There’s an old stock market staying that says to “sell in May and go away.”

That’s because, historically, the strongest period for the market tends to be the stretch between November-April, with May-October lagging, according to The Stock Trader’s Almanac.

Whether May will be a selling month remains to be seen, but there seems to be a sense that history might repeat given how elevated many stocks are. The Nasdaq Composite (COMP) and S&P 500 Index (SPX) both gained more than 5% in April, with the latter closing at a record high on Thursday before succumbing to some profit-taking on the last trading day of the week.

Selling pressure doesn’t seem to be a feature of this morning’s trading, with the path of least resistance appearing to be to the upside. Investors seem optimistic given the backdrop of a stronger-than-expected earnings season, improving economic data, a strong vaccine rollout in the United States, government stimulus, and easy monetary policy from the Fed.

Earnings Season Going Better Than Expected

With earnings season in full swing, investors have plenty to digest as they try to form a picture of the market in the near term based on corporate performance, executive commentary, and company outlooks.

Investors can learn a lot from executives during corporate earnings calls discussing the reopening economy and emerging consumer trends they’re seeing.

So far most of the SPX companies that have reported have beaten earnings expectations. On Friday, FactSet said that more SPX companies are beating earnings estimates for the first quarter than average, and that those beats are coming with a wider-than-average margin.

Of the 60% of SPX companies reporting first-quarter earnings, 86% of them had reported earnings that exceeded estimates, above the five-year average of 74%, FactSet said Friday. (See more on earnings below.)

This week, the earnings parade continues, although it may be less intense than last week. ConocoPhillips COP, Pfizer PFE, Uber UBER, PayPal PYPL, Wynn Resorts WYNN, Allstate ALL, T-Mobile TMUS, and Lyft LYFT, are among the companies reporting this week.

Manufacturing, Jobs Reports In The Headlights

It’s also a pretty big week for economic data releases.

A little later this morning, the market is scheduled to get the ISM manufacturing index. The measure of the nation’s factory sector is expected to have jumped again in April a month after the index hit its highest point in nearly four decades. A Briefing.com consensus expects the index to hit 65.3 after a reading of 64.7 the previous month.

We’ll see more from the factory sector on Tuesday with the release of March factory orders, which are expected to return to positive territory. A Briefing.com consensus expects the March number to show growth of 0.7% compared with an 0.8% decline the previous month.

A broader look at the labor market comes on Friday with the release of the nonfarm payrolls report. A Briefing.com consensus is expecting that a cool million jobs were added to the nation’s payrolls in April. As always, a big miss can end up weighing on the market while a big beat can stimulate buying in equities.

Another thing happening this week: The antitrust trial gets underway between Fortnite developer Epic Games and Apple AAPL, in which Epic has alleged AAPL’s requirement that developers use its in-app payment system (and be subject to its commission schedule) amounts to a monopoly. While media reports suggest the suit is a longshot for Epic, it has helped reframe the narrative about big tech companies such as AAPL, Alphabet GOOGL, and Facebook FB and the extent to which their platforms affect consumer purchases.

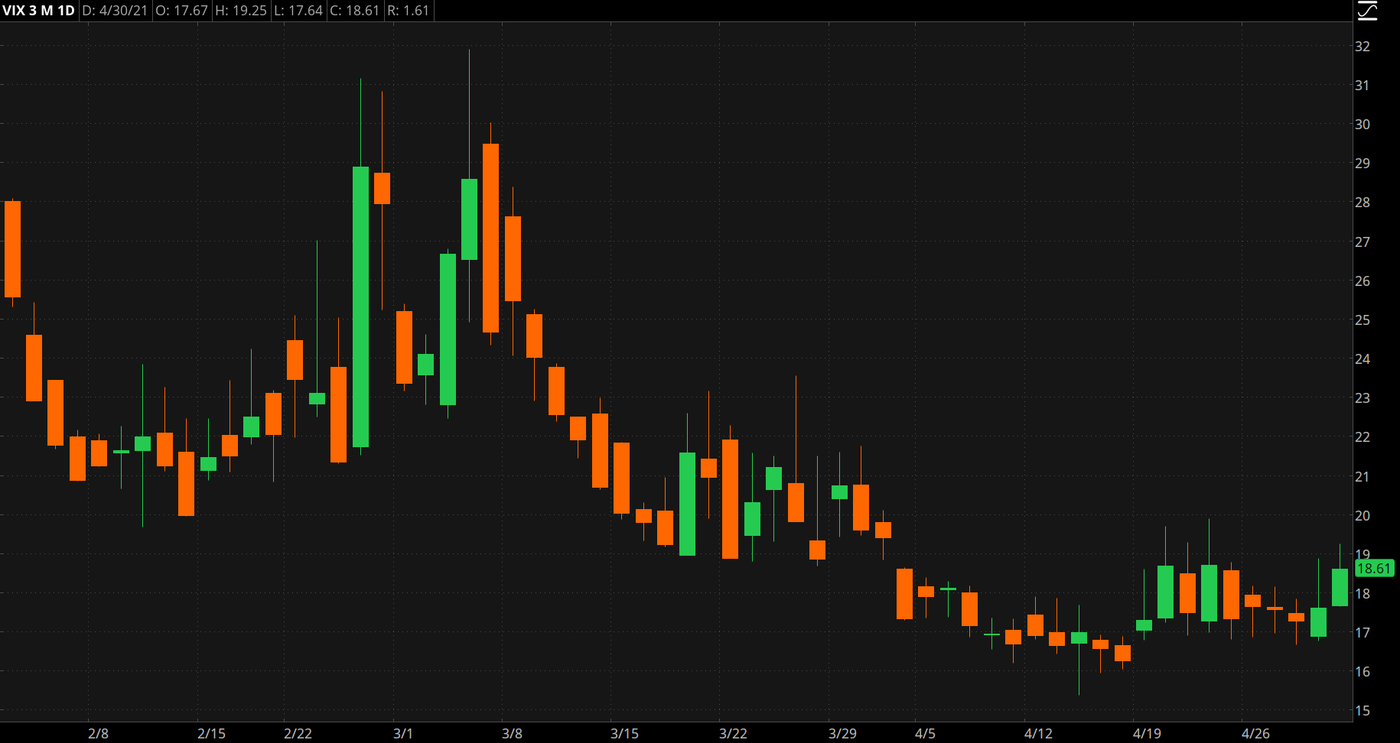

CHART OF THE DAY: VIX FIX: Market jitters, as represented here by the Cboe Volatility Index (VIX) moved higher toward the end of last week. That may be an indication that some investors are worried about high valuations in the market. Data source: Cboe Global Markets. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Driving Demand: This week, ride-hailing companies Uber Technologies and Lyft report earnings as people are more willing to catch a ride as they worry less about catching COVID-19. It’s presenting both companies with a “good” problem to have—a shortage of drivers. As demand for rides comes back faster than drivers do, Uber and Lyft are having to pay more to get contractors behind the wheel. In April, UBER said it was launching a $250 million stimulus for drivers as “there are more riders requesting trips than there are drivers available to give them.” Meanwhile, LYFT is reportedly offering bonuses of up to $800 for referring former drivers back to its app. While a shortage of drivers means the companies are at least temporarily having to spend more on driver incentives, at least it’s a sign that demand is coming back, which investors would probably welcome.

Setting The Bar High: On Thursday, we saw Amazon AMZN crush earnings expectations after the closing bell only to end Friday’s season on a down note. That may be due to some investors having a tinge of fear about some company valuations being high. Earning “beat rates continue to run at record levels though the bar has moved higher, with some of the lackluster reactions to better results from high-profile reporters fitting with concerns about peak growth,” FactSet said in its blog on Friday. We’ll have to see if the Amazon effect continues this week or if strong earnings beats will be rewarded with higher share prices.

Jobless Claims Declining: It could be interesting to see whether weekly jobless claims numbers show another decrease. It was nice to see initial claims drop from 742,000 for the week ending April 3 to 586,000 the week ending April 10 and to 566,000 the next week and to 553,000 last week. While the trend has been in a positive direction, even 500,000 claims would be a historically large figure. It just goes to show that even though the economy is doing much better, it’s not completely out of the COVID-19 woods yet. At least claims are now well under the peak they hit during the financial crisis.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image by freestocks-photos from PixabayEdge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.