The market feels like a coiled spring as we start the final week of the quarter. Last Friday’s late surge to new record highs despite the selloff in media stocks provided fresh life, but that strength didn’t show up for work Monday morning.

One question is whether the S&P 500 Index (SPX) can reach 4000 and climb out of its long-term trading range roughly between 3725 and 3970. Another question is whether the “reopening trade,” which flourished late last week, can continue with so many reports coming in of higher average daily Covid cases across the country.

Stocks retreated overnight but recovered slightly from their lows as morning approached. Bank stocks got the worst of it as Treasury yields ticked lower, down to around 1.64% for the 10-year note. Some banks also appeared to take a hit from news that a hedge fund had defaulted in the wake of last week’s selloff in media stocks (see more below). Most U.S. banks look OK, but a couple of overseas ones are down. Losses for the big U.S. banks appear to be small.

It’s kind of interesting that we set a new high Friday when media stocks were under such pressure. Considering how fast that rally occurred in the final minutes, it’s not too surprising to see stocks a little weaker this morning. Volatility rose, with the Cboe Volatility Index (VIX) back above 20 after falling below it last week.

Crude also gained in the early going, with everyone still watching the Suez Canal situation. There was also a bit of good news from the mother country today as England eased its Covid stay-at-home order. Tennis and golf are back, but haircuts are still forbidden, the BBC reported.

Jobs Report Due Friday, But Will Anyone Be Around For It?

It’s kind of a strange week. First of all, the new quarter starts Thursday, and the markets are closed Friday for the holiday. Even though things are shut down, the Labor Department says it plans to release the March payrolls report that day. Check this week to see if that schedule changes.

Assuming Friday’s the day, we won’t be publishing our Daily Market Update, but will include analysis the following Monday. Besides futures trading on Friday and Sunday night, that will be the first chance the overall market gets to react to the data. Hard to remember this happening before, and it’s odd. There will likely be a lot of futures trading Friday, but disconnected from the underlying shares. Many people will have all weekend to digest the numbers before trading them.

Before the jobs report, we might see some end-of-the quarter position squaring where traders shed their losing positions or cover shorts. Also, there can sometimes be quick rallies the last few days of a quarter as major funds perform some “window dressing” where they load up on the quarter’s best performers. So we’ll see if that’s the case.

All this means choppy action is possible, especially Wednesday. Thursday brings the always closely-watched monthly ISM manufacturing report, which we’ll preview tomorrow.

For people who like earnings, the start and end of quarters don’t tend to offer much. Still, there are a few worth watching over the next few days, including pet food retailer Chewy Inc CHWY, which performed very well during the worst pandemic months as people hunkered down at home but hasn’t had a great 2021 so far from a market perspective. Neither has Lululemon Athletica Inc LULU, another company on this week’s calendar. Chipmaker Micron Technology, Inc. MU also is expected to report, and so is Dow Jones Industrial Average ($DJI) component Walgreens Boots Alliance Inc WBA.

There also could be news from Washington, as President Biden is scheduled to introduce his infrastructure plan on Wednesday. This could mean proposals for higher taxes on corporations and the wealthy, according to media reports over the weekend. Any sign of rising taxes tends to get Wall Street’s attention, because they can directly affect future earnings. Listen for details on exactly how much the proposal suggests raising the corporate rate, which is now at 21%.

Last week brought investors a bit of relief from the relentless rise in Treasury yields. Don’t get too comfortable yet, because it’s hard to see this lasting. One reason is purely technical. The 10-year yield made an attempt to break below the psychological 1.6% level at one point last week but failed. It then rose from there before getting checked early today.

Also, the dollar continues to look firmer, and higher yields and a stronger dollar tend to be a tag-team performance. The U.S. Dollar Index ($DXY) has generally risen with bond yields so far this year, and if economic data this week—especially manufacturing and jobs—look solid, both yields and the dollar could gain support.

Participation Trophy

Whatever happens this week, it’s very good to see so much participation in the recent SPX surge. By that, we’re talking about the depth of companies that saw shares rise with the market. Last year, the argument against the rally was that a few high-powered “mega-caps” were thriving and lifting the SPX while most companies either flatlined or struggled. Not so much this time.

For instance, last Friday, 452 S&P 500 stocks finished higher. That’s the third time so far this year that at least that many components of the index have gone up on a single day, according to Barron’s, and it’s great to see the tide lifting most boats, not just the ocean liners.

As stocks climbed out of the muck last week, volatility kept retreating. The VIX ended Friday below 19. Earlier this year, VIX contacts farther out in time had pretty massive premiums to the front-month contract, but things have changed. You have to look farther than a month from now to see a VIX contract trading above 22, and out to July before a 25. That’s a long way off, and traders still build in some future premium for volatility. Nothing like earlier this year, though, when we often saw farther out contracts trading at 30 or above.

That being said, some analysts fret about the premium priced into future contracts, saying it’s above normal and means fear hasn’t left the room. The “contango” we’re seeing in the VIX term structure (where future prices are more expensive than spot prices) could reflect pandemic fears and rising Treasury yields.

Investors appear to be finding some solace in solid-performing companies, including Tech and Healthcare companies with strong balance sheets

Earnings Season Looming

Q1 earnings season doesn’t start for a couple of weeks, but now is a good time to start getting a handle on company guidance and analyst expectations. Remember, Q4 earnings massively outshined expectations. Will we see a repeat?

Taking a look at what companies expect for Q1, there’s sun in the forecast. Of the 94 companies sharing guidance so far, 34 have issued negative earnings per share (EPS) guidance and 60 have issued positive EPS guidance, according to FactSet.

The number of companies issuing negative EPS guidance is well below the five-year average of 66, while the number of companies issuing positive EPS guidance is well above the five-year average of 35. If 60 companies or more continue to give positive vibes, that would set the record going back to when FactSet began tracking this stat in 2006.

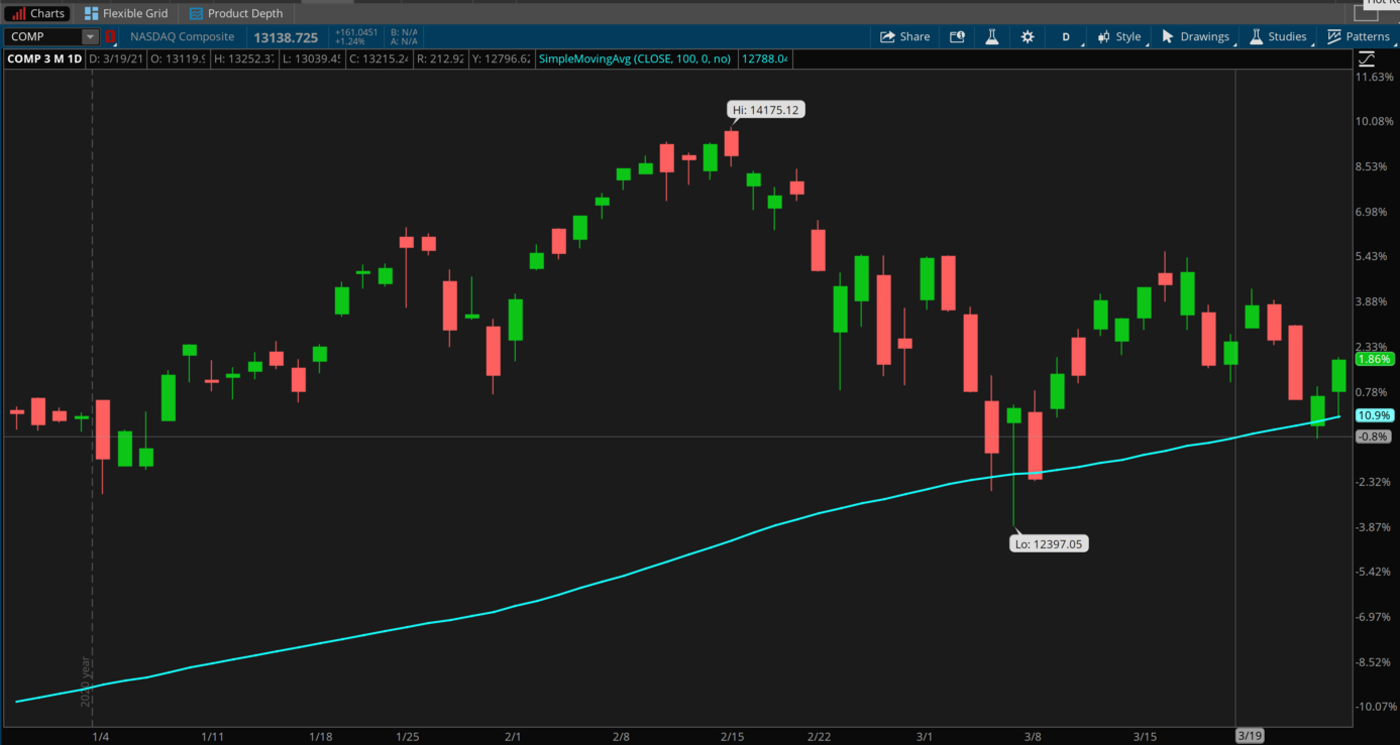

CHART OF THE DAY: SUPPORT TEST FOR COMP. Though the Nasdaq (COMP—candlestick) clawed back at the end of last week, it remains a bit delicate from a technical standpoint, as this year-to-date chart shows. The index, which is dominated by Tech, hasn’t made a new high since mid-February, and recent high points have been trending lower. It’s also not far above its 100-day moving average, a level it’s now bounced off of a couple times over the last few weeks. The question is whether support there can hold. Data source: Nasdaq. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Mass Media’s Mixed Messages: A recent article in The Ticker Tape looked at the battle of streaming giants attempting to join the streaming party led by Netflix Inc NFLX and asked whether consumers were approaching “subscription fatigue.” Last week a couple big media/streaming companies, ViacomCBS VIAC and Discovery Communications Inc. DISCA took it on the chin, with each losing about half their value in a few sessions. Granted, these and other streamers had previously seen monster rallies as investors gobbled up shares of companies that thrived in the stay-at-home economy. Now it seems some media companies are losing steam as the world looks toward vaccinations and a return to normalcy—similar to other stay-at-home darlings such as Zoom Video Communications Inc ZM and Peloton Interactive Inc PTON.

What’s the lesson here? One might be a reminder that mass media firms sometimes fit best inside a company with diverse business units and income streams (what seasoned investors refer to as the “conglomerate model”). Walt Disney Co DIS, AT&T Inc. T, Amazon.com, Inc. AMZN, and Apple Inc AAPL all have their media arms as part of a wide set of business units. Though each is off their highs in recent days, none are seeing the kind of action as VIAC and DISCA.

Smoothing the Way: Basically, the path of least resistance for yields still looks higher, which could continue helping Financial stocks and weighing on Tech. Many analysts are baking in a rise to 2% at some point this year for the 10-year yield, up from Friday’s close of 1.68%. However, as one analyst pointed out, there’s no reason why a yield that’s still so historically low should hurt the Tech sector. After all, Tech did just fine a few years ago when the yield was 2.5% or higher. All this focus on the “Tech effect” actually distracts from the real reason rates are running hot, which is the fear of blow-back inflation that slows the economy down and creates asset pressure.

Friday’s Personal Consumption Expenditure (PCE) prices report was benign on the inflation front, but it’s the coming inflation reports that could get some people nervous. That’s because the comparisons are against last year’s pandemic-related collapse in prices. Remember to take this for what it is by understanding the comparison issue. It’s later this year when we’ll see if the Fed is right about any price pressure being transient or, if it gets more sticky.

Back to Main Street: Investors seem ready to go out and about. A few of last week’s upside movers included Darden Restaurants, Inc. DRI, and retailers L Brands Inc LB and Restoration Hardware Holdings, Inc RH. LB is seeing an improved sales trend, and RH shares soared to new highs. We can probably attribute these moves at least partly to stimulus and relaxation of some of the restrictions, which have led to a positive shopping boom. Just anecdotally, Chicago’s downtown Michigan Avenue shopping district got crowded recently as warm weather drew people to stores and restaurants. Whether this continues could depend partly on any resurgence in Covid numbers, as well as potential supply problems as demand growth appears to be outpacing revenue growth. Home Depot Inc HD has also seen a winning streak with its stock price. These are all good companies to watch in coming weeks to assess whether vaccinations or new Covid fears are winning the war in consumers’ minds.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.