Walmart’s WMT ability to keep customers coming to its stores will again be on display when Q2 results are released tomorrow morning.

A year ago, people had few shopping options beyond WMT and a few other big stores that kept doors open through the pandemic. Now, with more choices, the question is what WMT is doing to keep old customers coming back and maintain the new ones who started shopping there in 2020.

For the most part, analysts think shopper traction has sustainability, some of it juiced by stimulus payments as well as a return to price-sensitive shopping. In Q1, WMT said foot traffic had picked up as COVID-19 mandates were lifted and shoppers ventured out to stores again.

“Our optimism is higher than it was at the beginning of the year,” Chief Executive Doug McMillon said in May. “In the U.S., customers clearly want to get out and shop.”

Investors will see how well that panned out in Q2, especially considering the rise of the Delta variant late that quarter. Many analysts have said WMT appears to be doing just fine, thank you. McMillon kept a cautionary but upbeat tone last time out. “The second half has more uncertainty than a typical year. We anticipate continued pent-up demand throughout 2021.”

WMT Vs. AMZN?

Some analysts expect Q2 to be relatively strong, though they note WMT is up against tough year-ago comparisons. At Bank of America BA, analysts are more bullish on WMT sales growth than Amazon’s AMZN.

“Walmart U.S. sales growth may outpace Amazon’s total ‘online stores’ growth” thanks to added merchandise, same-day delivery and pickup, and other perks,” BAC said in a recent note to clients.

“We believe Walmart’s omnichannel transformation in the U.S. will continue to gain momentum and support more sustainable and predictable positive same-store sales and traffic at U.S. supercenters and U.S. e-commerce,” the note said.

Consumer Intelligence Research Partners (CIRP) believes WMT’s e-commerce site “continues to show signs of strength,” according to a recent report. Shoppers are forking over some $1,300 a year above their in-store outlay, powering an upswing in average annual spending as the pandemic drove consumers to shop online, according to CIRP.

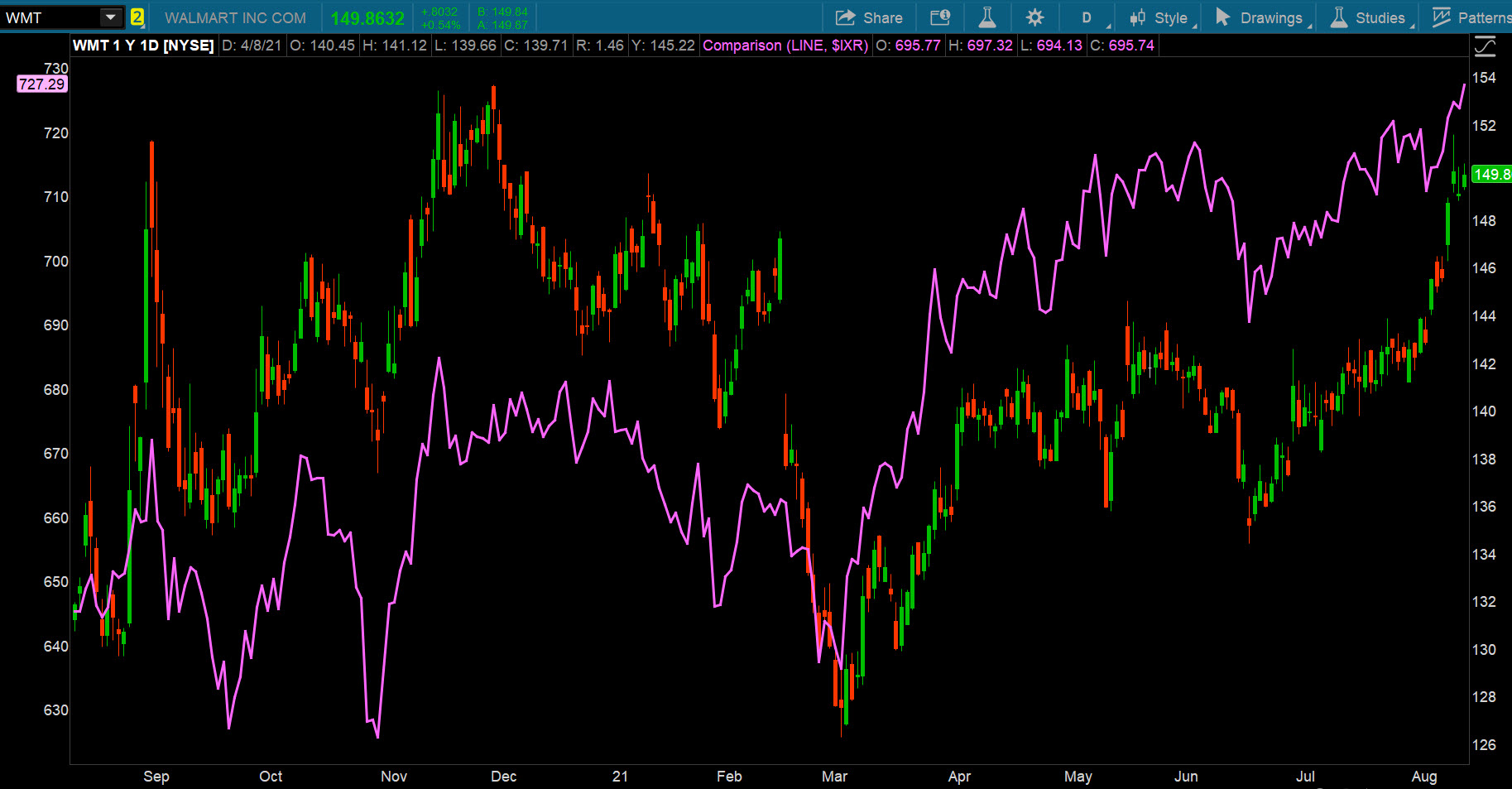

FIGURE 1: IN SYNC WITH STAPLES. Walmart (WMT—candlestick) has been pretty correlated with the Consumer Staples Select Sector Index ($IXR—purple line). The stock has seen a strong up move in the last few days. Data source: NYSE, S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

What Are The Plus Numbers?

Walmart+ has a huge game of catch-up with Amazon’s Prime membership program, but appears to be gaining traction and is something analysts are keeping close tabs on. As of June, PYMNTS data has tracked roughly 53.9 million subscribers to Walmart+. That’s a 21% jump just since May. And remember, WMT only launched the membership perks last September.

Like streaming services, it turns out consumers have more than one perks-related membership, and in Walmart+’s case, about 91% of new subscribers are also Amazon Prime members. Investors might want to take note of WMT’s comments on the membership program and expectations of what might be ahead. Remember, grocery is typically the drawing card for memberships like these.

Grocery Sales Comeback

Grocery sales represent some 56.3% of topline revenues, and in Q1 they faltered slightly —remember shoppers in the year-ago quarter were hoarding water, canned goods, and toilet paper—but apparel, home improvement, and recreation product sales filled the void.

Yet through it all, WMT still was able to hold onto and even edge up a bit in grocery market share, a panic button the retailer pushed earlier this year.

That’s given analysts conviction on grocery sales in Q2. “Grocery should lead (same-store sales) performance, accelerating from Q1,” Credit Suisse analysts said in a recent note.

BA’s Robert Ohmes is looking for hearty deli and bakery margins, anticipating they should come back in a “big way,” he said.

Cowen analysts have proprietary surveys to back up their beliefs that WMT held the lead grocery market share position at more than 58% in June. “We expect Walmart to maintain momentum over the coming quarters as the environment normalizes and shoppers once again become more price-sensitive,” analysts wrote.

Fuller Baskets, Fewer Trips

Analysts said they expect a continuation of a cycle that was prominent during lockdowns, where WMT saw fuller shopping carts but fewer trips. In Q1, transactions dropped 3.2% but average ticket growth shot up 9.5%.

Last time out, WMT easily outpaced Wall Street’s expectations with a 6.2% jump in sales at stores open longer than a year, a key industry metric. The same-store sales fell back for the first time since 2016—in the year-ago period, they had surged 10.3%—but were far ahead of the 2% analyst forecast.

BA’s Ohmes said he anticipates seeing continued general merchandise strength and upside from the back-to-school crowds. He also thinks vision and auto centers, mostly dark during pandemic shutdowns, will bounce back.

Overall, analysts are looking for global same-store sales growth to reach 3.1% with U.S. comparable-store sales up by 3% and international sales jumping 5%. Analysts also said they’re zooming in on Sam’s Club numbers. In Q1, Sam’s Club same-store sales vaulted 7.2%, far above the 1.2% analysts were charting. The warehouse club memberships also reached an all-time high that might proffer a solid outlook for sales ahead.

What Else Is There?

Given that it’s WMT we’re talking about, there’s plenty analysts said they’ll be listening for on the conference call. But here are a few things to keep top of mind:

Delivery: WMT has gone to great strides in recent months to step up the delivery in many ways, including same day, with drones and a number of providers. Executives might reveal what else is up to their sleeves for what has become a must-have for most retailers.

AMZN fees: Earlier this month AMZN announced it would charge Prime members ordering from Whole Foods in five U.S. states a $9.95 delivery service charge. Orders over $35 used to include free delivery everywhere. It will be interesting to hear if WMT addresses that AMZN change, considering a key driver for membership at either is food items and that free delivery still reigns with Walmart+ customers.

Inflation: In Q1, WMT said it expected to see signs of inflation pop up and indeed they did. July’s Consumer Price Index (CPI), released last week, logged a 5.4% jump on a year-over-year basis. On a month-over-month position, they ticked up 0.5%, suggesting to some that inflation is peaking.

But a one-month showing doesn’t make a trend and consumers can widely expect to see higher prices in the grocery aisles early next month. Federal Reserve members continue to hold interest rates near zero and repeat their stance that this strong inflation is temporary, driven by surging consumer demand that supply backlogs can’t keep pace with. Once the backlogs clear, prices will moderate, the Fed has said.

But what do WMT executives see and expect, and how are they going to continue to handle it? And how are they dealing with rising wholesale prices, as seen in last week’s July Producer Price Index (PPI)? In the past, they have mostly kept prices in check to hold on to market share. Analysts said they will be listening to the strategy going forward as commodity prices rise.

Supply: Speaking of the devil in the economy these days, WMT said it expected supply-chain glitches to continue and impact the bottom line. Investors might want to pay close attention to how the retailer intends to manage that.

Labor And Wages: Like many employers, finding workers can be difficult. WMT has done plenty to up its ante to attract workers including raising wages, offering 100% college tuition programs in certain areas, and, recently, giving warehouse employees bonuses and other incentives to work every hour of their schedules as the holiday season logistics blitz gets underway. But WMT, like other retailers, is facing increasing competition from restaurants, hotels, and other in-person jobs that are hiking wages to attract warm bodies. Investors might want to listen to the retailer’s latest plans to keep its workforce full.

Walmart Earnings And Options Data

WMT is expected to report adjusted EPS of $1.56, about even with last year according to third-party consensus analyst estimates. Revenue is projected at $135.92 billion, down from $137.7 billion a year earlier.

The options market has priced in an expected share price move of 3.13% in either direction around the earnings release, according to the Market Maker Move indicator on the thinkorswim® platform.

Looking at options expiring on Aug. 20, call activity is spread out between the 152.50 and 160 strikes. Puts have been active at the 135 and 140 strikes. The implied volatility sits at the 37th percentile as of Friday morning.

Note: Call options represent the right, but not the obligation, to buy the underlying security at a predetermined price over a set period of time. Put options represent the right, but not the obligation, to sell the underlying security at a predetermined price over a set period of time.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.