After Tesla Inc TSLA and several other major companies delivered on earnings, investors appeared less hopeful about Congress and the White House delivering on stimulus. Stocks have a red tilt early Thursday, continuing their pendulum swing back and forth as each new tidbit of news from Washington hits Wall Street.

The stimulus continues to be talked about, but, like the election itself, people are at a point where they want it to be over. Like in every other aspect of life, we’re seeing the sausage get made, and sausage-making is an ugly process. If nothing gets done in the final days before the election, it seems unlikely it would happen in a lame-duck Congress.

A jolt of positive news did emerge from Washington this morning as weekly jobless claims fell to 787,000, the lowest since the crisis hit and way below analysts’ estimates for 860,000. The previous week’s figure was also cut to 842,000 from 898,000. One week of data shouldn’t be looked at in isolation, and even today’s figure is well over twice the normal from before the pandemic. It will be interesting to see if next week can follow this one up with more progress.

Over on earnings row, two old stalwarts, AT&T Inc. T and Coca-Cola Co KO, beat analysts’ bottom-line estimates this morning. Shares of both marched ahead in pre-market trading, though neither has recovered to where they were before the pandemic hit. The 3% gain in T so far today is massive for that stock. Intel Corporation INTC reports after today’s close, giving investors a look at the chip sector.

Diving deeper into the bottle with KO, revenue is down but that’s what you’d expect if you think about bars, movie theaters, restaurants, and sports stadiums not selling the products. Elsewhere, the company is doing a good job managing risk and scaling down as we recently saw with the announcement that Tab is history.

Tesla Delivers Again

For the fifth straight quarter, TSLA recorded a profit. It also beat analysts’ estimates and delivered a record number of vehicles. Another good sign is that automotive gross margins rose during Q3, though TSLA’s heavy spending might be keeping the stock from getting more of a tailwind. Shares rose about 5% in pre-market trading.

News wasn’t so good in the burrito business as Chipotle Mexican Grill, Inc. CMG saw costs climb and shares fall. investors might want to look beyond that to strong same-store sales growth, though. One problem: Fewer sales of what the company called “high margin” beverages. It looks like people ordering food for delivery may be supplying their own drinks, which isn’t very comforting to restaurants that typically make sizable profits on every cup of soda they sell you.

It’s a big morning for the transports, with results expected from Southwest Airlines Co LUV, Alaska Air Group, Inc. ALK, American Airlines Group Inc AAL, and Union Pacific Corporation UNP. Airline stocks have been chopping around in a range the last few months after diving earlier this year, but the Dow Jones Transportation Average ($DJT) is up an amazing 19% over the last three months. A lot of that comes from strength in the package delivery segment.

One thing to consider, according to MarketWatch, is that the Dow Jones Industrial Average ($DJI) didn’t reach a new high of its own after the $DJT recently did. “Dow Theory” suggests that can be a “warning sign” to investors. Whether there’s truth to that this time remains to be seen.

Earnings Season So Far: Not Many Unpleasant Surprises

Stepping away from the fresh earnings and data, let’s take a high-level view of company results so far and how the market’s responding.

We’re less than two weeks into earnings season, and the numbers have generally been good. A couple exceptions were Netflix Inc NFLX and IBM IBM this week, but if there were a drastic difference between what the market had expected going in and the numbers in general, there might have been more volatility and some sort of pullback. Verizon Communications Inc. VZ, Abbott Laboratories ABT, and Texas Instruments Incorporated TXN all delivered strong results and upbeat guidance this week.

There has been some intraday volatility, but generally that isn’t a big story. Meanwhile, the major indices appear relatively range-bound for now, anyway. That could change quickly when you consider some of the heavy hitters lined up for next week, including Amazon.com, Inc. AMZN, Alphabet Inc GOOGL, Facebook, Inc. FB, Microsoft Corporation MSFT, and Apple Inc. AAPL, so we’re far from out of the woods.

The market entered earnings season with price-to-earnings multiples pretty high from a historic perspective, leading some to wonder if stocks climbed too far, too fast. So far, earnings data hasn’t seemed to make investors seriously question the valuation picture. “So far” being the operative phrase there.

One thing that’s leveled off a little the last few days after being a factor in September and earlier this month is sector rotation into small-caps. The Russell 2000 Index (RUT) of small-cap stocks suffered more than any other big index yesterday and is down 2.3% since peaking Oct. 11. That’s roughly in line with the S&P 500 Index’s (SPX) 2.1% decline since then.

Generally, small-caps have done better on days when it looked like a heavy dose of stimulus might be on its way, meaning $1 trillion or more. That’s looking questionable and could help explain why small-caps—which typically have more exposure to the domestic economy—did poorly on Wednesday.

Small-caps also might also have gotten slapped down Wednesday by worries that sections of the country might be heading back into virus-related shutdowns. Those could have a huge impact on smaller, domestic firms.

It was interesting to see some of the “stay-at-home” companies also take a beating Wednesday despite those shutdown fears. The carnage swept up shares of Slack Technologies Inc WORK, Peloton Interactive Inc PTON, Docusign Inc DOCU, Zoom Video Communications Inc ZM, and Netflix Inc NFLX. While the damage to NFLX shares might be due to disappointing subscriber growth, it’s harder to see why the other homebodies got hit.

There’s a chance it just reflected profit-taking in a few of the more highly-valued shares as the election gets closer and some investors start to feel nervous. Consider watching those stocks today for any possible follow-through. Also, be on the lookout for general choppiness as the weekend approaches, because some active traders might be less willing to carry long positions into a break with the election getting so close.

For what it’s worth, most of the mega-cap Tech and semiconductor shares held their own on Wednesday, possibly reflecting investors feeling more comfortable in stocks that weathered most of the 2020 turbulence.

Risk-On Or Risk-Off?

We noted here yesterday that fixed income often can be a market barometer. If that’s the case now, it looks like the U.S. Treasuries market is playing a “risk-on” tune as the 10-year yield finished above 0.8% for the first time since early June. When yields rise, it means investors are selling fixed income, which also means they might be jumping back into more risky investments like stocks as they contemplate possible fiscal help from Washington.

Whether yields can stay above 0.8% and even march all the way toward 1% again could be determined by the stimulus outcome, covid caseloads, and the election. News on any of those fronts might have the biggest impact on which direction yields trend from here.

Another sign that risk-on could be back in town (at least for the moment) is volatility’s retreat the last day or two after flirting with 30 in the Cboe Volatility Index (VIX) overnight Monday. One thing seems certain: The VIX has been stuck in the mud between 25 and 30 for what seems like weeks.

At the same time, the dollar hit one-month lows yesterday (see more below). Typically the dollar rises along with yields, but if “risk-on” is really at work here, the dollar’s descent could point to investors fleeing so-called “safe havens” like the greenback in hope of getting better returns elsewhere. Also, the dollar could be experiencing a bit of pressure from stimulus talk stirring inflation worries.

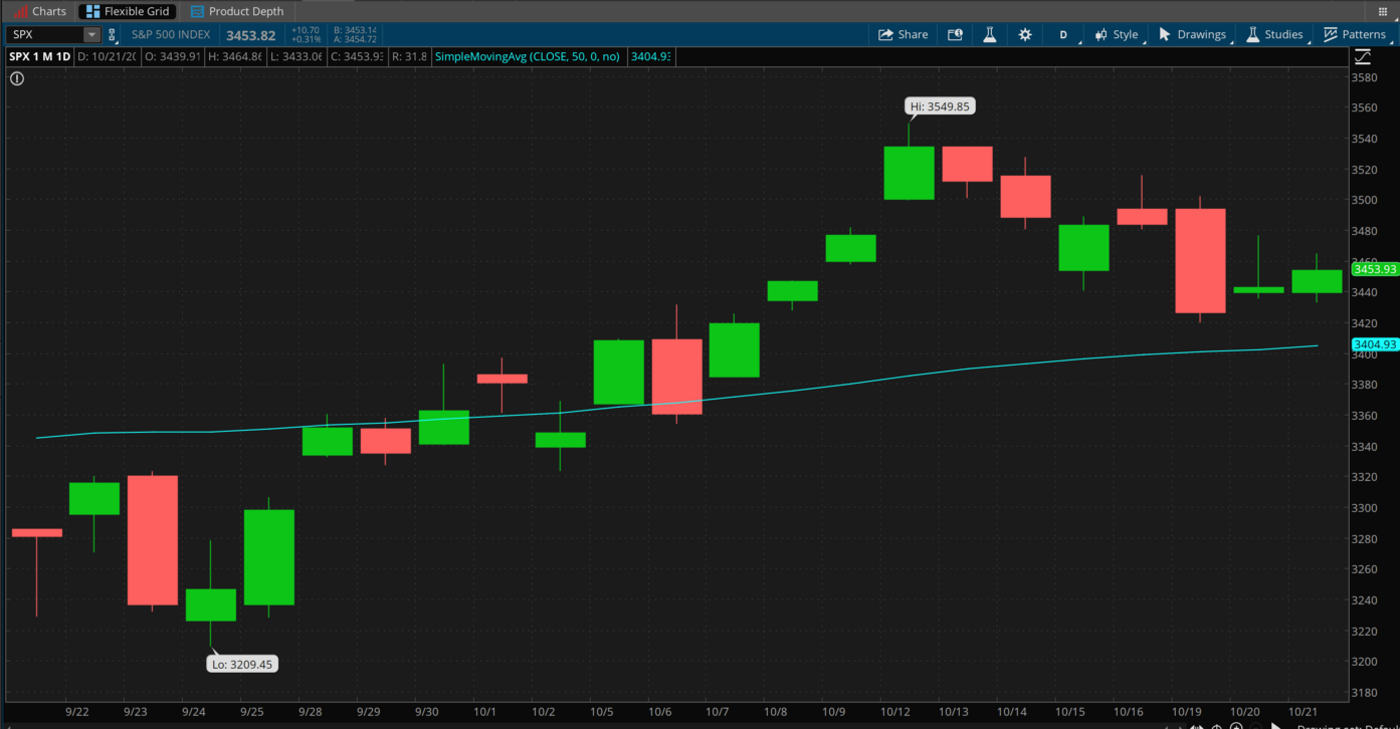

CHART OF THE DAY: HUGGING THE LINE. There’s still more than a week left in October, so things could change. Having said that, this one-month chart of the S&P 500 Index (SPX—candlestick) belies some analyst predictions that this month would take us on a wild ride into the election. The SPX has basically been sticking closely to its 50-day moving average (blue line), closing between roughly 3300 and 3500 for more than three weeks in a row. There’s been solid buying of dips and selling of rallies when the SPX goes down or up, and it’s basically in a holding pattern. Data source: S&P Dow Jones Indices. Chart source: The thinkorswim® platform from TD Ameritrade.For illustrative purposes only. Past performance does not guarantee future results.

Dollar Strength MIA: There’s been lots of talk lately about dollar recovery from its summer lows. For now, those rumors look a little exaggerated. As of Wednesday, the U.S. Dollar Index ($DXY), which measures dollar strength vs. a basket of other currencies, had crumbled to 92.50, down from last week’s highs near 94 and not far above its 2020 lows near 92 and below the recent September peak above 94.5. That’s particularly weird when you consider the rise in Treasury yields, which most of the time would give the dollar a lift. Some market relationships like this one continue to be out of sync, and only time will tell if they get back to normal.

At times last week the dollar got some help from a euro that was on the downturn thanks in part to rising covid cases there. Strong U.S. data, including a September retail sales report last Friday that was off the charts, also appeared to underpin the greenback. These factors could still help the dollar as we move ahead, but for now, a clear path back to the mid-90s or above isn’t guaranteed. Especially if stimulus talk stirs inflation worries.

Gold Rush Yesterday Defies “Risk-On” Psychology: Relationships are all over the map this week. Even as investors fled bonds and the greenback on Wednesday, gold—often seen as another “safe haven”—rose pretty sharply. Some analysts say there may be people moving into gold instead of bonds with yields so low, though it’s worth noting gold offers no yield.

If you look at gold on its own, it could suggest people are going back to one of the oldest hedges against inflation and economic turmoil. One day isn’t a trend, though, and gold—while still historically high—isn’t too close to its summer peaks and hasn’t shown much direction either way the last month or two.

How Healthy is the Health Sector? Health Care is expected to top the Q3 earnings leaderboard. Don’t get too excited about that, though, because competition is pretty thin. The sector is seen reporting revenue growth of 8% and earnings per share growth of 1.6%, according to research firm FactSet. Four of the six industries in Health Care are seen reporting year-over-year growth in revenue, including Biotechnology (22%), Life Sciences, Tools, & Services (9%), Health Care Providers & Services (8%), and Pharmaceuticals (7%).

Two health industry sub-sectors are expected to report declines in revenue: Health Care Technology (-4%) and Health Care Equipment & Supplies (-1%). These might still be hurting from drops in procedure volume related to people canceling or rescheduling surgeries and other medical visits due to the pandemic. Still, when you think about it, it’s pretty impressive to see any companies grow revenue year-over-year in this environment. It figures that if anyone can, it’s the health firms.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Photo by Erol Ahmed on Unsplash

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.