First American Financial FAF is poised to grow, given the increased demand among millennials for first-time home purchases. The expansion of its valuation and data businesses, as well as strength in commercial business and technological upgrades, is expected. These, along with solid growth projections, make the Zacks rank #3 (Hold) stock worth retaining.

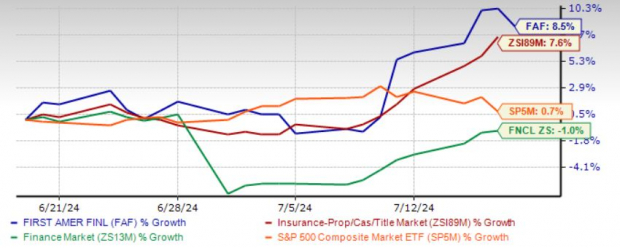

An Outperformer

Shares have gained 8.5% in the past month, outperforming the industry's growth of 7.6%, the Finance sector's decline of 1% and the Zacks S&P 500 composite's increase of 0.7%.

Image Source: Zacks Investment Research

Optimistic Growth Projection

The Zacks Consensus Estimate for 2024 earnings is pegged at $3.83, indicating an increase of 0.8% on 4.7% higher revenues of $6.3 billion. The consensus estimate for 2025 earnings is pegged at $5.12, indicating an increase of 33.8% on 10.2% higher revenues of $6.9 billion.

We expect 2026 EPS to witness a three-year CAGR of 11.3%.

Return on Equity

Return on equity (ROE) is a measure of profitability, reflecting how efficiently a company is utilizing its shareholders' funds. FAF's trailing 12-month ROE of 8.2% outperformed the industry average of 7.8%.

Growth Drivers

An increased demand for first-time home purchases among millennials continues to drive results at First American. It expects housing demand, improving economy and labor markets to drive home price appreciation. Thus, banking on growing leadership in title data, courtesy of proprietary data extraction, sturdy distribution relationships, prudent underwriting and continued investments in technology, FAF remains well poised for long-term growth.

Growing direct premiums, escrow fees and title agent premiums should continue to drive the top line. We expect the 2026 top line to increase at a three-year CAGR of 8.2%.

Strategic initiatives to strengthen its product offerings, intensify the company's focus on its core business and expand FAF's valuation and data businesses bode well. Also, the expansion of title plant assets and the upgrade of technology solutions drive increased efficiency.

Impressive Dividend History and Share Buyback Plans

First American has a solid track record of dividend increase, with the metric witnessing an eight-year (2016-2024) CAGR of 8.2%. FAF's dividend yield of 3.9% compares positively with the industry average of 0.3%.

The company also engaged in share buyback and had $210.4 million remaining under its authorization as of Mar 31, 2024.

Risks

Despite the upside potential, there are a few factors that investors should keep an eye on. A challenging real estate and mortgage industry weigh on First American. Transaction volumes suffer due to higher mortgage rates and slow inventory growth. A tough mortgage origination market is a concern.

Also, as the Fed intends to lower rates, the company estimates that for each 25-basis point decline in the Fed funds rate, the annualized investment income will decline $15 million. But the ultimate amount will fluctuate depending on the level of cash and escrow balances.

First American's debt levels have been increasing in the past few years, with the debt-to-capital ratio deteriorating. Its times interest earned compares unfavorably with the industry average.

Stocks to Consider

Some top-ranked stocks from the insurance industry are RLI Corporation RLI, Palomar Holdings PLMR and ProAssurance Corporation PRA. Each stock presently sports a Zacks Rank #1 (Strong Buy).

RLI Corporation's earnings surpassed estimates in three of the last four quarters while missing in one, the average beat being 132.39%. Year to date, shares of RLI have gained 8.2%.

The Zacks Consensus Estimate for RLI's 2024 and 2025 earnings implies 18.2% and 4.1% year-over-year growth, respectively.

Palomar's earnings surpassed estimates in each of the last four quarters, the average earnings surprise being 15.10%. Year to date, PLMR's stock has surged 65.8%.

The Zacks Consensus Estimate for PLMR's 2024 and 2025 earnings indicates 26.3% and 18.5% year-over-year growth, respectively.

ProAssurance earnings surpassed estimates in two of the last four quarters and missed in the other two. Year to date, PRA's stock has lost 12.4%.

The Zacks Consensus Estimate for PRA's 2024 and 2025 earnings implies 371.4% and 72.6% year-over-year growth, respectively.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

date | ticker | name | Price Target | Upside/Downside | Recommendation | Firm |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.