The following post was written and/or published as a collaboration between Benzinga’s in-house sponsored content team and a financial partner of Benzinga.

Nvidia and Snowflake report after the bell Wednesday. The options market is pricing just under a 4% move for Nvidia and just under a 7% move for Snowflake.

Nvidia / Expected Move: 3.7%/ Recent earnings moves: -8%, 0%, 0%

Snowflake / Expected Move: 6.6% / Recent earnings moves: +1%, +16%

Options price an expected move based on the uncertainty surrounding the earnings release. Typically that means elevated premiums (making options more expensive) into the event, and lower premiums after. (After earnings, with the uncertainty gone, options typically reset to price more day-to-day expected moves.)

Calls or puts into an earnings event may see a sharp overnight decline in implied volatility (making their premium less expensive). Put another way, when using an outright Call or Put to trade earnings, it’s possible not to realize a profit, even if you were right on direction and the stock has not moved significantly beyond your strike.

In options, however, there are more ways to trade than just Calls or Puts. Debit spreads can reduce the overall exposure to premium by lowering cost, while giving some protection to declining volatility. And Credit Spreads position to actually benefit from declining volatility by being net short premium (net selling options and receiving premium rather than net buying and paying a premium). Of course, direction is still the most important variable, but smarter positioning can lessen, eliminate, or even benefit from some of the other variables. This said, there are additional risks associated with spreads, including liquidity and assignment, that every investor should also be aware of.

Below we’ll look at ways Credit Spreads can express directional and non-directional views, using NVDA and SNOW earnings as examples.

Snowflake

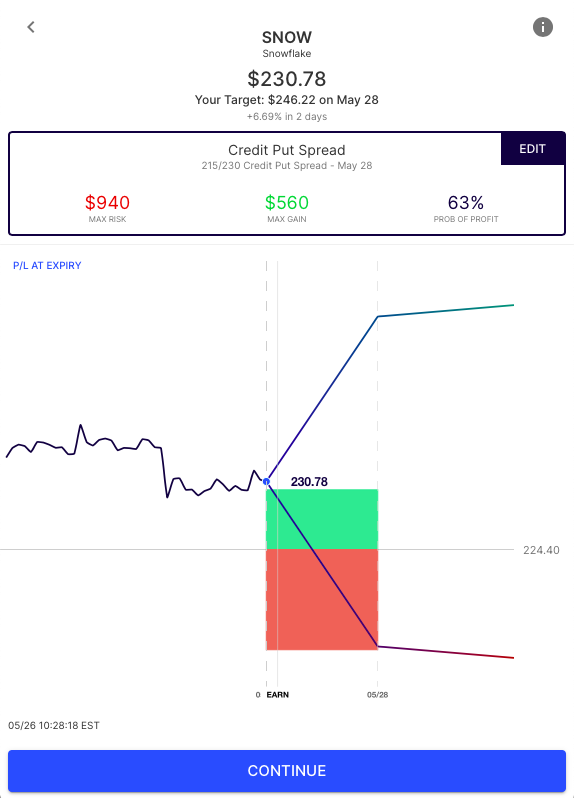

At the time of writing, SNOW stock is about $230. The 6.6% expected move corresponds to about $214 and $240 in the stock. Via Options AI, those price levels can be used to help create a credit spread that “sells the move”. In this case, an Iron Condor (which is the combination of a Credit Put Spread to the bearish consensus and a Credit Call Spread to the bullish consensus):

An Iron Condor is a credit spread that looks to make money if the stock stays within the short strikes (in this example, strikes based on the expected move.) In this case, the Condor risks around $140 to make up to $110 if the stock stays between $215 and $245 on Friday’s expiration

Directional Credit Spreads

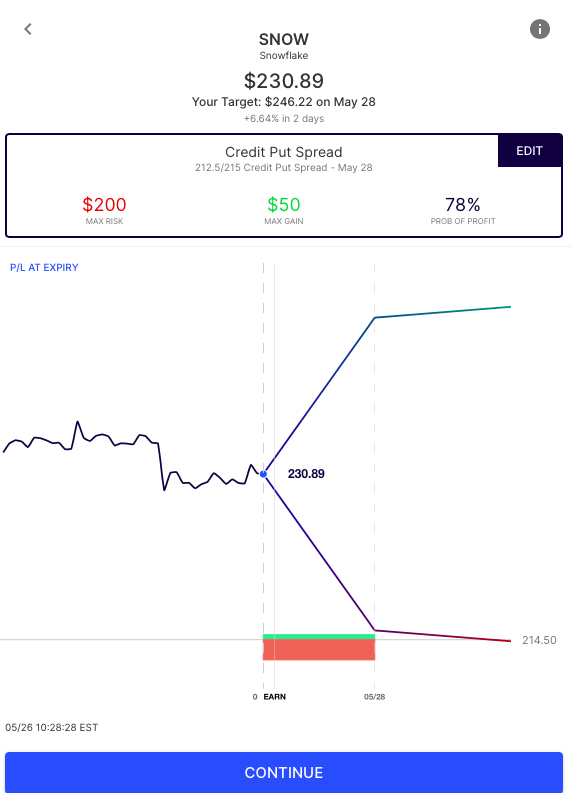

Credit Spreads can also be used to express a directional view. But instead of buying calls or puts and needing a move, a credit put or call spread is positioning against a move. For example, here are two credit put spreads in SNOW, both using the expected move to assist in strike selection. These are bullish trades, but are better thought of as “not bearish”:

Via Options AI:

The breakevens of each trade are below where the stock is currently trading. If the stock goes higher, they are max gain. In fact, any close on Friday above their upper (short) strikes and they are max gain. They are max loss if the stock makes a sharp move lower, below what options are expecting (and below their long strikes).

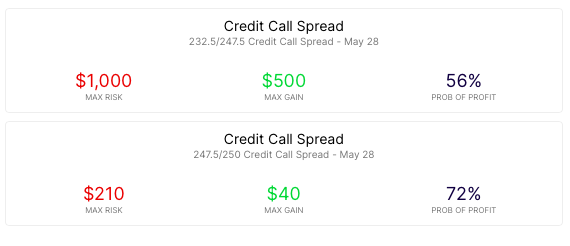

The Credit Call Spread version of these trades are below. Credit Call Spreads can be used both as “selling to the bulls” outright, or as potential added yield for those already long a stock. The ideal situation for added yield is if the stock is higher, but not above the breakeven of the credit call spread. In that case the credit received is added to the gains in the stock:

Aside from the additional potential risks of option spreads (such as early assignment and liquidity), it is important to note that a credit spread caps potential profits, and also risks more to make less. The farther away the breakeven is on the trade (or the higher probability of profit) the more that risk/reward ratio tilts towards risking more to make less.

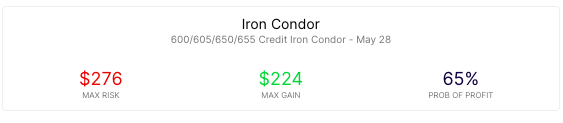

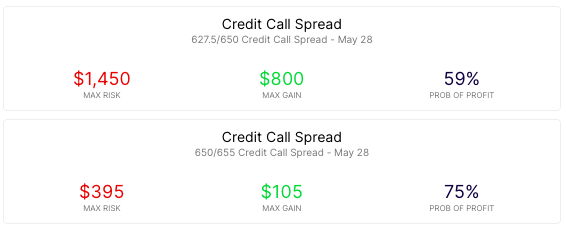

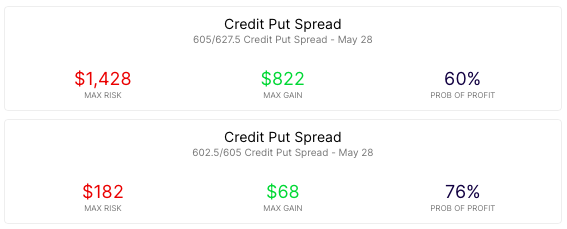

NVIDIA

At the time of writing, NVIDIA is about $625. Its expected move of 3.7% corresponds to about $605 and $652.

Once again, here’s a look at an Iron Condor with credit call and put spreads at those levels:

This Condor, with strikes set at the expected move looks to make max gain if the stock is between $605 and $650 on Friday. It is max loss if the stock is beyond the expected move, above $655 or below $600.

Directional Spreads

Here are bearish credit call spread examples in NVDA based on the expected move (better thought of as “not bullish”:

And here are bullish credit put spread examples in NVDA, based on the expected move (better thought of as “not bearish”:

Options AI puts the expected move at the heart of its trading platform. It allows traders to quickly generate and compare more ways to trade, by entering an informed price target or using the expected move for initial strike selection. The Credit Spreads discussed here are just an example of the various strategies available to traders.

Options AI provides a couple of free tools like an expected move calculator, as well as an earnings calendar with expected moves. More education on expected moves and spread trading can be found at Learn / Options AI.

Image Sourced from Pixabay

The preceding post was written and/or published as a collaboration between Benzinga’s in-house sponsored content team and a financial partner of Benzinga. Although the piece is not and should not be construed as editorial content, the sponsored content team works to ensure that any and all information contained within is true and accurate to the best of their knowledge and research. This content is for informational purposes only and not intended to be investing advice.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.