Vaccine makers are batting 1000, to borrow a baseball term. So far they’ve gone two for two in terms of positive results, and Wall Street is rounding the bases again early Monday.

Moderna Inc MRNA became the latest company to announce an effective vaccine, kicking off what appears to be a repeat of last Monday when the market soared on news of Pfizer Inc. PFE and BioNTech SE’s BNTX vaccine.

Moderna has the lead for now, reporting 94.5% effectiveness, compared with better than 90% for PFE/BNTX. That’s arguably neither here nor there when you consider some medical experts were originally hoping for just 50% to 60%.

The same pattern seems to be forming early Monday as a week ago today, with stay-at-home stocks putting pressure on the Nasdaq 100 (NDX) even as other indices roar. Shares of MRNA rocketed 16% higher in pre-market trading even as Zoom Video Communications Inc ZM fell 6% and Peloton Interactive Inc PTON fell 4%.

There’s still plenty to worry about as virus cases keep climbing and more states talk about possible shutdowns. Lockdowns could absolutely continue to affect the market, and possibly start eating into near-term earnings. The vaccine news has been great, but the logistics to distribute these products can take nine months to a year. Some medical experts think we might not get to normal until next summer.

Also, investors should consider keeping their enthusiasm under control amid this amazing rally. Nothing goes up forever, and eventually some consolidation could creep in. The counter-argument is that the market’s incredibly strong and for many people it still seems like the best game in town, so to speak. While it’s true the 10-year Treasury yield is approaching 1%, do people want to put money in bonds now when there could be risk to principal?

Last week’s PFE/BNTX vaccine news injected some confidence, helping the S&P 500 Index (SPX) record its first all-time high close Friday in more than two months. That finish at approximately 3585 eclipsed the Sept. 1 closing record by five points and arguably gave the market a nice technical tailwind to start the week. Sometimes closing above an old high can ignite new buying interest.

Despite virus fears, the Cboe Volatility Index (VIX) has descended to three-month lows near 23, almost the softest levels of the pandemic recovery (see more below). The odd thing this morning is that VIX is up a bit despite the rally in the SPX. That’s something to consider watching, because we’re near this 23 level that’s been a support point for VIX.

Risk “Horsemen” Generally Calm

While 10-year yields and the dollar index couldn’t preserve big gains they made earlier last week, at least the “horsemen of risk” weren’t stomping too loudly early Monday. Gold has been hanging out around $1,870 an ounce, historically high but well below summer peaks. The 10-year yield stands at 0.92% early Monday after last week’s run toward 1% flamed out. Bonds have cooled off pretty noticeably from earlier this fall when the yield sank toward 0.7%.

The failure to take out 1% last week might reflect tepid inflation data on Thursday and Friday. Yields tend to rise in times of economic strength, and inflation tends to climb when the economy gets hot. Unfortunately, inflation didn’t really show up in last week’s consumer price index (CPI) and producer price index (PPI) data, so yields lost a bit of their mojo.

Maybe inflation doesn’t hint at much economic sizzle, but there’s growing optimism for next year. It’s still more than a month until 2021, but already expectations are riding high for earnings growth. The Wall Street consensus is for 22% S&P 500 earnings gains in 2021, according to research firm FactSet, but other analysts are even more optimistic amid hopes for a vaccine and the pent-up demand it could unleash.

Earnings ultimately drive the market, and could do their part to keep valuations from getting out of hand. If you’re looking out over the next 12 months, the average S&P price-to-earnings ratio is 21.8, approximately a 40% premium to the 10-year average, according to research firm Briefing.com.

That might sound alarming, but, as Briefing.com noted, the persistence of low interest rates could offer justification for the premium multiple. That said, valuations now do reflect pretty nice earnings growth next year, so it’ll be important to see if companies can live up to expectations.

Get Ready: Retail Earnings Now At A Store Near You

Looking at the week ahead, retail earnings step into the center ring. The fun begins tomorrow morning with Walmart Inc WMT and continues later this week with Target Corporation TGT. Other major retail firms expected to report in coming days include Home Depot Inc HD, Kohl’s Corporation KSS, Lowe’s Companies Inc LOW, Macy’s Inc M, and Foot Locker, Inc. FL.

Retail stocks did pretty well last week, helped by the vaccine news. Still, it could be a long time before a vaccine is readily available, meaning a tough winter ahead for retailers without a major online or pick-up presence. It’s been a really tough year for department stores.

That hasn’t been the case for WMT, however, as its first-half 2020 earnings just tore the cover off the ball. WMT was one of the few big-box retailers ready with a robust online presence and the people power to handle the onslaught of lockdown-related sales.

Most analysts expect continued strength for Q3, but some wonder whether WMT’s results will be off the charts like they were in Q1 and Q2. Online sales in Q2 jumped 97%, and net income surged a jaw-dropping 80% to $6.48 billion. It might be tough to see a repeat performance quite like that when WMT reports early Tuesday. Guidance could play a big role in how investors treat WMT shares following the earnings report.

WMT has been pushing Black Friday sales since before Halloween, so analysts said they’re looking forward to hearing what might actually be happening in these still-early days of the most important shopping period of the year (see more below).

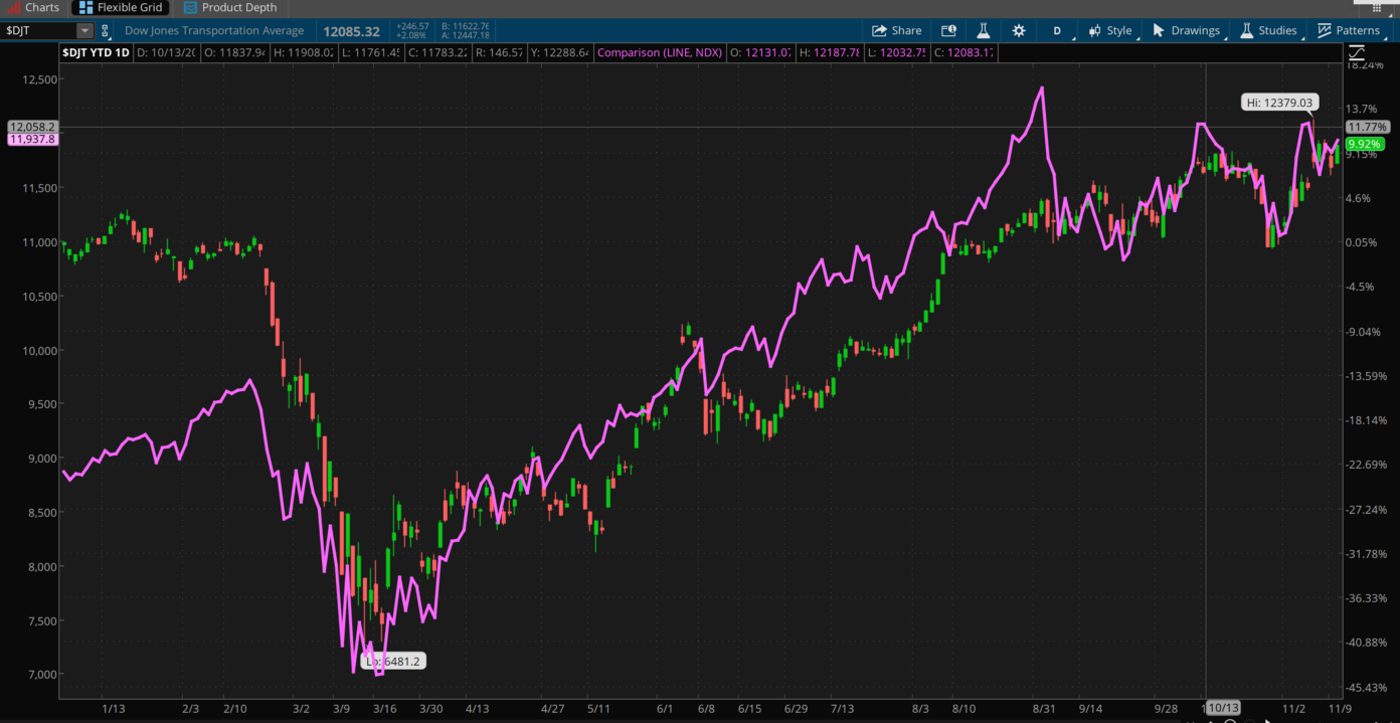

CHART OF THE DAY: LOOK OUT! NO BRAKES! It’s common knowledge that “stay-at-home” stocks have boosted the Info Tech sector. You can see that here in the year-to-date performance of the tech-heavy Nasdaq 100 (NDX—purple line). Even more impressive, maybe, is how the Dow Jones Transportation Average ($DJT—candlestick) continues making new highs and keeps pace with the NDX. That partly reflects that someone has to deliver all those goods people are buying online. And now the holidays approach. Data sources: Nasdaq, S&P Dow Jones Indices. Chart source: The thinkorswim® platform from TD Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

This Week’s and Last Week’s Numbers: Data this week won’t offer a lot of fireworks, with the exception of retail sales and existing home sales. October retail sales take the spotlight tomorrow morning, and Wall Street consensus is for 0.5% growth, according to Briefing.com. That’s down from 1.9% in September. Sales that month got a boost from a huge jump in the clothing category that might be hard to duplicate, but a lot of other categories also grew.

Taking a quick look at last week’s sector action, Energy led everyone by miles with 10.5% gains over the last five sessions. A jump in crude to back above $40 a barrel probably helped, along with the vaccine news that raised hopes of stronger demand next year. Still, we’ve seen this movie many times before. It feels like every time people get excited about crude topping $40, you look a few days later and it’s back at $36. This morning it’s up 4% at nearly $42.

Other sector stalwarts last week included a 5% rise in Financials as yields improved, and a 3% jump in Industrials. Some of the more “defensive” sectors like Utilities, Staples, and Real Estate also performed well. Surprisingly, Technology was the third-worst performer last week. This could reflect the “stay-at-home” trade losing a bit of its appeal.

An Eye on Holiday Shopping as Thanksgiving Nears: One of the main things to listen for on this week’s retail earnings calls is how companies see the holiday shopping season shaping up. It’s likely to be kind of a mixed bag, if you listen to analysts and others who study the retail industry. On the one hand, there’s still high unemployment, threats of stores getting shut down due to coronavirus outbreaks, and people who still have jobs but feel scared to spend too much.

On the other hand, people won’t necessarily be spending money on eating out, throwing holiday parties, or traveling to exotic locales. Meaning those who do have jobs might throw more money at holiday gifts, helping retailers. The National Retail Federation expects consumers will spend around $998 per person this year on holiday shopping, $50 less than last year, partly because they’re likely to focus on gifts for others rather than spending on themselves like in years past.

VIX Eyes Milestone: Early last week, the Cboe Volatility Index (VIX), often called the market’s “fear gauge,” dipped to its lowest level since late August at around 22.6. The low that month was just above 21, so any drop under that could signal sentiment really starting to ease following that pre-election rally to 40. What would be interesting is if the VIX could get back below 20, a level that’s historically been about average for the index. That would mark a real milestone in the market’s reaction to the pandemic, because VIX hasn’t been below 20 since before COVID-19 showed up.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Photo by Marcin Kempa on Unsplash

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.