver the best interconnected shopping experience, capture wallet-share with the Pro, and expand its store footprint.

The company is on track with the execution of the "One Home Depot" investment plan, which focuses on expanding supply-chain facilities, technology investments and enhancement to the digital experience. The interconnected retail strategy and underlying technology infrastructure have helped consistently boost web traffic for the past few quarters.

Home Depot's Pro segment has been a key growth driver, with the Pro segment witnessing robust sales growth for the past several quarters. In first-quarter fiscal 2024, the company's Pro and DIY sales were almost in line with one another. Although lower than the year-ago quarter, the company noted that Pro backlogs continued to be healthy and elevated relative to historic trends.

Recent external data point suggests that the types of projects in these backlogs are changing from large-scale remodels to smaller projects. HD continues to invest in Pro capabilities like enhanced fulfillment, more personalized online experience, and other business management tools to drive deeper engagement with Pro customers.

By the end of fiscal 2024, the company expects to equip 17 of its top Pro markets with new fulfillment options, localized product assortment and expanded sales force, along with enhanced digital capabilities with trade credit and order management in pilot for development.

Enhanced search capabilities, improved Pro site experience and robust fulfillment capabilities have been driving increased online conversions. Sales leveraging HD's digital platforms rose 3.3% year over year in first-quarter fiscal 2024. The company's strategy of providing an interconnected experience is resonating well with customers, as around 50% of the online orders were fulfilled through stores in the fiscal first quarter.

What's Holding Back the Stock?

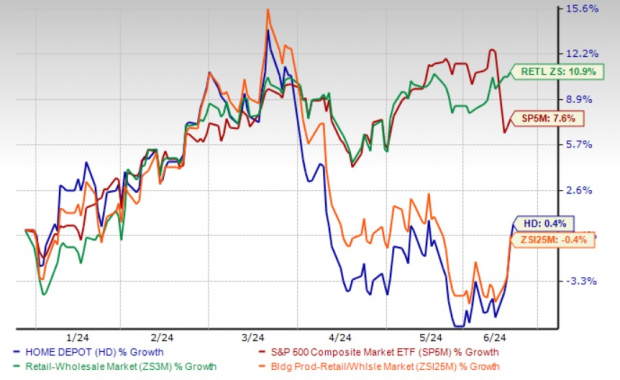

Shares of the Zacks Rank #3 (Hold) company have gained 0.4% against the industry's 0.4% decline in the year-to-date period. Meanwhile, HD compared unfavorably with the Retail-Wholesale sector's growth of 10.9% and the S&P 500's improvement of 7.6% year to date. The stock's downside can be mainly attributed to pressures related to broad-based pressures across the business, driven by softened demand.

Image Source: Zacks Investment Research

The company has been witnessing softness in demand for certain big-ticket, discretionary categories. This led to soft first-quarter fiscal 2024 results, with the top and bottom lines declining year over year. Results for the quarter were mainly impacted by a delayed start to the spring season, as well as continued demand softness for certain larger discretionary projects. However, the company benefited from its store readiness and product assortments in stores and online.

Home Depot anticipates the high interest rate environment at the beginning of 2024 versus last year to persist and pressurize the demand for larger projects. The company expects sales to increase 1% year over year for fiscal 2024, including $2.3 billion of sales contribution from the 53rd week.

HD estimates the gross margin for fiscal 2024 to be 33.9%, indicating a 50-bps year-over-year expansion. The operating margin is expected to be 14.1%. The company estimates earnings per share to increase 1% year over year for fiscal 2024. It expects the 53rd week to contribute 30 cents per share to earnings in fiscal 2024.

Key Picks

Some better-ranked stocks are Abercrombie & Fitch ANF, The Gap Inc. GPS and Stitch Fix SFIX.

Abercrombie, a specialty retailer of premium, high-quality casual apparel for men, women and kids, currently flaunts a Zacks Rank #1 (Strong Buy). ANF has a trailing four-quarter earnings surprise of 210.3%, on average.

The Zacks Consensus Estimate for ANF's current financial-year sales and earnings indicates growth of 10.5% and 47.5%, respectively, from the year-ago reported numbers.

Gap is a premier international specialty retailer offering a diverse range of clothing, accessories and personal care products. It sports a Zacks Rank #1 at present.

The Zacks Consensus Estimate for Gap's current financial-year sales and earnings indicates growth of 0.1% and 17.5%, respectively, from the year-ago reported numbers. GPS has a trailing four-quarter earnings surprise of 202.7%, on average.

Stitch Fix is a leading online personal styling service. It currently carries a Zacks Rank #2 (Buy). SFIX has a trailing four-quarter average earnings surprise of 14.5%.

The Zacks Consensus Estimate for Stitch Fix's current fiscal-year earnings indicates growth of 20% from the previous year's reported figure.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

date | ticker | name | Price Target | Upside/Downside | Recommendation | Firm |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.