This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

(Monday Market Open) WTI crude oil futures spiked over the weekend—trading as high as $130 per barrel—as an increasing number of companies are choosing not to buy Russian oil. Before the opening bell, oil prices had retreated to $120, which was still 3.85% higher than the closing price on Friday. The higher oil prices are pushing equity index futures lower in premarket trading. The S&P 500 futures are down about 0.86% as the benchmark index is testing the 4,300 support level once again. This level has been an important level over the last few weeks and even back into July of 2021.

In addition to private companies refusing to buy Russian oil, U.S. Secretary of State Antony Blinken said the United States and European allies were considering a ban on Russian oil. Previously, these groups have avoided bans on Russian commodities because of how these embargos could hurt consumers already struggling under the weight of pandemic-related inflation.

Embargos on oil could be quite expensive. Analysts from Bank of America BAC said if Russia’s 5 million barrels per day were to end, oil prices could rise to $200. JP Morgan JPM analysts are forecasting oil prices at $185 per barrel this year. Analysts from Mitsubishi UFJ Financial Groups MUFG were projecting oil at $180 per barrel and added if that price was reached it would probably cause a global recession.

Government officials are hoping that reduced sanctions on Iran and Venezuela will get more oil supplies to market and help alleviate some of the price pressures. Additionally, Republicans are pressuring President Joe Biden to repeal some of his executive orders signed when he first came into office. These orders banned some offshore drilling as well as some drilling on public lands.

Ukraine continues to struggle as it fights back against the Russian invasion. Ukrainian President Volodymyr Zelensky is asking the Western allies to help by enforcing a no-fly zone over Ukraine. However, the allies have been unwilling to get directly involved in the conflict out of fear of escalation. The Cboe Market Volatility Index (VIX) spiked above 36 this morning and may not retreat without major improvement in Ukraine.

Interest in Rates

The Consumer Price Index (CPI) comes out on Thursday and will provide important inflation information in preparation for next week’s Federal Reserve interest rate decision. After Fed Chairman Jerome Powell told Congress last week he favored a quarter point hike, the market has adjusted its expectations accordingly. The market is also confident that another hike will come in May, but the picture is increasingly unclear because of the Russian-Ukraine conflict. According to comments from the Kroger KR earnings announcement last week, inflation is rising across the board.

Looking at individual stocks, Bed Bath & Beyond BBBY jumped more than 80% in premarket trading after it was reported that GameStop GME chairman and Chewy CHWY co-founder Ryan Cohen’s company, RC Ventures, took a 10% stake in the company.

Also, Uber UBER rose about 3% in premarket trading after the company adjusted its first quarter outlook. The company reported a faster-than-expected rebound from the Omicron-related slowdown and is now seeing a “significant” demand in rides.

Friday’s Action

It’s starting to sound like a broken record—the major indexes continued to slide today. Leading the way were the Nasdaq Composite ($COMP), down 1.66%, the Russell 2000 (RUT), down 1.55%, the Dow Jones Industrial Average ($DJI), down 0.53%, and the S&P 500 (SPX), down 0.79%. Large-cap stocks weighing down the Dow were Boeing (BA), down 4.24% to a 17-month low, American Express (AXP), down 3.86%, and Visa (V), down 3.35%. Shares of several banks and financial services companies are trading lower amid market weakness after Russian forces in Ukraine seized control of the Zaporizhzhia nuclear power plant. The conflict has also pressured U.S. Treasury yields as the 10-year Treasury yield (TNX) fell 6.51% to end at 17.24. It appeared there’s no buying on the dip going into the weekend.

Today’s strong sectors were energy, utilities, real estate, health care, and consumer staples. Weaker sectors were financials, information technology, and consumer discretionary.

The United States added 678,000 new jobs to the economy in February, and the unemployment rate fell to 3.8%. These were some great numbers compared to the expectation of 440,000 jobs and 3.9% on the jobless rate. This report confirms that the rampant Omicron variant spread during the winter had little impact and shows a big decrease from last February’s 6.2 % rate. In February 2020, prior to the coronavirus pandemic, the unemployment rate was 3.5%.

New job growth was led by leisure and hospitality with 179,000, professional and business services with 95,000, health care with 64,000, and construction with 60,000. Average hourly earnings for all employees on private nonfarm payrolls came in at $31.58 and were barely changed over the month (+.01) after large increases in recent months. Over the past 12 months, average hourly earnings have increased 5.1%. In February, average hourly earnings of private-sector production and nonsupervisory employees rose $0.08 to end at $26.94.

Increasing Geopolitical Risk

Despite the positive Jobs report, the continuing conflict between Russia and Ukraine is the progress of the overall market. The conflict escalation has continued to lift oil and energy sectors as WTI crude oil traded around $111 per barrel, hitting the highest level in 14 years, earlier in the week. Occidental Petroleum OXY was up 17.59%, PBF Energy Inc. PBF was up 16.62%, and Peabody Energy BTU was up 14.71% and led energy stocks. Fertilizer company Mosaic MOS was up 7.49%, grocer Kroger KR was up 6.79%, and industrial company Alcoa (AA) was up 9.37% and led non-energy companies. The Cboe Market Volatility Index (VIX) settled off its highs to end at 31.98 but stayed in a range, which reflects market uncertainty.

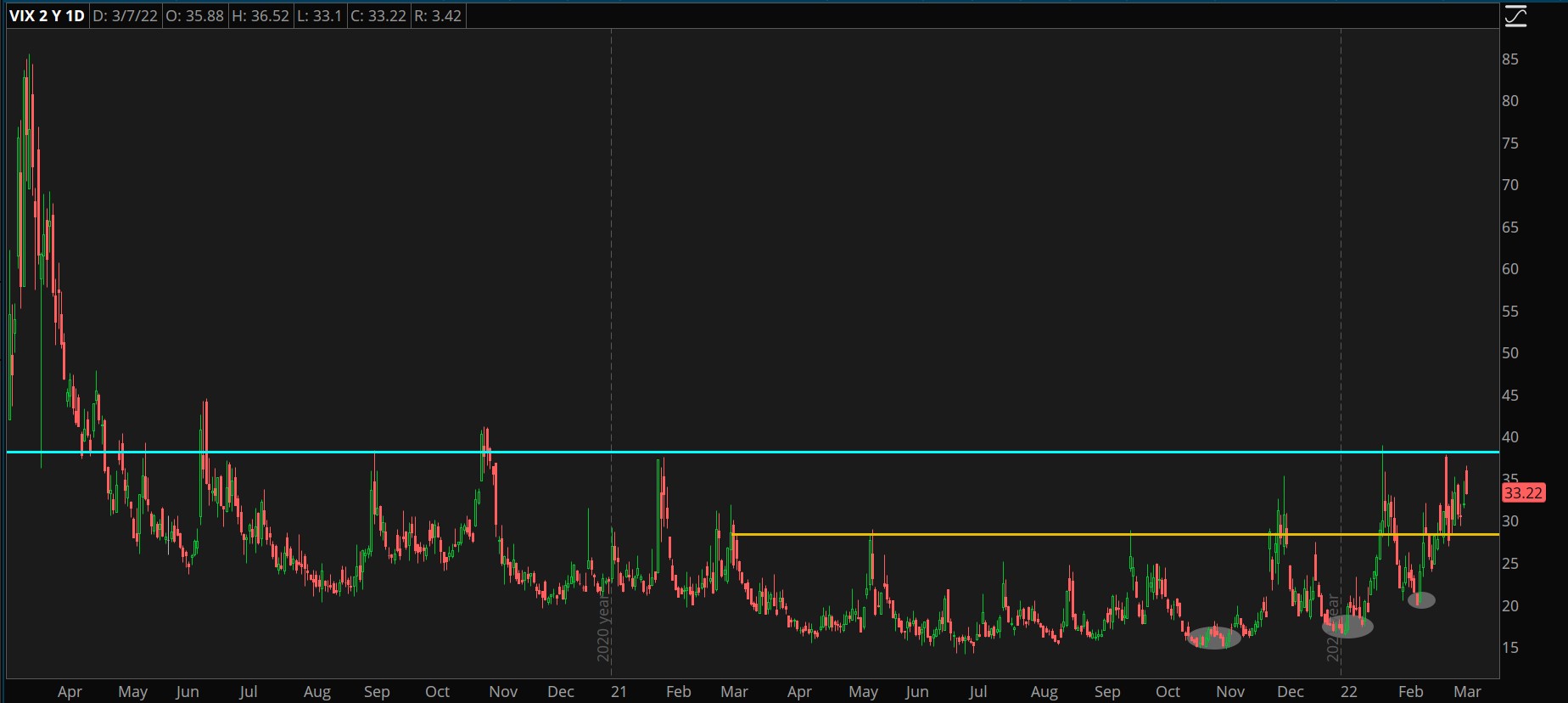

CHART OF THE DAY: APPLYING THE VIX. The Cboe Market Volatility Index (VIX—candlesticks) has been building since the first of the year and is near its previous reversal level around 39. Data Sources: ICE, S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Fear Gauge: The VIX continues to build and is nearly testing its reversal area around the 39 to 40 level. Increased uncertainty among investors isn’t seeing any progress because of the Russia-Ukraine situation. While Russian officials have talked about potential ceasefires, the bombing has continued. If the 39 level in the VIX is broken, it’s likely that the 4,300 support level in the S&P 500 (SPX) will also break, which would be bearish for stocks.

Earnings Update: According to Refinitiv, thus far, 493 companies in the S&P 500 have reported earnings with 76.5% beating analysts estimates. This is higher than the historical average of 65.9% but lower than the previous four-quarter average of 83.9%. The year-over-year earnings are on track for a 32% increase, but the energy sector continues to carry earnings. When energy is removed from the numbers, the growth is 23.4%.

FactSet is reporting that the S&P 500 has an estimated earnings growth rate of 4.8% for the quarter which is the lowest quarter since Q4 2020. Earnings estimates for the S&P 500 in Q1 have fallen 1.2% with eight of the 11 sectors decreasing forecasts. Only energy, real estate, and technology are expecting increases. Inflation concerns could continue to cut into these earnings estimates unless some relief is provided soon.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Pixabay

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.