With Treasury yields losing a bit of their grip and volatility edging lower, stocks have a slight green tint this final morning of the quarter. Barring one of the greatest rallies ever, September is going to be a down month.

A little progress in Washington’s budget battle overnight could help explain what’s going on so far today, but there’s still a long way to go before anyone can breathe easy about the D.C. situation. It looks like a shutdown might be avoided, but the debt ceiling is still looming.

Yesterday saw markets recover a bit from Tuesday’s ugly spill, though the Tech sector didn’t get included in that slight bounce. A more mild day in the Treasury market might have been one factor in the gains, but some “buy the dip” mentality also could help explain the rebound.

While “buy the dip” still exists, what we’ve seen the last couple of weeks is a new theme, “sell the rally.” The market has had trouble holding onto rallies lately, and we’ll see if that pattern continues.

Tech’s Weakness Could Dampen SPX Rallies

One thing to keep in mind is that Tech’s huge weighting in the S&P 500 Index (SPX) could be something that prevents the index from clawing back to recent highs if Tech can’t fully recover. A few “mega-cap” Tech stocks make up a huge part of the SPX, so gains in lower-weighted sectors like Energy can’t necessarily make up the difference if Tech is on the sidelines.

And Tech got some more bad news this week aside from rising yields (which hurt Tech in part because higher yields make future profits less valuable and the Tech sector is all about hopes for sizzling future profit gains). The semiconductor sector came under pressure after Micron MU issued downside guidance for its fiscal Q1 due to ongoing supply chain disruptions. The Philadelphia Semiconductor Index (SOX) slipped 1.5% yesterday.

Having said all that, some of the major Tech stocks like Salesforce CRM, Microsoft MSFT, and Nvidia NVDA saw gains in overnight trading. We’ll see if this gets any follow-through after the opening bell.

Bed Bath & Beyond BBBY is going in the opposite direction of those Tech stocks after a disappointing earnings report today. Shares fell a dramatic 17% in pre-market trading. The company talked about a “traffic slowdown” due to the Delta variant, and “steeper cost inflation.” Those evidently weren’t what investors wanted to hear.

The one theme that keeps coming out in earnings we’ve seen lately is the supply chain, supply chain, supply chain. As we head into the holidays and Q3 earnings, it wouldn’t be surprising to hear retailers talking about this even more. The issue is primarily in retail now, but every industry could be affected and it appears to be causing some analysts to bring down their Q3 earnings estimates. It may be worth looking over your portfolio to see how badly the stocks you hold might be hurt by this.

Looking at the technical picture, the SPX remains well below the 50-day moving average of 4444 even after Wednesday’s slightly positive performance. The SPX hasn’t spent any appreciable amount of time below the 50-day all year, but it could be losing a little momentum these last few weeks with a pattern of lower highs and lower lows. The 100-day moving average of 4343 held up on Tuesday’s selloff, and may now represent a support point.

Pin the Tail on the Catalyst

It’s not always easy to say the market moved in a certain way because of a specific catalyst, but the recent softness in Tech almost certainly comes at least in part from the Fed’s more hawkish stance, outlined after last week’s Fed meeting. But the Fed’s not the only game in town.

Capitol concerns. You could also argue that some of the action this week relates to the precarious situation on Capitol Hill, where Congress appears to be playing a game of bumper cars and making little progress on key issues like the debt ceiling and avoiding a shutdown. Tuesday’s sharp selloff across a broad spectrum of the market could certainly be a symptom of the political battles, and even Wednesday’s slight rebound favored more “cautious” sectors like Consumer Staples and Utilities. We’ll have to see if this more cautious stance is here for a while or just a passing thing.

Volatility reverberations. The Cboe Volatility Index (VIX) eased back just a bit to around 22, down from the highs around 25 earlier this week but above the recent average. A drop below 20 might indicate caution receding, but it’s hard to believe we’ll see that with so much business left undone in Washington, D.C. A day like Tuesday, when the market gets slammed so hard, typically has reverberations that last a few days, at least. Higher volatility could be a sign that the bumps and bruises might not be over yet.

Watching the yield. Also, even though Treasury yields didn’t really build on their recent sharp move higher Wednesday, they didn’t exactly ease off, either. While some of the shorter-term yields like the two-year and five-year stepped back, the benchmark 10-year yield was back above 1.54% by late Wednesday, up 25 basis points from last week’s low of 1.29%.

While 1.54% is low historically, that’s a very quick and dramatic gain for the market to absorb in just a week. Could the yield make another run at this year’s high near 1.75%? It’s certainly possible, especially if we see strong data over the next week or two.

Eyeing the Data

Key data to watch at the end of this week is the ISM manufacturing read for September. It’s due early tomorrow and analysts expect a headline figure of 59.5%, according to research firm Briefing.com. That’s exactly in line with the previous month, and probably wouldn’t cause any concern. A big bump higher, however, might raise inflation fears.

Speaking of which, tomorrow also brings the monthly personal consumption expenditure prices (PCE) data from the government. Analysts expect a core rise of just 0.2% for August, which may reflect some economic slowing amid the Delta variant. Anything much higher than 0.2% could spark more inflation worries and perhaps send yields higher.

“Fed Watch” Tool Back in the Mixture

For the first time in months, the CME Group’s CME FedWatch tool is starting to be relevant again. That’s the gauge that tells you where the Fed funds futures market anticipates the chance of future Fed rate hikes.

Nothing to get too excited about yet, because futures show a 100% chance of the Fed funds rate staying at the current zero level through the end of this year. It gets more interesting when you look a bit farther out. There’s a 4% chance of a hike by next March, the tool shows. That rises to 21% by next June and over 50% by a year from now. There’s even a small (10%) chance of two rate hikes between now and next September, according to the futures market.

Of course, things could change a lot between now and then depending on everything from economic data to U.S. politics (mainly the budget debate) to the course of Covid. The Fed might also take some cues from how the market reacts when the Fed begins to taper the $120 billion a month stimulus it’s had in place since Covid began.

Although the Fed doesn’t have any responsibility to keep stock market investors happy, there’s a sense that sometimes the Fed acts in ways designed to do that, at least peripherally. Its quick move to lower rates in early 2019 after a series of rate hikes helped lead to a market selloff in late 2018 might have been a “for instance” moment.

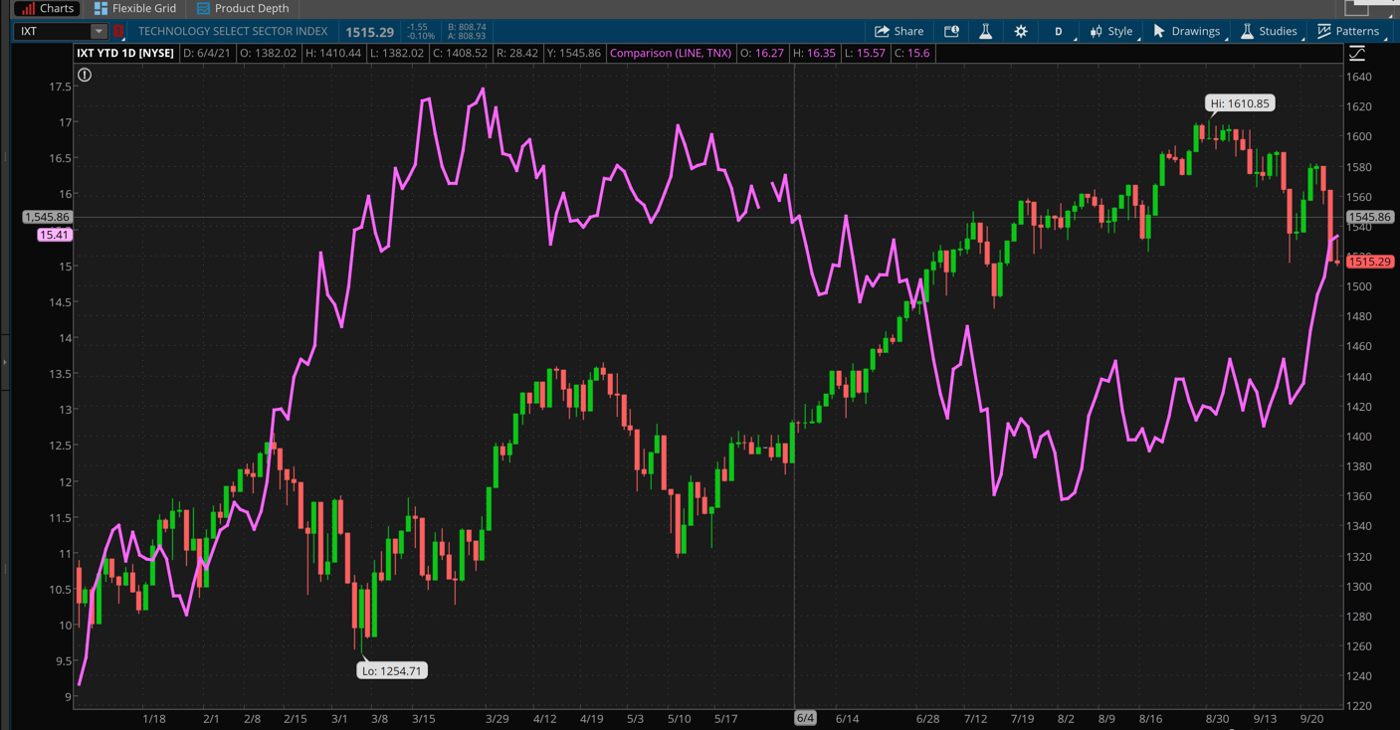

CHART OF THE DAY: SEE-SAW RIDE FOR TECH. Want to know where the S&P 500 Tech sector (IXT—candlestick) has gone this year? Consider checking where the 10-year Treasury yield (TNX—purple line) was trading at any given time. Because the two have been closely correlated throughout 2021, with Tech soaring when yields flagged and then coming back to earth as yields recovered, the way they are now. This year-to-date chart makes the correlation pretty clear. Data Sources: S&P Dow Jones Indices, CBOE Global Markets. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

End of Q3 Review: Today’s the last day of a volatile quarter for Wall Street, marked by everything from a historically strong earnings season to the Delta variant to hints of the Fed finally taking baby steps away from its long cycle of monetary easing. Looking back, it’s not surprising, really, to see that Financials and Technology shares led the way in Q3, with Financials rising nearly 4% quarter to date and Tech up 2.6%. The Tech sector might have benefitted from more of a “stay at home” move away from “reopening” stocks at times during the quarter as Delta took its toll on the travel, casino, hotel, and other sectors that tend to do better when the economy is reopening.

Financials, meanwhile, have gotten a boost from rising inflation that’s helped lead to the Fed’s hints at a more hawkish policy. You’d think Energy would also be on the Q3 leaderboard, and it has been hot lately. Overall, however, the Energy sector is actually down 1% over the last three months. The SPX would appear to have had a quiet quarter, up 1.45% through Wednesday, if you hadn’t been along for the bumpy ride.

Coffee Rally Brewing: Commodity prices are booming, but so are margin costs. But there are other ways to express an opinion on the market direction of one of the world’s favorite ways to caffeinate. While drinking a mug of Joe, consider this: a major coffee-growing region in Brazil was recently hit by an unseasonal blast of polar air, hurting an estimated 10% of the coffee bean bushes. Meanwhile, coffee commodity prices have been steadily climbing since Oct. 2020.

The International Coffee Organization estimates that coffee prices will rise globally due to low supply and supply chain disruptions, adding that the world’s coffee consumption is expected to climb by 1.9% to 167.2 million bags in 2020-2021, compared to 164.1 million bags in the year 2019-2020. Commodities trading can be a useful hedging tool, but it also carries notoriously high risk with margin calls that can quickly become exponentially more than the initial amount of money put down.

Stocks, which also carry risk, tend not to have such extreme moves. So, if the belief is that others will agree that coffee is the beverage of choice, think about where it can be bought, like Starbucks SBUX or McDonald’s MCD with its plans to open 4,000 McCafes in China. Other coffee industry players to get a caffeine fix include manufacturers J.M. Smucker SJM, which owns Folgers and Dunkin’, and Coffee Holding Co. JVA, which includes Private Label and Wholesale Green coffee, or coffee roaster and distributor Farmer Brothers FARM.

Will Gold Hold? Technical traders and die-hard gold bugs are likely keeping their eyes on the critical support level of $1,680 an ounce. Not only does it mark a 61.8% retracement from the March 2020 low to the yellow metal’s all-time high, something of an “uncle point” for chartists, that level has also been tested three times—in March, April, and August of this year. Each test resulted in a strong and sharp bounce, as both bulls and “bugs” saw that level as a signal to load up on the metal. Beyond that, however, there hasn’t been enough momentum over the last twelve months to drive a follow-through. This time around, gold’s luster appears to be dimming as it approaches its fourth retest.

The recent spike in 10-year yields helped cause a dramatic tumble in the markets, led by Tech. But it did very little for gold, except provide a kind of calm negative consistency; hinting that bearishness in the yellow metal just might be the right side of the market. Rising 10-year yields and a strengthening dollar often signal downside for gold. If the metal fails to claw above $1,835 in the near term and instead falls below $1,680, it’s quite possible that gold bulls and bugs may be packing up for a swift retreat to $1,600, the next potential support level.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image Sourced from Pixabay

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.